What is Global Electrical Distribution System Market?

The Global Electrical Distribution System Market is a crucial component of the broader electrical infrastructure, responsible for delivering electricity from power generation facilities to end-users, including residential, commercial, and industrial sectors. This market encompasses a wide range of products and technologies designed to ensure the efficient and reliable distribution of electrical power. Key components include transformers, switchgear, circuit breakers, and distribution panels, which work together to manage and control the flow of electricity. The market is driven by the increasing demand for electricity, driven by urbanization, industrialization, and the growing adoption of renewable energy sources. Additionally, advancements in smart grid technologies and the integration of digital solutions are transforming the landscape of electrical distribution, enhancing efficiency, reliability, and sustainability. As the world continues to transition towards cleaner energy sources and smarter infrastructure, the Global Electrical Distribution System Market is poised for significant growth, playing a vital role in supporting the evolving energy needs of societies worldwide.

AC, DC, Others in the Global Electrical Distribution System Market:

The Global Electrical Distribution System Market is segmented into various types, including AC (Alternating Current), DC (Direct Current), and other systems, each serving distinct roles and applications. AC systems are the most prevalent in the market, primarily due to their ability to efficiently transmit electricity over long distances. This is achieved through the use of transformers, which can step up the voltage for transmission and step it down for distribution to end-users. AC systems are widely used in residential, commercial, and industrial settings, providing the backbone for most electrical infrastructure. They are favored for their cost-effectiveness and compatibility with existing grid systems. On the other hand, DC systems are gaining traction, particularly in specific applications where efficiency and reliability are paramount. DC systems are known for their ability to provide stable and consistent power, making them ideal for use in data centers, telecommunications, and renewable energy installations such as solar power systems. The rise of electric vehicles (EVs) has also spurred interest in DC systems, as they are integral to the charging infrastructure required for EVs. Additionally, DC microgrids are being explored as a means to enhance energy efficiency and resilience in localized settings. Beyond AC and DC, the market also includes other specialized systems designed to meet unique requirements. These may include hybrid systems that combine elements of both AC and DC, as well as advanced technologies like superconducting cables and wireless power transmission. These innovations are being driven by the need to address challenges such as energy losses, grid stability, and the integration of renewable energy sources. As the Global Electrical Distribution System Market continues to evolve, the interplay between AC, DC, and other systems will be crucial in shaping the future of electrical distribution. The ongoing development of smart grid technologies, energy storage solutions, and digitalization is expected to further enhance the capabilities and efficiency of these systems, paving the way for a more sustainable and resilient energy landscape.

Passenger Vehicles (PVs), Commercial Vehicles (CVs) in the Global Electrical Distribution System Market:

The Global Electrical Distribution System Market plays a pivotal role in the automotive industry, particularly in the context of Passenger Vehicles (PVs) and Commercial Vehicles (CVs). In passenger vehicles, the electrical distribution system is responsible for managing and distributing electrical power to various components and systems, including lighting, infotainment, climate control, and safety features. With the increasing complexity of modern vehicles, the demand for advanced electrical distribution systems has grown significantly. These systems are designed to ensure reliable power delivery, minimize energy losses, and support the integration of new technologies such as electric and hybrid powertrains. The shift towards electric vehicles (EVs) has further amplified the importance of efficient electrical distribution, as these vehicles rely heavily on electrical systems for propulsion and auxiliary functions. In commercial vehicles, the electrical distribution system is equally critical, supporting a wide range of applications from basic lighting and instrumentation to more complex systems like telematics, fleet management, and advanced driver-assistance systems (ADAS). The growing emphasis on fuel efficiency, emissions reduction, and vehicle connectivity has driven the need for more sophisticated electrical distribution solutions in commercial vehicles. This includes the integration of high-voltage systems for hybrid and electric commercial vehicles, as well as the adoption of smart technologies to optimize energy usage and enhance operational efficiency. As the automotive industry continues to evolve, the Global Electrical Distribution System Market is expected to play an increasingly important role in enabling the transition to cleaner, smarter, and more connected vehicles. The development of new materials, technologies, and design approaches will be key to meeting the diverse and evolving needs of both passenger and commercial vehicles, ensuring that electrical distribution systems remain a cornerstone of automotive innovation.

Global Electrical Distribution System Market Outlook:

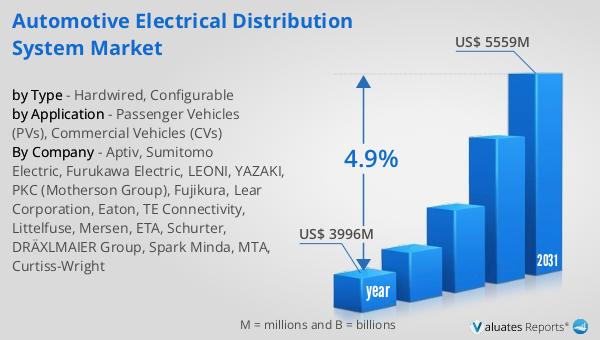

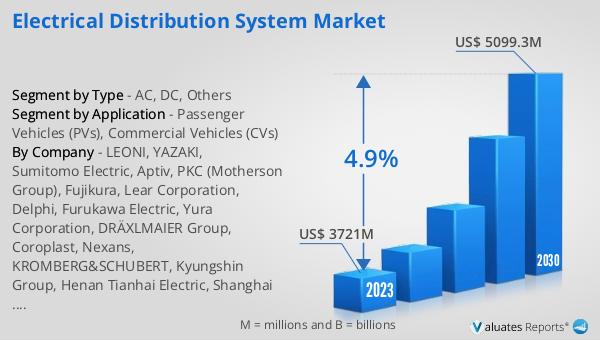

The global market for Electrical Distribution Systems was valued at approximately USD 3,996 million in 2024, and it is anticipated to expand to a revised size of around USD 5,559 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 4.9% over the forecast period. The market's expansion is driven by several factors, including the increasing demand for electricity, the integration of renewable energy sources, and advancements in smart grid technologies. As urbanization and industrialization continue to accelerate, the need for efficient and reliable electrical distribution systems becomes more critical. Additionally, the transition towards cleaner energy sources and the adoption of digital solutions are reshaping the landscape of electrical distribution, enhancing efficiency, reliability, and sustainability. The market's growth is also supported by the rising demand for electric vehicles, which require robust electrical distribution infrastructure for charging and operation. As the world continues to evolve towards a more sustainable and connected future, the Global Electrical Distribution System Market is poised to play a vital role in supporting the energy needs of societies worldwide.

| Report Metric | Details |

| Report Name | Electrical Distribution System Market |

| Accounted market size in year | US$ 3996 million |

| Forecasted market size in 2031 | US$ 5559 million |

| CAGR | 4.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | LEONI, YAZAKI, Sumitomo Electric, Aptiv, PKC (Motherson Group), Fujikura, Lear Corporation, Delphi, Furukawa Electric, Yura Corporation, DRÄXLMAIER Group, Coroplast, Nexans, KROMBERG&SCHUBERT, Kyungshin Group, Henan Tianhai Electric, Shanghai Jinting Automobile Harness |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |