What is Global Electronic Device History Record Solution Market?

The Global Electronic Device History Record Solution Market is a rapidly evolving sector that focuses on the management and documentation of electronic device histories. This market provides solutions that help in tracking the lifecycle of electronic devices, from manufacturing to end-of-life. These solutions are crucial for industries that require stringent compliance with regulatory standards, such as healthcare, automotive, and aerospace. By maintaining a comprehensive record of each device's history, companies can ensure quality control, traceability, and accountability. This not only aids in meeting regulatory requirements but also enhances operational efficiency and reduces the risk of recalls or defects. The market is driven by the increasing demand for transparency and traceability in manufacturing processes, as well as the growing complexity of electronic devices. As technology continues to advance, the need for robust electronic device history record solutions is expected to grow, making it an essential component of modern manufacturing and quality assurance processes.

Cloud Based, On-premises in the Global Electronic Device History Record Solution Market:

The Global Electronic Device History Record Solution Market can be broadly categorized into two deployment models: cloud-based and on-premises. Cloud-based solutions are hosted on remote servers and accessed via the internet, offering several advantages such as scalability, flexibility, and cost-effectiveness. These solutions allow companies to store and manage large volumes of data without the need for significant upfront investment in hardware or infrastructure. Cloud-based solutions are particularly beneficial for small to medium-sized enterprises (SMEs) that may not have the resources to maintain extensive IT infrastructure. They also offer the advantage of remote access, enabling users to access device history records from anywhere, at any time, which is particularly useful for companies with multiple locations or remote teams. On the other hand, on-premises solutions are installed and run on a company's own servers and infrastructure. These solutions offer greater control over data security and privacy, as the data is stored within the company's own network. This can be a critical factor for industries that handle sensitive information or are subject to strict regulatory requirements. On-premises solutions also allow for greater customization, as companies can tailor the software to meet their specific needs and integrate it with existing systems. However, they require a significant upfront investment in hardware and infrastructure, as well as ongoing maintenance and support. Despite these differences, both cloud-based and on-premises solutions play a crucial role in the Global Electronic Device History Record Solution Market. Companies must carefully evaluate their specific needs, resources, and regulatory requirements when choosing between these deployment models. As the market continues to evolve, we can expect to see further advancements in both cloud-based and on-premises solutions, offering even greater functionality and flexibility to meet the diverse needs of businesses across various industries.

Medical, Diagnosis, Other in the Global Electronic Device History Record Solution Market:

The Global Electronic Device History Record Solution Market finds significant application in various sectors, including medical, diagnostic, and other industries. In the medical field, these solutions are essential for ensuring the safety and efficacy of medical devices. By maintaining a detailed history of each device, manufacturers can track performance, identify potential issues, and ensure compliance with regulatory standards. This is particularly important in the medical industry, where device failures can have serious consequences for patient safety. Electronic device history records also facilitate the efficient management of recalls, allowing manufacturers to quickly identify and address any defects. In the diagnostic sector, these solutions play a crucial role in ensuring the accuracy and reliability of diagnostic equipment. By tracking the history of each device, companies can monitor performance, identify trends, and implement preventive maintenance measures to minimize downtime and ensure accurate results. This is particularly important in laboratories and healthcare facilities, where timely and accurate diagnostics are critical for patient care. Beyond the medical and diagnostic sectors, electronic device history record solutions are also used in a variety of other industries, including automotive, aerospace, and consumer electronics. In these industries, maintaining a comprehensive record of each device's history is essential for quality control, traceability, and compliance with regulatory standards. By providing a detailed history of each device, these solutions help companies ensure product quality, reduce the risk of defects, and enhance customer satisfaction. As technology continues to advance and regulatory requirements become more stringent, the demand for robust electronic device history record solutions is expected to grow across various industries.

Global Electronic Device History Record Solution Market Outlook:

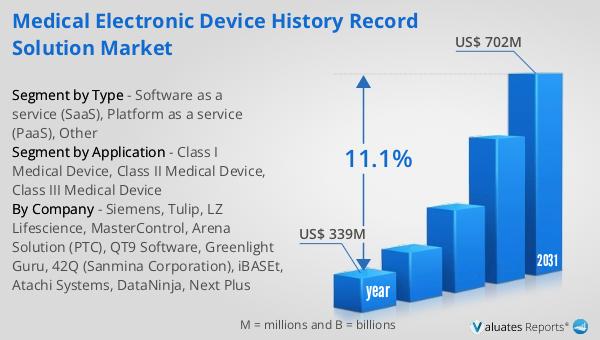

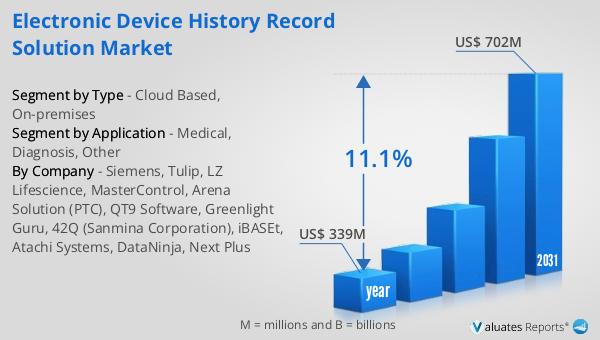

The global market for Electronic Device History Record Solution was valued at $339 million in 2024 and is anticipated to expand significantly, reaching an estimated $702 million by 2031. This growth is projected to occur at a compound annual growth rate (CAGR) of 11.1% over the forecast period. This impressive growth trajectory underscores the increasing importance of electronic device history record solutions across various industries. As companies strive to enhance quality control, ensure regulatory compliance, and improve operational efficiency, the demand for these solutions is expected to rise. The market's expansion is driven by several factors, including the growing complexity of electronic devices, the need for transparency and traceability in manufacturing processes, and the increasing emphasis on quality assurance. Additionally, advancements in technology and the rising adoption of cloud-based solutions are expected to further fuel market growth. As the market continues to evolve, companies will need to stay abreast of the latest trends and developments to remain competitive and capitalize on the opportunities presented by this dynamic and rapidly growing market.

| Report Metric | Details |

| Report Name | Electronic Device History Record Solution Market |

| Accounted market size in year | US$ 339 million |

| Forecasted market size in 2031 | US$ 702 million |

| CAGR | 11.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Siemens, Tulip, LZ Lifescience, MasterControl, Arena Solution (PTC), QT9 Software, Greenlight Guru, 42Q (Sanmina Corporation), iBASEt, Atachi Systems, DataNinja, Next Plus |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |