What is Global Orange Pulp Market?

The Global Orange Pulp Market is a segment of the food and beverage industry that focuses on the production, distribution, and consumption of orange pulp. Orange pulp is the fibrous material found in oranges, which is often used in the production of juices, smoothies, and other food products. This market is driven by the increasing demand for natural and healthy food products, as consumers become more health-conscious and seek out products with fewer artificial ingredients. The market is also influenced by the growing popularity of citrus fruits due to their high vitamin C content and other health benefits. Additionally, the orange pulp market is supported by advancements in food processing technologies that allow for the efficient extraction and preservation of pulp, ensuring that it retains its nutritional value and flavor. The market is global in scope, with key regions including North America, Europe, Asia-Pacific, and Latin America, each with its own unique consumer preferences and regulatory environments. As the demand for orange pulp continues to grow, companies in this market are focusing on innovation and sustainability to meet consumer needs and reduce their environmental impact.

Organic, Conventional in the Global Orange Pulp Market:

In the Global Orange Pulp Market, products are typically categorized into two main types: organic and conventional. Organic orange pulp is derived from oranges that are grown without the use of synthetic pesticides, fertilizers, or genetically modified organisms (GMOs). This type of pulp is increasingly popular among consumers who are concerned about the environmental impact of conventional farming practices and the potential health risks associated with chemical residues in food. Organic orange pulp is often perceived as being more natural and healthier, which can justify its higher price point compared to conventional options. The production of organic orange pulp requires adherence to strict agricultural standards and certifications, which can vary by region but generally emphasize sustainable farming practices and the preservation of biodiversity. On the other hand, conventional orange pulp is produced using traditional farming methods that may involve the use of synthetic chemicals to enhance crop yield and protect against pests and diseases. This type of pulp is typically more affordable and widely available, making it accessible to a broader range of consumers. However, there is growing awareness and concern about the environmental and health implications of conventional farming, which is driving some consumers to seek out organic alternatives. In terms of market dynamics, the demand for organic orange pulp is expected to grow at a faster rate than conventional pulp, as more consumers prioritize health and sustainability in their purchasing decisions. However, the conventional segment still holds a significant share of the market due to its cost-effectiveness and established supply chains. Companies operating in the Global Orange Pulp Market are increasingly investing in organic production to capture this growing segment, while also working to improve the sustainability of conventional farming practices. This includes initiatives to reduce the use of synthetic chemicals, improve soil health, and enhance water conservation. The choice between organic and conventional orange pulp ultimately depends on consumer preferences, price sensitivity, and availability, with both segments playing important roles in the overall market landscape.

Online Sales, Offline Sales in the Global Orange Pulp Market:

The Global Orange Pulp Market serves a variety of sales channels, with online and offline sales being the primary methods of distribution. Online sales have gained significant traction in recent years, driven by the convenience and accessibility of e-commerce platforms. Consumers can easily browse and purchase orange pulp products from the comfort of their homes, with the added benefit of home delivery. This channel is particularly appealing to tech-savvy consumers and those living in urban areas with limited access to physical stores. Online sales also offer companies the opportunity to reach a wider audience, as they are not limited by geographical boundaries. Additionally, e-commerce platforms often provide detailed product information and customer reviews, which can help consumers make informed purchasing decisions. On the other hand, offline sales remain a dominant channel in the Global Orange Pulp Market, particularly in regions where internet penetration is low or consumers prefer the tactile experience of shopping in physical stores. Supermarkets, hypermarkets, and specialty food stores are common offline retail outlets for orange pulp products. These stores offer consumers the opportunity to physically inspect products before purchase, which can be an important factor for those concerned about quality and freshness. Offline sales also benefit from impulse purchases, as consumers may be more likely to buy orange pulp products when they see them on display. Furthermore, offline sales channels often provide opportunities for in-store promotions and sampling, which can drive consumer interest and increase sales. Despite the growth of online sales, offline sales continue to play a crucial role in the distribution of orange pulp products, particularly in regions with strong retail infrastructure. Companies in the Global Orange Pulp Market are increasingly adopting an omnichannel approach, integrating both online and offline sales strategies to maximize reach and cater to diverse consumer preferences. This approach allows companies to leverage the strengths of each channel, providing consumers with a seamless shopping experience and ensuring that orange pulp products are readily available to meet demand.

Global Orange Pulp Market Outlook:

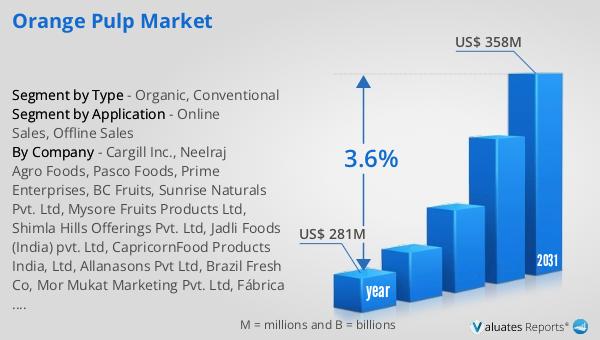

The global market for orange pulp was valued at approximately $281 million in 2024, and it is anticipated to expand to a revised size of around $358 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 3.6% over the forecast period. The steady increase in market size reflects the rising demand for orange pulp products across various regions, driven by consumer preferences for natural and healthy food options. The market's growth is supported by the expanding applications of orange pulp in the food and beverage industry, as well as the increasing popularity of citrus fruits for their nutritional benefits. Companies operating in this market are focusing on innovation and sustainability to capture a larger share of the growing demand. This includes the development of new product formulations, improvements in processing technologies, and efforts to reduce the environmental impact of production. As the market continues to evolve, companies are also exploring new distribution channels and marketing strategies to reach a broader audience and enhance consumer engagement. The projected growth of the global orange pulp market underscores the importance of understanding consumer trends and adapting to changing preferences to remain competitive in this dynamic industry.

| Report Metric | Details |

| Report Name | Orange Pulp Market |

| Accounted market size in year | US$ 281 million |

| Forecasted market size in 2031 | US$ 358 million |

| CAGR | 3.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Cargill Inc., Neelraj Agro Foods, Pasco Foods, Prime Enterprises, BC Fruits, Sunrise Naturals Pvt. Ltd, Mysore Fruits Products Ltd, Shimla Hills Offerings Pvt. Ltd, Jadli Foods (India) pvt. Ltd, CapricornFood Products India, Ltd, Allanasons Pvt Ltd, Brazil Fresh Co, Mor Mukat Marketing Pvt. Ltd, Fábrica de Mermeladas, YESRAJ AGRO EXPORTS PVT. LTD |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |