What is Global Probiotics Based Dietary Supplement Market?

The Global Probiotics Based Dietary Supplement Market is a rapidly evolving sector within the broader health and wellness industry. Probiotics are live microorganisms that, when consumed in adequate amounts, confer health benefits to the host. These dietary supplements are designed to improve gut health, boost the immune system, and enhance overall well-being. The market is driven by increasing consumer awareness about the health benefits of probiotics, rising demand for functional foods, and a growing trend towards preventive healthcare. Additionally, the aging population and the prevalence of digestive disorders have further fueled the demand for probiotic supplements. The market encompasses a wide range of products, including capsules, tablets, powders, and liquids, each catering to different consumer preferences and needs. As consumers become more health-conscious, the demand for natural and effective health solutions like probiotics continues to rise, making this market a significant area of interest for manufacturers and investors alike. The global reach of this market is evident as it caters to diverse demographics and regions, adapting to varying dietary habits and health concerns.

Capsule, Tablets, Powder, Liquid in the Global Probiotics Based Dietary Supplement Market:

In the Global Probiotics Based Dietary Supplement Market, products are available in various forms, including capsules, tablets, powders, and liquids, each offering unique benefits and catering to different consumer preferences. Capsules are one of the most popular forms due to their convenience and ease of consumption. They are often preferred by consumers who seek a quick and straightforward way to incorporate probiotics into their daily routine. Capsules are designed to protect the probiotics from stomach acid, ensuring that a significant number of live microorganisms reach the intestines where they exert their beneficial effects. Tablets, on the other hand, are similar to capsules but may offer additional benefits such as extended-release formulations. They are often chosen by consumers who prefer a more traditional supplement form and may include additional ingredients to enhance the probiotic effects. Powders are another popular form, offering flexibility in consumption. They can be easily mixed with water, juice, or smoothies, making them an ideal choice for those who prefer a more customizable approach to their probiotic intake. Powders are also often used in formulations targeting specific health concerns, such as digestive health or immune support. Liquid probiotics are gaining popularity due to their fast absorption and ease of use. They are particularly appealing to consumers who have difficulty swallowing pills or prefer a more natural form of supplementation. Liquid probiotics can be consumed directly or added to beverages, providing a versatile option for those seeking to improve their gut health. Each form of probiotic supplement has its own set of advantages, and the choice often depends on individual preferences, lifestyle, and specific health goals. As the market continues to grow, manufacturers are innovating and expanding their product offerings to meet the diverse needs of consumers, ensuring that there is a probiotic supplement suitable for everyone.

Online Sales, Offline Sales in the Global Probiotics Based Dietary Supplement Market:

The usage of Global Probiotics Based Dietary Supplements is prevalent in both online and offline sales channels, each offering distinct advantages and catering to different consumer behaviors. Online sales have seen significant growth in recent years, driven by the increasing penetration of the internet and the convenience of e-commerce platforms. Consumers are increasingly turning to online platforms to purchase probiotics due to the ease of access, wide variety of products, and the ability to compare prices and read reviews. Online sales channels also offer the advantage of home delivery, making it easier for consumers to maintain a consistent supply of their preferred probiotic supplements. Additionally, online platforms often provide detailed product information and customer reviews, helping consumers make informed purchasing decisions. On the other hand, offline sales channels, such as pharmacies, health food stores, and supermarkets, continue to play a crucial role in the distribution of probiotic supplements. These channels offer the advantage of immediate product availability and the opportunity for consumers to seek advice from knowledgeable staff. Many consumers prefer purchasing probiotics offline to ensure product authenticity and quality, as well as to receive personalized recommendations based on their specific health needs. Offline sales channels also provide the opportunity for consumers to physically examine the product before purchase, which can be an important factor for those who are new to probiotics or have specific preferences regarding packaging and formulation. Both online and offline sales channels are essential for the growth and accessibility of the Global Probiotics Based Dietary Supplement Market, each catering to different consumer preferences and contributing to the overall expansion of the market. As consumer awareness and demand for probiotics continue to rise, both channels are expected to evolve and adapt to meet the changing needs of consumers, ensuring that probiotic supplements remain accessible and appealing to a broad audience.

Global Probiotics Based Dietary Supplement Market Outlook:

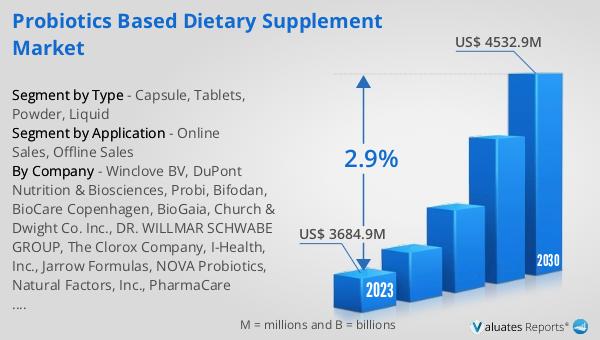

The outlook for the Global Probiotics Based Dietary Supplement Market indicates a promising future, with the market valued at US$ 3910 million in 2024 and projected to reach a revised size of US$ 4776 million by 2031, growing at a compound annual growth rate (CAGR) of 2.9% during the forecast period. This growth is driven by increasing consumer awareness of the health benefits associated with probiotics, as well as the rising demand for natural and effective health solutions. The market is characterized by a diverse range of players, with BioGaia Probi AB, iHealth, Winclove, and Probiotics International Ltd (Protexin) being among the top five companies. Despite their prominence, these companies collectively hold only a 20% share of the market, indicating a highly competitive landscape with numerous players vying for market share. This competitive environment encourages innovation and the development of new and improved probiotic products, catering to the evolving needs and preferences of consumers. As the market continues to expand, companies are focusing on research and development to enhance the efficacy and appeal of their probiotic offerings, ensuring that they remain at the forefront of this dynamic industry. The Global Probiotics Based Dietary Supplement Market is poised for continued growth, driven by the increasing demand for health and wellness products and the ongoing innovation within the sector.

| Report Metric | Details |

| Report Name | Probiotics Based Dietary Supplement Market |

| Accounted market size in year | US$ 3910 million |

| Forecasted market size in 2031 | US$ 4776 million |

| CAGR | 2.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Winclove BV, DuPont Nutrition & Biosciences, Probi, Bifodan, BioCare Copenhagen, BioGaia, Church & Dwight Co. Inc., DR. WILLMAR SCHWABE GROUP, The Clorox Company, I-Health, Inc., Jarrow Formulas, NOVA Probiotics, Natural Factors, Inc., PharmaCare Laboratories |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |