What is Global Animal Epidemic Prevention Technical Service Market?

The Global Animal Epidemic Prevention Technical Service Market is a specialized sector focused on safeguarding animal health by preventing and controlling the spread of infectious diseases among animals. This market encompasses a range of services and products designed to monitor, diagnose, and manage animal epidemics, ensuring the health and productivity of livestock and pets. These services are crucial for maintaining food security, public health, and economic stability, as animal diseases can have significant impacts on agriculture and trade. The market includes various stakeholders such as veterinary service providers, diagnostic laboratories, pharmaceutical companies, and government agencies, all working collaboratively to implement effective disease prevention strategies. With the increasing demand for animal-derived food products and the rising awareness of zoonotic diseases, the importance of this market continues to grow. Technological advancements in diagnostics and vaccines, along with supportive government policies, are driving the expansion of the Global Animal Epidemic Prevention Technical Service Market, making it a vital component of the global animal health industry.

Vaccines, Reagents in the Global Animal Epidemic Prevention Technical Service Market:

Vaccines and reagents play a pivotal role in the Global Animal Epidemic Prevention Technical Service Market, serving as essential tools in the fight against animal diseases. Vaccines are biological preparations that provide immunity to specific diseases, helping to prevent outbreaks and control the spread of infections among animal populations. They work by stimulating the animal's immune system to recognize and combat pathogens, thereby reducing the incidence of disease and minimizing economic losses in the livestock industry. The development and distribution of vaccines are critical components of animal health management, with ongoing research focused on improving their efficacy, safety, and accessibility. Reagents, on the other hand, are substances or compounds used in diagnostic tests to detect the presence of pathogens or antibodies in animal samples. They are integral to the accurate diagnosis of diseases, enabling timely intervention and treatment. The use of reagents in diagnostic laboratories allows for the rapid identification of infectious agents, facilitating the implementation of targeted control measures. Together, vaccines and reagents form the backbone of animal epidemic prevention efforts, providing the necessary tools to protect animal health and ensure the sustainability of livestock production. The market for these products is driven by the increasing prevalence of animal diseases, the growing demand for animal-derived food products, and the need for effective disease management strategies. As the global population continues to rise, the demand for meat, dairy, and other animal products is expected to increase, further emphasizing the importance of vaccines and reagents in maintaining animal health and productivity. Additionally, the threat of zoonotic diseases, which can be transmitted from animals to humans, underscores the need for robust animal health systems and effective disease prevention measures. The development of new and improved vaccines and reagents is a key focus for researchers and companies in the Global Animal Epidemic Prevention Technical Service Market. Advances in biotechnology and molecular biology are enabling the creation of more effective and targeted vaccines, while innovations in diagnostic technologies are enhancing the sensitivity and specificity of reagents. These advancements are crucial for addressing emerging and re-emerging animal diseases, as well as for improving the overall efficiency of animal health management. Furthermore, the increasing emphasis on sustainable and ethical livestock production is driving the demand for vaccines and reagents that are not only effective but also environmentally friendly and socially responsible. The Global Animal Epidemic Prevention Technical Service Market is characterized by a diverse range of products and services, with vaccines and reagents being among the most important. The market is highly competitive, with numerous companies and research institutions involved in the development and commercialization of these products. Collaboration between industry, academia, and government agencies is essential for advancing research and ensuring the availability of high-quality vaccines and reagents. The regulatory environment also plays a significant role in shaping the market, with stringent requirements for the approval and distribution of animal health products. Overall, vaccines and reagents are indispensable components of the Global Animal Epidemic Prevention Technical Service Market, providing the tools needed to protect animal health, ensure food security, and safeguard public health.

Pig, Cattle, Poultry, Others in the Global Animal Epidemic Prevention Technical Service Market:

The Global Animal Epidemic Prevention Technical Service Market plays a crucial role in the health management of various animal species, including pigs, cattle, poultry, and others. In the pig industry, the market provides essential services and products to prevent and control diseases such as African Swine Fever, Porcine Reproductive and Respiratory Syndrome, and Foot-and-Mouth Disease. These diseases can have devastating effects on pig populations, leading to significant economic losses for farmers and impacting the global pork supply. Vaccines and diagnostic reagents are vital tools in the prevention and management of these diseases, enabling early detection and effective intervention. In the cattle industry, the market focuses on preventing diseases such as Bovine Respiratory Disease, Bovine Viral Diarrhea, and Mastitis. These diseases can affect the health and productivity of cattle, leading to reduced milk production and increased mortality rates. The use of vaccines and diagnostic tests helps to maintain the health of cattle herds, ensuring the sustainability of the dairy and beef industries. The market also provides technical services such as herd health management and biosecurity measures to prevent the introduction and spread of infectious diseases. In the poultry industry, the Global Animal Epidemic Prevention Technical Service Market addresses diseases such as Avian Influenza, Newcastle Disease, and Infectious Bronchitis. These diseases can spread rapidly among poultry flocks, leading to high mortality rates and significant economic losses. Vaccination programs and diagnostic testing are essential components of disease prevention and control in the poultry industry, helping to protect the health of birds and ensure the safety of poultry products. The market also offers biosecurity services and training programs to help poultry producers implement effective disease prevention strategies. In addition to pigs, cattle, and poultry, the Global Animal Epidemic Prevention Technical Service Market also serves other animal species, including sheep, goats, and companion animals. The market provides vaccines and diagnostic tests for diseases such as Bluetongue, Scrapie, and Canine Parvovirus, helping to protect the health of these animals and prevent the spread of infectious diseases. The market also offers technical services such as disease surveillance and outbreak response, ensuring that animal health professionals have the tools and resources needed to manage disease outbreaks effectively. Overall, the Global Animal Epidemic Prevention Technical Service Market is an essential component of animal health management, providing the tools and services needed to prevent and control infectious diseases in a wide range of animal species. By ensuring the health and productivity of livestock and companion animals, the market plays a vital role in supporting food security, public health, and economic stability.

Global Animal Epidemic Prevention Technical Service Market Outlook:

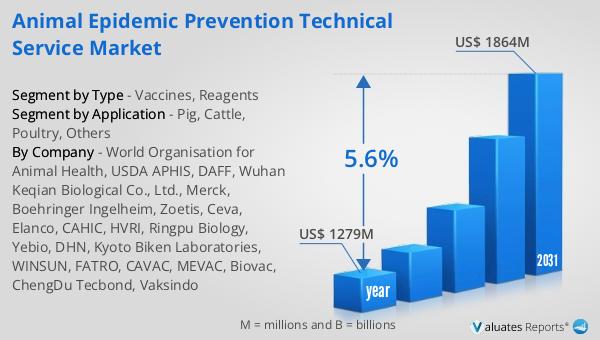

The global market for Animal Epidemic Prevention Technical Service was valued at $1,279 million in 2024 and is anticipated to grow to a revised size of $1,864 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.6% over the forecast period. In the United Kingdom, annual spending on veterinary and other pet services has seen a significant increase, rising from £2.6 billion in 2015 to £4 billion in 2021, marking a 54% increase over six years. According to Vetnosis, the global animal health industry's value was projected to rise by 12% to $38.3 billion in 2021. Additionally, data from the 2022 China Pet Medical Industry White Paper indicates that the market size of China's pet medical sector is approximately 67.5 billion yuan, accounting for about 22.5% of the entire pet industry. These figures highlight the growing importance and investment in animal health services globally, driven by increasing awareness of animal welfare, the rising demand for animal-derived products, and the need for effective disease prevention and management strategies. The expansion of the Global Animal Epidemic Prevention Technical Service Market is supported by technological advancements, government initiatives, and the collaboration of various stakeholders in the animal health sector.

| Report Metric | Details |

| Report Name | Animal Epidemic Prevention Technical Service Market |

| Accounted market size in year | US$ 1279 million |

| Forecasted market size in 2031 | US$ 1864 million |

| CAGR | 5.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | World Organisation for Animal Health, USDA APHIS, DAFF, Wuhan Keqian Biological Co., Ltd., Merck, Boehringer Ingelheim, Zoetis, Ceva, Elanco, CAHIC, HVRI, Ringpu Biology, Yebio, DHN, Kyoto Biken Laboratories, WINSUN, FATRO, CAVAC, MEVAC, Biovac, ChengDu Tecbond, Vaksindo |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |