What is Global Compositing Software Market?

The Global Compositing Software Market refers to the industry focused on the development and distribution of software tools used for compositing in digital media production. Compositing is a crucial process in the creation of visual effects, where multiple images or video elements are combined to create a single, cohesive scene. This software is widely used in film, television, video games, and advertising to create stunning visual effects and seamless transitions. The market encompasses a range of software solutions, from basic tools for beginners to advanced systems for professional studios. These tools allow artists to manipulate images, adjust colors, and integrate computer-generated imagery with live-action footage. The demand for compositing software is driven by the increasing production of digital content and the need for high-quality visual effects. As technology advances, the capabilities of compositing software continue to expand, offering more sophisticated features and improved performance. The market is characterized by a mix of established companies and innovative startups, all competing to provide the most effective and user-friendly solutions. Overall, the Global Compositing Software Market plays a vital role in the digital media industry, enabling creators to bring their visions to life with precision and creativity.

On-Premise, Cloud in the Global Compositing Software Market:

The Global Compositing Software Market is segmented into two primary deployment models: On-Premise and Cloud-based solutions. On-Premise compositing software refers to applications that are installed and run on computers within the user's premises. This model offers several advantages, particularly for larger enterprises with specific security and compliance requirements. By hosting the software on their own servers, companies have greater control over their data and can ensure that sensitive information remains secure. Additionally, On-Premise solutions often provide more customization options, allowing businesses to tailor the software to their specific needs. However, this model also comes with certain drawbacks, such as higher upfront costs for hardware and software licenses, as well as ongoing maintenance and IT support expenses. Despite these challenges, On-Premise compositing software remains a popular choice for organizations that prioritize data security and have the resources to manage their own IT infrastructure. On the other hand, Cloud-based compositing software offers a more flexible and cost-effective alternative. With this model, the software is hosted on remote servers and accessed via the internet, allowing users to work from anywhere with an internet connection. This is particularly beneficial for small and medium-sized enterprises (SMEs) that may not have the budget or infrastructure to support On-Premise solutions. Cloud-based software typically operates on a subscription model, which reduces the initial investment and allows businesses to scale their usage according to their needs. Additionally, cloud solutions often come with automatic updates and maintenance, relieving users of the burden of managing software upgrades and technical issues. The collaborative nature of cloud-based software also facilitates teamwork, as multiple users can access and work on projects simultaneously, regardless of their physical location. Despite the advantages of Cloud-based solutions, there are also potential concerns, particularly regarding data security and internet reliability. Storing data on remote servers can pose risks if the provider's security measures are not robust enough to protect against breaches. Additionally, reliance on internet connectivity means that any disruptions can impact productivity. However, many cloud providers invest heavily in security and offer service level agreements (SLAs) to ensure reliability and data protection. As a result, the adoption of Cloud-based compositing software is growing rapidly, driven by the increasing demand for flexible, scalable, and cost-effective solutions. In conclusion, both On-Premise and Cloud-based compositing software have their unique advantages and challenges. The choice between the two largely depends on the specific needs and resources of the organization. Larger enterprises with stringent security requirements and the ability to manage their own IT infrastructure may prefer On-Premise solutions. In contrast, SMEs and businesses seeking flexibility and lower upfront costs may find Cloud-based software more appealing. As the Global Compositing Software Market continues to evolve, it is likely that we will see further innovations in both deployment models, offering even more options for businesses of all sizes.

Larger Enterprise, Medium and Small Enterprise in the Global Compositing Software Market:

The usage of Global Compositing Software Market varies significantly across different types of enterprises, including larger enterprises, medium-sized enterprises, and small enterprises. Larger enterprises, such as major film studios and multinational advertising agencies, often have extensive resources and complex requirements for their compositing software. These organizations typically invest in high-end, On-Premise solutions that offer advanced features and customization options. The ability to control and secure their data is a top priority, given the sensitive nature of the projects they handle. Larger enterprises also benefit from having dedicated IT teams to manage the software and ensure it integrates seamlessly with other tools in their production pipeline. The scalability of On-Premise solutions allows these organizations to handle large volumes of data and complex visual effects projects efficiently. Medium-sized enterprises, which may include regional production companies and independent studios, often have different needs and constraints. While they may not have the same level of resources as larger enterprises, they still require powerful compositing tools to produce high-quality content. For these organizations, Cloud-based compositing software can be an attractive option. The subscription-based model reduces the initial investment, making it more accessible for medium-sized enterprises with limited budgets. Additionally, the flexibility of cloud solutions allows these companies to scale their usage as needed, without the need for significant infrastructure investments. The collaborative features of cloud-based software also enable medium-sized enterprises to work with remote teams and freelancers, expanding their creative capabilities. Small enterprises, such as independent filmmakers and boutique agencies, often operate with tight budgets and limited resources. For these businesses, affordability and ease of use are critical factors when choosing compositing software. Cloud-based solutions are particularly appealing to small enterprises, as they offer a low-cost entry point and eliminate the need for expensive hardware and IT support. The ability to access the software from any location is also a significant advantage, allowing small enterprises to work flexibly and collaborate with partners worldwide. While small enterprises may not require the same level of customization as larger organizations, they still benefit from the powerful features and intuitive interfaces offered by modern compositing software. In summary, the Global Compositing Software Market serves a diverse range of enterprises, each with its unique needs and challenges. Larger enterprises prioritize security and customization, often opting for On-Premise solutions that offer greater control over their data and production processes. Medium-sized enterprises benefit from the flexibility and cost-effectiveness of Cloud-based software, which allows them to scale their operations and collaborate with remote teams. Small enterprises, with their focus on affordability and ease of use, find Cloud-based solutions particularly advantageous, enabling them to produce high-quality content without significant upfront investments. As the market continues to evolve, compositing software providers are likely to develop even more tailored solutions to meet the specific needs of enterprises of all sizes.

Global Compositing Software Market Outlook:

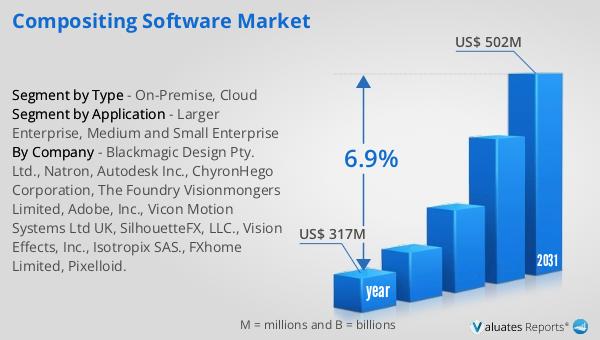

The outlook for the Global Compositing Software Market indicates a promising growth trajectory. In 2024, the market was valued at approximately $317 million, reflecting its significance in the digital media industry. Looking ahead, projections suggest that by 2031, the market will expand to a revised size of around $502 million. This growth is expected to occur at a compound annual growth rate (CAGR) of 6.9% over the forecast period. This upward trend underscores the increasing demand for compositing software as digital content production continues to rise. The market's expansion is driven by advancements in technology, which enhance the capabilities of compositing tools, making them more efficient and user-friendly. Additionally, the growing popularity of digital media, including films, television, and online content, fuels the need for sophisticated visual effects, further boosting the demand for compositing software. As the industry evolves, both established companies and new entrants are likely to innovate and compete to capture a share of this expanding market. Overall, the Global Compositing Software Market is poised for significant growth, offering numerous opportunities for businesses and professionals involved in digital media production.

| Report Metric | Details |

| Report Name | Compositing Software Market |

| Accounted market size in year | US$ 317 million |

| Forecasted market size in 2031 | US$ 502 million |

| CAGR | 6.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Blackmagic Design Pty. Ltd., Natron, Autodesk Inc., ChyronHego Corporation, The Foundry Visionmongers Limited, Adobe, Inc., Vicon Motion Systems Ltd UK, SilhouetteFX, LLC., Vision Effects, Inc., Isotropix SAS., FXhome Limited, Pixelloid. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |