What is Global Ambulatory EHR Systems Market?

The Global Ambulatory EHR Systems Market refers to the worldwide industry focused on electronic health record (EHR) systems specifically designed for outpatient care settings. These systems are crucial for managing patient information, streamlining workflows, and enhancing the quality of care in ambulatory settings such as clinics and outpatient departments. Unlike inpatient EHR systems, ambulatory EHRs are tailored to meet the unique needs of outpatient care, where patients do not stay overnight. They help healthcare providers efficiently document patient encounters, manage prescriptions, and coordinate care across different providers. The market for these systems has been growing steadily due to the increasing demand for digital healthcare solutions, driven by the need for improved patient outcomes, regulatory requirements, and the shift towards value-based care. As healthcare providers continue to adopt technology to enhance operational efficiency and patient care, the Global Ambulatory EHR Systems Market is expected to expand further, offering innovative solutions that cater to the evolving needs of the healthcare industry.

On-premise, Cloud-based in the Global Ambulatory EHR Systems Market:

In the Global Ambulatory EHR Systems Market, there are two primary deployment models: on-premise and cloud-based systems. On-premise EHR systems are installed and run on the healthcare provider's own servers and infrastructure. This model offers healthcare organizations greater control over their data and systems, as they are responsible for maintaining and securing their own servers. On-premise systems can be customized to meet the specific needs of the organization, allowing for tailored solutions that align with existing workflows and processes. However, this model also requires significant upfront investment in hardware and IT resources, as well as ongoing maintenance and support costs. Additionally, on-premise systems may require more time and effort to implement and update, as organizations must manage these processes internally. On the other hand, cloud-based EHR systems are hosted on remote servers and accessed via the internet. This model offers several advantages, including lower upfront costs, as there is no need to invest in expensive hardware or IT infrastructure. Cloud-based systems are typically offered on a subscription basis, allowing healthcare providers to pay for only the services they need. This model also provides greater flexibility and scalability, as organizations can easily adjust their usage and storage needs as they grow. Cloud-based systems are often easier to implement and update, as the vendor is responsible for maintaining and upgrading the software. This allows healthcare providers to focus on patient care rather than IT management. One of the key benefits of cloud-based EHR systems is their ability to facilitate data sharing and collaboration among healthcare providers. With data stored in the cloud, authorized users can access patient information from any location with an internet connection, enabling seamless coordination of care across different providers and settings. This is particularly important in ambulatory care, where patients may receive care from multiple providers and need their information to be readily accessible. Cloud-based systems also offer enhanced data security, as vendors typically employ advanced security measures to protect sensitive patient information. This can help healthcare organizations comply with regulatory requirements and reduce the risk of data breaches. Despite the advantages of cloud-based systems, some healthcare providers may have concerns about data security and privacy, as well as potential downtime or service disruptions. To address these concerns, it is important for organizations to carefully evaluate potential vendors and choose a provider with a strong track record of security and reliability. Additionally, healthcare providers should ensure that their chosen system complies with relevant regulations and standards, such as the Health Insurance Portability and Accountability Act (HIPAA) in the United States. In conclusion, both on-premise and cloud-based EHR systems have their own advantages and challenges. On-premise systems offer greater control and customization, but require significant investment and resources to maintain. Cloud-based systems provide flexibility, scalability, and ease of use, but may raise concerns about data security and privacy. Ultimately, the choice between these two models will depend on the specific needs and priorities of the healthcare organization. As the Global Ambulatory EHR Systems Market continues to evolve, it is likely that we will see further innovation and development in both deployment models, offering healthcare providers a range of options to meet their unique needs.

Hospitals, Clinics, Others in the Global Ambulatory EHR Systems Market:

The Global Ambulatory EHR Systems Market plays a crucial role in various healthcare settings, including hospitals, clinics, and other outpatient care facilities. In hospitals, ambulatory EHR systems are used to manage patient information for outpatient services, such as consultations, diagnostic tests, and follow-up appointments. These systems help streamline workflows by enabling healthcare providers to efficiently document patient encounters, manage prescriptions, and coordinate care across different departments. By providing a comprehensive view of a patient's medical history, ambulatory EHR systems can improve the quality of care and support better clinical decision-making. Additionally, these systems can help hospitals comply with regulatory requirements and participate in value-based care initiatives, which focus on improving patient outcomes and reducing healthcare costs. In clinics, ambulatory EHR systems are essential for managing patient information and streamlining administrative tasks. These systems enable healthcare providers to efficiently document patient visits, manage appointments, and process billing and insurance claims. By automating routine tasks and reducing paperwork, ambulatory EHR systems can help clinics improve operational efficiency and focus more on patient care. Additionally, these systems can facilitate communication and collaboration among healthcare providers, ensuring that patients receive coordinated and comprehensive care. For smaller clinics with limited resources, cloud-based EHR systems can be particularly beneficial, as they offer a cost-effective and scalable solution that can be easily adapted to meet the clinic's needs. Beyond hospitals and clinics, ambulatory EHR systems are also used in other outpatient care settings, such as urgent care centers, rehabilitation facilities, and specialty practices. In these settings, EHR systems help manage patient information, streamline workflows, and improve the quality of care. For example, in urgent care centers, ambulatory EHR systems can help providers quickly access patient information and document encounters, ensuring that patients receive timely and appropriate care. In rehabilitation facilities, these systems can support the coordination of care among different providers, helping to ensure that patients receive comprehensive and personalized treatment plans. In specialty practices, ambulatory EHR systems can help manage complex patient information and support specialized workflows, enabling providers to deliver high-quality care tailored to the unique needs of their patients. Overall, the Global Ambulatory EHR Systems Market is essential for improving the quality and efficiency of care in various outpatient settings. By providing healthcare providers with the tools they need to manage patient information, streamline workflows, and coordinate care, these systems can help improve patient outcomes and support the transition to value-based care. As the healthcare industry continues to evolve, the demand for innovative and effective ambulatory EHR solutions is expected to grow, driving further advancements in this important market.

Global Ambulatory EHR Systems Market Outlook:

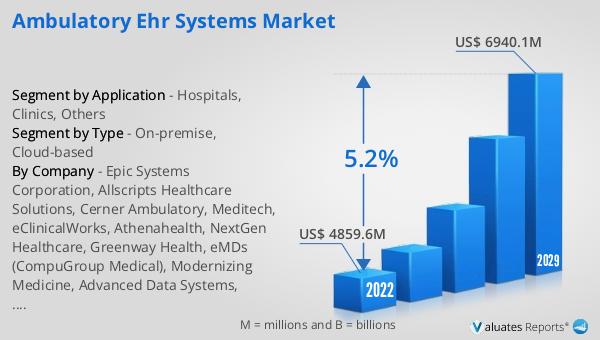

The worldwide market for Ambulatory EHR Systems was valued at $5,360 million in 2024 and is anticipated to expand to a revised size of $7,605 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.2% over the forecast period. Currently, 90% of hospitals have adopted ambulatory electronic health records to enhance the quality of care while also boosting the performance and efficiency of their staff, particularly in areas related to patient care and risk assessments. Our research indicates that the global market for medical devices is estimated to be valued at $603 billion in 2023, with an expected growth rate of 5% CAGR over the next six years. This growth is indicative of the increasing reliance on digital solutions to improve healthcare delivery and patient outcomes. As healthcare providers continue to embrace technology to streamline operations and enhance patient care, the market for ambulatory EHR systems is poised for significant growth, offering innovative solutions that cater to the evolving needs of the healthcare industry.

| Report Metric | Details |

| Report Name | Ambulatory EHR Systems Market |

| Accounted market size in year | US$ 5360 million |

| Forecasted market size in 2031 | US$ 7605 million |

| CAGR | 5.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Epic Systems Corporation, Allscripts Healthcare Solutions, Cerner Ambulatory, Meditech, eClinicalWorks, Athenahealth, NextGen Healthcare, Greenway Health, eMDs (CompuGroup Medical), Modernizing Medicine, Advanced Data Systems, Evident (CPSI), CureMD, Netsmart Technologies, Harris Healthcare, Praxis, GE Healthcare, Practice Fusion, ChartLogic, DrChrono, AdvancedMD, Amazing Charts, iPatientCare, Azalea Health, MEDHOST |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |