What is Global Managed Vulnerability Scanning Service Market?

The Global Managed Vulnerability Scanning Service Market is a rapidly evolving sector that focuses on providing organizations with comprehensive solutions to identify, assess, and manage security vulnerabilities in their IT infrastructure. This market encompasses a range of services designed to help businesses protect their digital assets from potential threats and cyber-attacks. Managed vulnerability scanning services are typically offered by third-party providers who specialize in cybersecurity. These services involve the use of advanced tools and technologies to scan networks, systems, and applications for vulnerabilities that could be exploited by malicious actors. The primary goal is to proactively identify and address security weaknesses before they can be exploited, thereby reducing the risk of data breaches and other cyber incidents. As organizations increasingly rely on digital technologies and face growing cyber threats, the demand for managed vulnerability scanning services is expected to continue to rise. This market is characterized by a diverse range of service offerings, including on-premises and cloud-based solutions, tailored to meet the specific needs of different industries and organizations.

On-premises Vulnerability Scanning, Cloud-based Vulnerability Scanning in the Global Managed Vulnerability Scanning Service Market:

On-premises vulnerability scanning refers to the process of conducting security assessments within an organization's own IT environment. This approach involves deploying scanning tools and technologies directly on the organization's network, allowing for a more controlled and customized scanning process. On-premises solutions are often preferred by organizations with strict data privacy and compliance requirements, as they provide greater control over the scanning process and data management. These solutions are typically managed by the organization's internal IT or security team, who are responsible for configuring and maintaining the scanning tools, analyzing the results, and implementing necessary security measures. On-premises vulnerability scanning offers several advantages, including the ability to tailor the scanning process to the organization's specific needs and the ability to integrate with existing security infrastructure. However, it also requires significant resources and expertise to manage effectively, which can be a challenge for smaller organizations with limited IT capabilities.

Finance, Bank, Telecommunications, Data Center, Other in the Global Managed Vulnerability Scanning Service Market:

Cloud-based vulnerability scanning, on the other hand, involves conducting security assessments using tools and technologies hosted in the cloud. This approach offers several benefits, including scalability, flexibility, and ease of deployment. Cloud-based solutions are typically managed by third-party providers who specialize in cybersecurity, allowing organizations to leverage their expertise and resources without the need for significant in-house capabilities. These solutions are particularly well-suited for organizations with dynamic and distributed IT environments, as they can easily scale to accommodate changes in the organization's infrastructure. Cloud-based vulnerability scanning also offers the advantage of continuous monitoring, allowing organizations to receive real-time alerts and updates on potential security threats. However, it also raises concerns about data privacy and compliance, as sensitive information may be transmitted and stored in the cloud. Organizations must carefully evaluate the security measures and certifications of their chosen cloud provider to ensure that their data is adequately protected.

Global Managed Vulnerability Scanning Service Market Outlook:

The Global Managed Vulnerability Scanning Service Market plays a crucial role in several key industries, including finance, banking, telecommunications, data centers, and others. In the finance and banking sectors, these services are essential for protecting sensitive financial data and ensuring compliance with stringent regulatory requirements. Financial institutions are prime targets for cybercriminals due to the valuable data they hold, making robust vulnerability scanning services a critical component of their cybersecurity strategy. In the telecommunications industry, managed vulnerability scanning services help protect the vast networks and infrastructure that support communication services. These services are vital for identifying and addressing vulnerabilities that could disrupt service delivery or compromise customer data. Data centers, which house vast amounts of sensitive information for various organizations, also rely heavily on managed vulnerability scanning services to maintain the security and integrity of their systems. These services help data centers identify potential security weaknesses and implement necessary measures to protect against data breaches and other cyber threats. Other industries, such as healthcare, retail, and manufacturing, also benefit from managed vulnerability scanning services, as they help protect sensitive data and ensure compliance with industry-specific regulations.

| Report Metric | Details |

| Report Name | Managed Vulnerability Scanning Service Market |

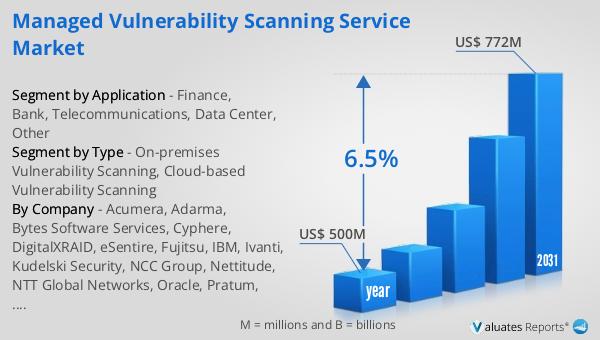

| Accounted market size in year | US$ 500 million |

| Forecasted market size in 2031 | US$ 772 million |

| CAGR | 6.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Acumera, Adarma, Bytes Software Services, Cyphere, DigitalXRAID, eSentire, Fujitsu, IBM, Ivanti, Kudelski Security, NCC Group, Nettitude, NTT Global Networks, Oracle, Pratum, Redscan, Root Group, Trapp Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |