What is Global Circular Power Connector Market?

The Global Circular Power Connector Market is a dynamic and essential segment of the electrical components industry, focusing on connectors that facilitate the transmission of electrical power in a circular form. These connectors are designed to provide a reliable and secure connection in various applications, ensuring efficient power distribution and minimizing the risk of disconnection or power loss. Circular power connectors are widely used due to their robust design, which can withstand harsh environmental conditions, making them suitable for both indoor and outdoor applications. They are commonly found in industries such as telecommunications, automotive, aerospace, and industrial machinery, where reliable power connections are critical. The market for these connectors is driven by the increasing demand for advanced electronic devices and the need for efficient power management solutions. As technology continues to evolve, the Global Circular Power Connector Market is expected to grow, driven by innovations in connector design and materials that enhance performance and durability. Manufacturers are focusing on developing connectors that offer higher power ratings, improved safety features, and compatibility with a wide range of devices and systems. This market is characterized by intense competition, with numerous players striving to offer the best solutions to meet the diverse needs of their customers.

Light-duty, Medium-duty, Heavy-duty in the Global Circular Power Connector Market:

In the Global Circular Power Connector Market, connectors are categorized into light-duty, medium-duty, and heavy-duty based on their application and capacity to handle different levels of electrical power. Light-duty circular power connectors are typically used in applications where the power requirements are relatively low, such as consumer electronics, small appliances, and portable devices. These connectors are designed to be compact and lightweight, making them ideal for use in devices where space is limited. They offer sufficient power transmission capabilities for low-power applications while ensuring safety and reliability. Light-duty connectors are often used in environments where they are not exposed to harsh conditions, as they may not have the same level of durability as their medium and heavy-duty counterparts. Medium-duty circular power connectors are used in applications that require a moderate level of power transmission, such as industrial equipment, medical devices, and telecommunications systems. These connectors are designed to provide a balance between size, power capacity, and durability, making them suitable for a wide range of applications. They are often used in environments where they may be exposed to moderate levels of vibration, moisture, or temperature fluctuations, and are built to withstand these conditions while maintaining a reliable connection. Medium-duty connectors are often equipped with features such as locking mechanisms and sealing to enhance their performance in challenging environments. Heavy-duty circular power connectors are designed for applications that require high levels of power transmission and are often used in industries such as aerospace, automotive, and heavy machinery. These connectors are built to withstand extreme conditions, including high levels of vibration, shock, and temperature variations. They are typically larger and more robust than light and medium-duty connectors, with enhanced features such as reinforced housings, advanced sealing technologies, and high-grade materials to ensure durability and reliability. Heavy-duty connectors are essential in applications where failure is not an option, as they provide a secure and stable connection even in the most demanding environments. The choice between light-duty, medium-duty, and heavy-duty circular power connectors depends on the specific requirements of the application, including the level of power transmission needed, the environmental conditions, and the space available for the connector. Manufacturers in the Global Circular Power Connector Market are continually innovating to develop connectors that meet the evolving needs of their customers, offering solutions that provide the right balance of size, power capacity, and durability for each application. As technology advances and the demand for reliable power connections grows, the market for circular power connectors is expected to expand, with new products and technologies emerging to meet the diverse needs of various industries.

Data Communications, Industrial and Instrumentation, Vehicle, Aerospace, Others in the Global Circular Power Connector Market:

The Global Circular Power Connector Market plays a crucial role in various sectors, including data communications, industrial and instrumentation, vehicles, aerospace, and others. In data communications, circular power connectors are essential for ensuring reliable power connections in networking equipment, servers, and data centers. These connectors are designed to provide stable power transmission, minimizing the risk of downtime and data loss. They are often used in environments where space is limited, and a compact, efficient power connection is required. In industrial and instrumentation applications, circular power connectors are used to provide power to machinery, control systems, and measurement devices. These connectors are designed to withstand harsh industrial environments, including exposure to dust, moisture, and vibration. They offer secure and reliable connections, ensuring that equipment operates efficiently and safely. In the vehicle sector, circular power connectors are used in automotive and transportation applications to provide power to various systems, including lighting, infotainment, and engine control. These connectors are designed to withstand the rigors of the automotive environment, including temperature fluctuations, vibration, and exposure to chemicals. They offer reliable connections that ensure the safe and efficient operation of vehicle systems. In the aerospace industry, circular power connectors are used in aircraft and spacecraft to provide power to critical systems, including navigation, communication, and control systems. These connectors are designed to meet stringent safety and performance standards, ensuring reliable connections in the demanding aerospace environment. They are built to withstand extreme conditions, including high levels of vibration, shock, and temperature variations. In addition to these sectors, circular power connectors are used in a variety of other applications, including medical devices, consumer electronics, and renewable energy systems. In each of these areas, circular power connectors provide reliable and efficient power connections, ensuring the safe and effective operation of equipment and systems. As technology continues to advance and the demand for reliable power connections grows, the Global Circular Power Connector Market is expected to expand, with new products and technologies emerging to meet the diverse needs of various industries.

Global Circular Power Connector Market Outlook:

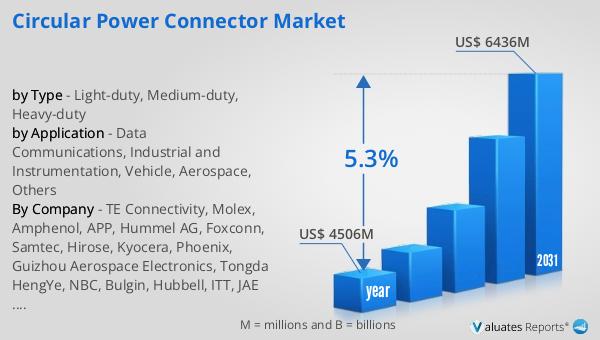

The outlook for the Global Circular Power Connector Market indicates a promising growth trajectory. In 2024, the market was valued at approximately US$ 4506 million, reflecting its significant role in various industries that rely on robust and efficient power connections. Looking ahead, the market is projected to reach an estimated size of US$ 6436 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.3% during the forecast period. This upward trend underscores the increasing demand for circular power connectors across different sectors, driven by the need for reliable and durable power solutions. The market's expansion is likely fueled by technological advancements and the continuous development of new applications that require efficient power transmission. As industries such as telecommunications, automotive, aerospace, and industrial machinery continue to evolve, the demand for high-performance circular power connectors is anticipated to rise. Manufacturers are expected to focus on innovation, developing connectors that offer enhanced performance, safety, and compatibility with a wide range of devices and systems. This growth trajectory highlights the importance of circular power connectors in supporting the technological advancements and operational efficiency of various industries, ensuring that they remain a critical component in the global market landscape.

| Report Metric | Details |

| Report Name | Circular Power Connector Market |

| Accounted market size in year | US$ 4506 million |

| Forecasted market size in 2031 | US$ 6436 million |

| CAGR | 5.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TE Connectivity, Molex, Amphenol, APP, Hummel AG, Foxconn, Samtec, Hirose, Kyocera, Phoenix, Guizhou Aerospace Electronics, Tongda HengYe, NBC, Bulgin, Hubbell, ITT, JAE Electronics, Omron, Jonhon, Souriau, Binder Group, Belden, CUI, Deren |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |