What is Global PV System Cables and Wires Market?

The Global PV System Cables and Wires Market refers to the worldwide industry focused on the production and distribution of cables and wires specifically designed for photovoltaic (PV) systems. These systems are used to convert sunlight into electricity, and the cables and wires play a crucial role in connecting various components of the solar power system, such as solar panels, inverters, and batteries. The market encompasses a wide range of products, including different types of cables and wires that are engineered to withstand harsh environmental conditions, such as UV radiation, temperature fluctuations, and moisture. As the demand for renewable energy sources continues to grow, the market for PV system cables and wires is expanding, driven by the increasing adoption of solar power installations in residential, commercial, and industrial sectors. This market is characterized by technological advancements aimed at improving the efficiency and durability of the cables and wires, as well as efforts to reduce costs and enhance the overall performance of solar power systems. The global PV system cables and wires market is a vital component of the renewable energy industry, supporting the transition to cleaner and more sustainable energy sources.

Copper Solar Cables, Aluminum Solar Cables, Other in the Global PV System Cables and Wires Market:

Copper solar cables are a fundamental component of the Global PV System Cables and Wires Market, known for their excellent conductivity and durability. Copper, being a highly conductive metal, ensures minimal energy loss during the transmission of electricity generated by solar panels. This makes copper solar cables a preferred choice for many solar power installations, especially in environments where efficiency and reliability are paramount. These cables are designed to withstand extreme weather conditions, including high temperatures and UV exposure, ensuring long-term performance and safety. Additionally, copper solar cables are flexible, making them easy to install and maintain, which is a significant advantage in complex solar power systems. On the other hand, aluminum solar cables offer a cost-effective alternative to copper cables. While aluminum is not as conductive as copper, it is significantly lighter and less expensive, making it an attractive option for large-scale solar installations where cost savings are a priority. Aluminum solar cables are also designed to resist environmental stressors, although they may require larger diameters to achieve the same conductivity as copper cables. This can sometimes lead to increased installation complexity. Despite these challenges, aluminum solar cables are gaining popularity in the market due to their affordability and adequate performance in many applications. In addition to copper and aluminum solar cables, the Global PV System Cables and Wires Market also includes other types of cables and wires that cater to specific needs and applications. These may include hybrid cables that combine different materials to optimize performance and cost, as well as specialized cables designed for unique environmental conditions or technical requirements. For instance, some cables are engineered to be highly resistant to chemical exposure or mechanical stress, making them suitable for industrial applications where harsh conditions are prevalent. The market also sees innovations in cable design, such as the development of thinner and more flexible cables that can be easily integrated into various solar power systems. These advancements are driven by the need to enhance the efficiency, reliability, and cost-effectiveness of solar power installations, ultimately supporting the broader adoption of renewable energy technologies. As the Global PV System Cables and Wires Market continues to evolve, the demand for high-quality, durable, and efficient cables and wires is expected to grow, reflecting the increasing importance of solar power in the global energy landscape.

Residential, Commercial, Industrial in the Global PV System Cables and Wires Market:

The usage of Global PV System Cables and Wires Market in residential, commercial, and industrial areas is pivotal to the effective deployment of solar power systems. In residential settings, PV system cables and wires are used to connect solar panels installed on rooftops to inverters and the home’s electrical system. These cables must be durable and safe, as they are often exposed to outdoor elements such as sunlight, rain, and wind. Homeowners rely on these cables to ensure that the electricity generated by their solar panels is efficiently transmitted to power their household appliances and reduce their reliance on the grid. The flexibility and ease of installation of these cables are crucial, as residential solar installations often involve navigating tight spaces and complex layouts. In commercial applications, PV system cables and wires are used in larger solar power installations, such as those found on office buildings, shopping centers, and other commercial properties. These installations require cables that can handle higher power capacities and longer distances, as they often involve connecting multiple solar panels spread across large areas. The cables used in commercial solar systems must be robust and reliable, capable of withstanding the demands of continuous operation and varying environmental conditions. Additionally, commercial solar installations often prioritize cost-effectiveness, making aluminum solar cables a popular choice due to their lower cost compared to copper cables. In industrial settings, the usage of PV system cables and wires is even more critical, as these installations often involve large-scale solar power systems designed to meet the energy needs of factories, warehouses, and other industrial facilities. The cables used in these applications must be capable of handling high voltages and currents, as well as being resistant to harsh environmental conditions such as extreme temperatures, chemical exposure, and mechanical stress. Industrial solar installations often require specialized cables that can meet stringent safety and performance standards, ensuring reliable and efficient energy transmission. The choice of cables in industrial applications is influenced by factors such as cost, performance, and the specific requirements of the installation site. Overall, the Global PV System Cables and Wires Market plays a crucial role in enabling the widespread adoption of solar power across residential, commercial, and industrial sectors, supporting the transition to a more sustainable energy future.

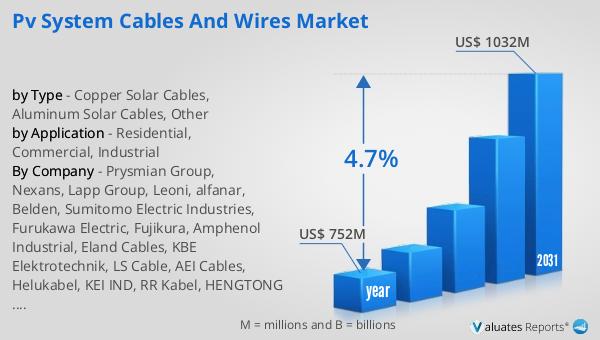

Global PV System Cables and Wires Market Outlook:

The global market for PV System Cables and Wires was valued at $752 million in 2024 and is anticipated to grow to a revised size of $1,032 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.7% during the forecast period. This growth is indicative of the increasing demand for renewable energy solutions and the critical role that PV system cables and wires play in the efficient transmission of solar-generated electricity. The market's expansion is driven by technological advancements, cost reductions, and the growing adoption of solar power systems across various sectors. According to the International Energy Agency, China's market share in all key products of the supply chain has exceeded 80%, highlighting the country's dominant position in the global PV system cables and wires market. This significant market share underscores China's leadership in the production and distribution of solar power components, driven by its robust manufacturing capabilities and supportive government policies. As the global market continues to evolve, the demand for high-quality, durable, and efficient PV system cables and wires is expected to grow, reflecting the increasing importance of solar power in the global energy landscape. The market outlook suggests a positive trajectory for the industry, with opportunities for growth and innovation as the world transitions to cleaner and more sustainable energy sources.

| Report Metric | Details |

| Report Name | PV System Cables and Wires Market |

| Accounted market size in year | US$ 752 million |

| Forecasted market size in 2031 | US$ 1032 million |

| CAGR | 4.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Prysmian Group, Nexans, Lapp Group, Leoni, alfanar, Belden, Sumitomo Electric Industries, Furukawa Electric, Fujikura, Amphenol Industrial, Eland Cables, KBE Elektrotechnik, LS Cable, AEI Cables, Helukabel, KEI IND, RR Kabel, HENGTONG OPTIC-ELECTRIC Co., Ltd., Jiangsu Zhongtian Technology, Catic Baosheng Electric, FAR EAST Cable Co., Ltd., WANMA Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |