What is Global Automotive Testing and Validation Services Market?

The Global Automotive Testing and Validation Services Market is a crucial segment within the automotive industry, focusing on ensuring that vehicles meet safety, performance, and regulatory standards before they reach consumers. This market encompasses a wide range of services, including testing for durability, emissions, safety, and functionality. These services are essential for automotive manufacturers and component suppliers to validate the performance and reliability of their products. The market is driven by the increasing complexity of vehicles, which now incorporate advanced technologies such as electric drivetrains, autonomous driving systems, and connected car features. As a result, testing and validation services have become more sophisticated, requiring specialized equipment and expertise. The market is also influenced by stringent government regulations aimed at reducing emissions and improving vehicle safety, which necessitate rigorous testing procedures. Additionally, the growing consumer demand for high-quality, reliable vehicles further propels the need for comprehensive testing and validation services. Overall, the Global Automotive Testing and Validation Services Market plays a vital role in ensuring that vehicles are safe, efficient, and compliant with global standards, thereby supporting the automotive industry's growth and innovation.

Chassis Dynamometer, Engine Dynamometer, Vehicle Emission Test System, Wheel Alignment Tester in the Global Automotive Testing and Validation Services Market:

Chassis dynamometers, engine dynamometers, vehicle emission test systems, and wheel alignment testers are integral components of the Global Automotive Testing and Validation Services Market. Chassis dynamometers are used to simulate real-world driving conditions in a controlled environment, allowing manufacturers to test a vehicle's performance, fuel efficiency, and emissions. These devices are essential for evaluating how a vehicle will perform on the road, providing valuable data that can be used to optimize design and engineering. Engine dynamometers, on the other hand, focus specifically on the engine's performance. They measure parameters such as torque, power output, and fuel consumption, helping manufacturers fine-tune engine designs for better efficiency and performance. This is particularly important as the industry shifts towards more fuel-efficient and environmentally friendly powertrains. Vehicle emission test systems are critical for ensuring compliance with environmental regulations. These systems measure the pollutants emitted by a vehicle, such as carbon dioxide, nitrogen oxides, and particulate matter. With increasing regulatory pressure to reduce emissions, these tests are vital for manufacturers to certify that their vehicles meet the required standards. Wheel alignment testers are used to assess and adjust the alignment of a vehicle's wheels. Proper wheel alignment is crucial for vehicle safety, handling, and tire longevity. Misaligned wheels can lead to uneven tire wear, reduced fuel efficiency, and compromised handling, making this testing an important part of vehicle validation. Together, these testing systems provide a comprehensive approach to vehicle evaluation, ensuring that all aspects of a vehicle's performance and compliance are thoroughly assessed. As vehicles become more complex, with advanced electronics and autonomous features, the demand for sophisticated testing and validation services continues to grow. This growth is further supported by the increasing adoption of electric vehicles, which require specialized testing procedures to evaluate battery performance, range, and safety. In summary, chassis dynamometers, engine dynamometers, vehicle emission test systems, and wheel alignment testers are essential tools in the Global Automotive Testing and Validation Services Market, enabling manufacturers to deliver safe, efficient, and compliant vehicles to consumers.

Automotive Manufacturers, Automotive Component Manufacturers in the Global Automotive Testing and Validation Services Market:

The Global Automotive Testing and Validation Services Market is extensively utilized by both automotive manufacturers and automotive component manufacturers. For automotive manufacturers, these services are indispensable in the development and production of vehicles. They rely on testing and validation to ensure that their vehicles meet safety standards, perform reliably, and comply with environmental regulations. This involves a wide range of tests, from crash testing to emissions testing, each designed to evaluate different aspects of a vehicle's performance. By using these services, manufacturers can identify potential issues early in the development process, reducing the risk of costly recalls and enhancing the overall quality of their vehicles. For automotive component manufacturers, testing and validation services are equally important. These companies produce the parts and systems that make up a vehicle, such as engines, transmissions, brakes, and electronic systems. Each component must be rigorously tested to ensure it meets the required standards for performance, durability, and safety. This is particularly critical as vehicles become more complex, with components that must work seamlessly together. Testing and validation services help component manufacturers verify that their products will perform as expected in real-world conditions, providing assurance to both manufacturers and consumers. Additionally, these services support innovation by allowing manufacturers to test new technologies and designs in a controlled environment. This is essential for the development of advanced features such as autonomous driving systems, electric powertrains, and connected car technologies. By leveraging testing and validation services, automotive and component manufacturers can accelerate the development process, reduce time to market, and maintain a competitive edge in the rapidly evolving automotive industry. Overall, the Global Automotive Testing and Validation Services Market is a critical enabler of quality, safety, and innovation in the automotive sector, supporting manufacturers in delivering high-performance, reliable vehicles to consumers.

Global Automotive Testing and Validation Services Market Outlook:

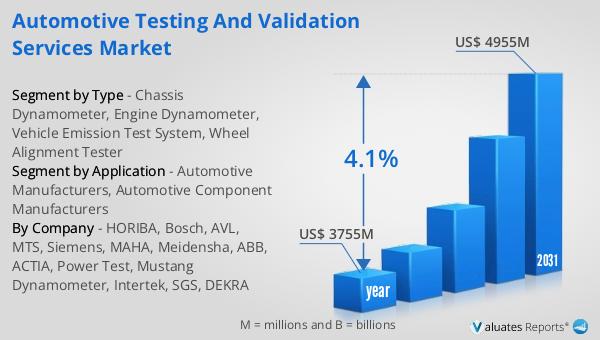

The global market for Automotive Testing and Validation Services was valued at $3,755 million in 2024 and is anticipated to expand to a revised size of $4,955 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.1% over the forecast period. Currently, over 90% of the world's automobiles are concentrated in the continents of Asia, Europe, and North America. Among these, Asia leads with 56% of the world's automobile production, followed by Europe at 20%, and North America at 16%. This distribution highlights the significant role these regions play in the global automotive industry, driving demand for testing and validation services. The growth in the market is fueled by the increasing complexity of vehicles, stringent regulatory requirements, and the need for manufacturers to ensure the safety, performance, and compliance of their products. As the automotive industry continues to evolve, with advancements in electric vehicles, autonomous driving, and connected technologies, the demand for comprehensive testing and validation services is expected to rise. This growth trajectory underscores the importance of the Global Automotive Testing and Validation Services Market in supporting the automotive industry's innovation and development.

| Report Metric | Details |

| Report Name | Automotive Testing and Validation Services Market |

| Accounted market size in year | US$ 3755 million |

| Forecasted market size in 2031 | US$ 4955 million |

| CAGR | 4.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | HORIBA, Bosch, AVL, MTS, Siemens, MAHA, Meidensha, ABB, ACTIA, Power Test, Mustang Dynamometer, Intertek, SGS, DEKRA |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |