What is Global Business Password Manager Market?

The Global Business Password Manager Market is a rapidly evolving sector that focuses on providing solutions to securely store and manage passwords for businesses worldwide. As organizations increasingly rely on digital platforms and online services, the need for robust password management systems has become critical. These systems help businesses protect sensitive information, streamline access to various applications, and enhance overall cybersecurity. The market encompasses a range of software solutions designed to store, retrieve, and manage passwords efficiently. These solutions often include features like password generation, encryption, and secure sharing among team members. With the rise in cyber threats and data breaches, businesses are prioritizing password security, driving the demand for advanced password management tools. The market is characterized by a mix of established players and innovative startups, each offering unique features to cater to different business needs. As technology continues to advance, the Global Business Password Manager Market is expected to grow, offering more sophisticated and user-friendly solutions to meet the evolving security demands of businesses across various industries.

On-premises, Cloud Based in the Global Business Password Manager Market:

In the Global Business Password Manager Market, solutions are typically categorized into two main types: on-premises and cloud-based. On-premises password managers are installed and run on a company's own servers and infrastructure. This type of solution offers businesses complete control over their data, as everything is stored locally within the organization’s IT environment. Companies that prioritize data privacy and have stringent security policies often prefer on-premises solutions because they can tailor the security measures to their specific needs. However, maintaining an on-premises password manager requires significant IT resources, including hardware, software updates, and dedicated personnel to manage the system. This can be a costly and time-consuming endeavor, especially for smaller businesses with limited IT budgets. On the other hand, cloud-based password managers are hosted on the provider's servers and accessed via the internet. These solutions offer greater flexibility and scalability, allowing businesses to easily adjust their usage based on current needs. Cloud-based solutions are typically easier to deploy and manage, as the service provider handles updates, maintenance, and security. This can be particularly advantageous for businesses with limited IT resources, as it reduces the burden on internal teams. Additionally, cloud-based password managers often come with advanced features such as automatic backups, multi-device synchronization, and seamless integration with other cloud services. However, some businesses may have concerns about data privacy and security, as sensitive information is stored off-site on third-party servers. To address these concerns, many cloud-based providers implement robust security measures, including encryption and multi-factor authentication, to protect user data. Ultimately, the choice between on-premises and cloud-based password managers depends on a business's specific needs, resources, and security requirements. Both types of solutions have their own advantages and challenges, and businesses must carefully evaluate their options to determine the best fit for their organization. As the Global Business Password Manager Market continues to grow, we can expect to see further innovations and improvements in both on-premises and cloud-based solutions, offering businesses more choices and enhanced security features.

Enterprise, Government, Association, Others in the Global Business Password Manager Market:

The usage of Global Business Password Manager Market solutions spans across various sectors, including enterprises, government, associations, and others, each with unique requirements and challenges. In the enterprise sector, password managers are essential tools for enhancing security and productivity. Large organizations often have numerous applications and systems that require secure access, and managing passwords manually can be cumbersome and risky. Password managers streamline this process by securely storing and autofilling credentials, reducing the risk of password-related breaches. They also facilitate secure password sharing among team members, ensuring that sensitive information is only accessible to authorized personnel. In government sectors, password managers play a crucial role in safeguarding sensitive data and maintaining compliance with stringent security regulations. Government agencies handle vast amounts of confidential information, and a breach could have severe consequences. Password managers help mitigate these risks by enforcing strong password policies, providing audit trails, and ensuring that access to sensitive systems is tightly controlled. Associations, which often operate with limited resources, benefit from password managers by improving security without the need for extensive IT infrastructure. These organizations can leverage password management solutions to protect member data, streamline operations, and enhance collaboration among staff and volunteers. Finally, other sectors, such as healthcare, education, and non-profits, also utilize password managers to address their specific security needs. In healthcare, for example, password managers help protect patient data and comply with regulations like HIPAA. Educational institutions use these tools to secure student and faculty information, while non-profits rely on them to safeguard donor data and streamline operations. Overall, the Global Business Password Manager Market provides valuable solutions for a wide range of sectors, helping organizations enhance security, improve efficiency, and reduce the risk of data breaches.

Global Business Password Manager Market Outlook:

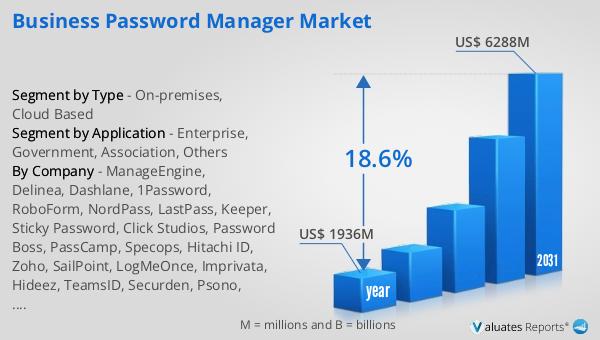

The outlook for the Global Business Password Manager Market indicates significant growth in the coming years. In 2024, the market was valued at approximately $1,936 million. By 2031, it is anticipated to expand to a revised size of around $6,288 million. This growth trajectory represents a compound annual growth rate (CAGR) of 18.6% over the forecast period. Such a robust growth rate underscores the increasing importance of password management solutions in today's digital landscape. As businesses continue to digitize their operations and rely more heavily on online platforms, the need for secure and efficient password management becomes paramount. The rising incidence of cyber threats and data breaches further fuels the demand for advanced password management tools. Organizations across various sectors are recognizing the critical role that password managers play in safeguarding sensitive information and ensuring compliance with security regulations. This growing awareness, coupled with technological advancements and the introduction of innovative features, is driving the expansion of the Global Business Password Manager Market. As the market evolves, businesses can expect to see more sophisticated solutions that offer enhanced security, user-friendliness, and integration capabilities, further solidifying the importance of password managers in the digital age.

| Report Metric | Details |

| Report Name | Business Password Manager Market |

| Accounted market size in year | US$ 1936 million |

| Forecasted market size in 2031 | US$ 6288 million |

| CAGR | 18.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | ManageEngine, Delinea, Dashlane, 1Password, RoboForm, NordPass, LastPass, Keeper, Sticky Password, Click Studios, Password Boss, PassCamp, Specops, Hitachi ID, Zoho, SailPoint, LogMeOnce, Imprivata, Hideez, TeamsID, Securden, Psono, Rippling, BeyondTrust, Keeper Security, Hitachi, Nord Security, Bitwarden, Passportal, Siber Systems |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |