What is Global Bakery Confectionary Machinery Market?

The Global Bakery Confectionary Machinery Market is a specialized segment within the broader food processing equipment industry, focusing on machinery used in the production of bakery and confectionery products. This market encompasses a wide range of equipment designed to streamline and enhance the production processes of baked goods and sweets, including bread, pastries, cakes, cookies, and chocolates. The machinery involved ranges from mixers and ovens to packaging and cooling systems, each playing a crucial role in ensuring efficiency, consistency, and quality in production. The demand for such machinery is driven by the growing consumer preference for baked and confectionery products, coupled with the need for automation and technological advancements in the food processing industry. As consumer tastes evolve and the demand for diverse and high-quality bakery products increases, manufacturers are investing in innovative machinery solutions to meet these needs. This market is characterized by continuous innovation, with companies striving to develop equipment that not only enhances productivity but also reduces energy consumption and minimizes waste. The Global Bakery Confectionary Machinery Market is thus a dynamic and essential component of the food industry, supporting the production of a wide array of beloved bakery and confectionery items worldwide.

Bread Lines, Croissant Lines, Pastry Make Up Lines, Flatbread and Pizza Lines, Others in the Global Bakery Confectionary Machinery Market:

Bread Lines, Croissant Lines, Pastry Make Up Lines, Flatbread and Pizza Lines, and other machinery types are integral components of the Global Bakery Confectionary Machinery Market, each serving a specific purpose in the production of various bakery products. Bread Lines are designed to automate the bread-making process, from mixing and kneading the dough to shaping, proofing, and baking. These lines are equipped with advanced technology to ensure uniformity and quality in bread production, catering to both artisanal and mass production needs. Croissant Lines, on the other hand, are specialized for the production of croissants and other laminated dough products. These lines handle the delicate process of dough lamination, which involves folding and rolling the dough with layers of butter to create the flaky texture characteristic of croissants. Pastry Make Up Lines are versatile systems used for producing a wide range of pastries, including Danish pastries, puff pastries, and other filled or topped products. These lines are equipped with various tools and attachments to shape, fill, and decorate pastries, allowing for creativity and customization in product offerings. Flatbread and Pizza Lines are designed to produce flatbreads, pizzas, and similar products, focusing on dough handling, shaping, and baking processes. These lines are often equipped with stone or conveyor ovens to achieve the desired texture and flavor profiles. Other machinery types in this market include equipment for producing cakes, cookies, and chocolates, each tailored to the specific requirements of these products. The diversity of machinery in the Global Bakery Confectionary Machinery Market reflects the wide array of bakery and confectionery products available, each requiring specialized equipment to ensure quality and efficiency in production. As consumer preferences continue to evolve, manufacturers are constantly innovating to develop machinery that can accommodate new product trends and production techniques, ensuring that the market remains dynamic and responsive to industry needs.

Industrial Use, Commercial Use in the Global Bakery Confectionary Machinery Market:

The Global Bakery Confectionary Machinery Market finds extensive usage in both industrial and commercial settings, each with distinct requirements and applications. In industrial use, the machinery is employed in large-scale production facilities where efficiency, speed, and consistency are paramount. These facilities often produce bakery and confectionery products in bulk, supplying to supermarkets, retail chains, and food service providers. Industrial bakery machinery is designed to handle high volumes of production, with features such as automated mixing, proofing, baking, and packaging systems that streamline the entire production process. The focus in industrial settings is on maximizing output while maintaining product quality and minimizing waste. Advanced technologies, such as programmable logic controllers (PLCs) and human-machine interfaces (HMIs), are often integrated into industrial machinery to enhance automation and control, allowing for precise monitoring and adjustment of production parameters. In commercial use, bakery confectionary machinery is utilized in smaller-scale operations, such as bakeries, cafes, and restaurants. These establishments prioritize flexibility and versatility in their machinery, as they often produce a diverse range of products in smaller batches. Commercial bakery machinery is designed to be user-friendly and adaptable, allowing operators to easily switch between different products and recipes. The focus in commercial settings is on delivering high-quality, artisanal products that cater to specific customer preferences. As such, commercial machinery often includes features that allow for customization and creativity in product offerings, such as adjustable settings for dough thickness, filling quantities, and baking times. Both industrial and commercial users of bakery confectionary machinery benefit from ongoing advancements in technology, which continue to enhance the efficiency, quality, and sustainability of production processes. As the demand for bakery and confectionery products continues to grow, the Global Bakery Confectionary Machinery Market plays a crucial role in supporting the diverse needs of both industrial and commercial producers, ensuring that they can meet consumer expectations and remain competitive in the market.

Global Bakery Confectionary Machinery Market Outlook:

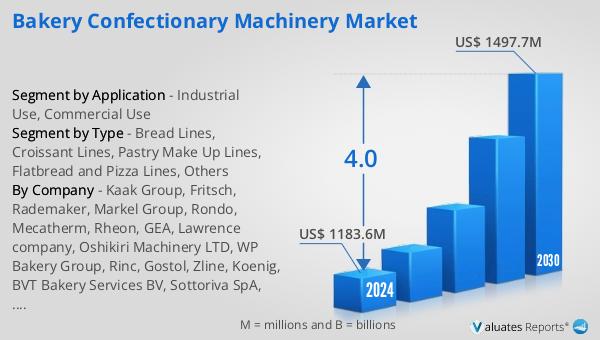

The global market for Bakery Confectionary Machinery was valued at $1,226 million in 2024 and is anticipated to expand to a revised size of $1,607 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.0% over the forecast period. This growth trajectory underscores the increasing demand for bakery and confectionery products worldwide, driven by evolving consumer preferences and the rising popularity of convenience foods. Europe stands out in this market, capturing a significant 40% share of global sales. This remarkable market share highlights Europe's strong presence and influence in the bakery confectionary machinery industry. The region's dominance can be attributed to its rich culinary heritage, high consumption of bakery products, and the presence of numerous established manufacturers and suppliers. European companies are known for their innovation and quality in machinery production, which has helped them maintain a competitive edge in the global market. As the market continues to evolve, Europe is expected to remain a key player, contributing significantly to the growth and development of the Global Bakery Confectionary Machinery Market. This market outlook reflects the dynamic nature of the industry, with continuous advancements in technology and changing consumer demands shaping its future trajectory.

| Report Metric | Details |

| Report Name | Bakery Confectionary Machinery Market |

| Accounted market size in year | US$ 1226 million |

| Forecasted market size in 2031 | US$ 1607 million |

| CAGR | 4.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Kaak Group, Fritsch, Rademaker, Markel Group, Rondo, Mecatherm, Rheon, GEA, Lawrence company, Oshikiri Machinery LTD, WP Bakery Group, Rinc, Gostol, Zline, Koenig, BVT Bakery Services BV, Sottoriva SpA, Canol Srl |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |