What is Global Veterinary SpO2 Sensor Market?

The Global Veterinary SpO2 Sensor Market is a specialized segment within the broader veterinary equipment industry, focusing on devices that measure the oxygen saturation levels in the blood of animals. These sensors are crucial for monitoring the health and well-being of animals, particularly during surgical procedures or in critical care situations. The market encompasses a variety of sensor types, each designed to cater to different anatomical sites and species, ensuring accurate and reliable readings. As pet ownership continues to rise globally, so does the demand for advanced veterinary care, driving the growth of this market. The sensors are used in various settings, including veterinary hospitals, animal clinics, and research facilities, highlighting their versatility and importance in modern veterinary medicine. With technological advancements, these sensors are becoming more sophisticated, offering features such as wireless connectivity and enhanced accuracy, which further fuels their adoption. The market's growth is also supported by increasing awareness among pet owners about the importance of regular health check-ups and the role of SpO2 sensors in maintaining animal health. Overall, the Global Veterinary SpO2 Sensor Market is poised for significant expansion, driven by the growing emphasis on animal health and welfare.

Fingertip, Toe, Auricular, Tongue, Tail in the Global Veterinary SpO2 Sensor Market:

In the Global Veterinary SpO2 Sensor Market, various types of sensors are utilized to cater to the diverse anatomical structures of different animals. Fingertip sensors are commonly used for smaller animals or those with accessible extremities. These sensors are designed to fit snugly on the animal's finger or paw, providing accurate readings of blood oxygen levels. They are particularly useful in situations where quick and non-invasive monitoring is required. Toe sensors, similar in function to fingertip sensors, are used for animals where the toes are more accessible than the fingers. These sensors are often employed in veterinary practices dealing with larger animals, such as dogs or cats, where the toes provide a convenient site for measurement. Auricular sensors are designed for placement on the ear, a site that offers a rich blood supply and is often less intrusive for the animal. These sensors are ideal for animals with larger ears, such as rabbits or certain dog breeds, and provide reliable readings even in challenging conditions. Tongue sensors are another option, particularly useful for animals where other sites are not feasible. These sensors are placed on the tongue, taking advantage of the rich vascularization to obtain accurate oxygen saturation levels. They are often used in research settings or with animals that are difficult to handle. Tail sensors are specifically designed for animals with accessible tails, such as certain reptiles or small mammals. These sensors wrap around the tail, providing a secure fit and consistent readings. They are particularly useful in situations where other sites are not practical or when continuous monitoring is required. Each of these sensor types plays a crucial role in the Global Veterinary SpO2 Sensor Market, offering veterinarians and researchers the flexibility to choose the most appropriate tool for their specific needs. The diversity of sensor types ensures that animals of all sizes and species can be monitored effectively, contributing to better health outcomes and improved veterinary care. As the market continues to evolve, the development of new sensor technologies and designs will likely expand the range of options available, further enhancing the ability of veterinarians to provide high-quality care to their animal patients.

Veterinary Hospital, Animal Clinic, Others in the Global Veterinary SpO2 Sensor Market:

The usage of Global Veterinary SpO2 Sensors is widespread across various settings, including veterinary hospitals, animal clinics, and other specialized facilities. In veterinary hospitals, these sensors are an integral part of the monitoring equipment used during surgeries and critical care. They provide real-time data on an animal's oxygen saturation levels, allowing veterinarians to make informed decisions about anesthesia management and post-operative care. The ability to continuously monitor an animal's vital signs is crucial in these settings, as it helps prevent complications and ensures a higher standard of care. In animal clinics, SpO2 sensors are used for routine check-ups and diagnostic purposes. They offer a non-invasive method for assessing an animal's respiratory health, making them a valuable tool for veterinarians. By providing quick and accurate readings, these sensors enable early detection of potential health issues, allowing for timely intervention and treatment. This is particularly important in clinics where resources may be limited, and efficient patient management is essential. Beyond hospitals and clinics, SpO2 sensors are also used in research facilities and other specialized environments. In research settings, these sensors are used to monitor the health of animals involved in scientific studies, ensuring their well-being and compliance with ethical standards. They provide researchers with vital data that can inform study outcomes and contribute to advancements in veterinary medicine. Additionally, SpO2 sensors are used in wildlife rehabilitation centers and zoos, where they play a crucial role in monitoring the health of diverse animal species. The versatility and reliability of these sensors make them an indispensable tool in various veterinary applications, supporting the overall goal of improving animal health and welfare. As the Global Veterinary SpO2 Sensor Market continues to grow, the adoption of these devices in different settings is expected to increase, driven by the ongoing demand for high-quality veterinary care and the need for advanced monitoring solutions.

Global Veterinary SpO2 Sensor Market Outlook:

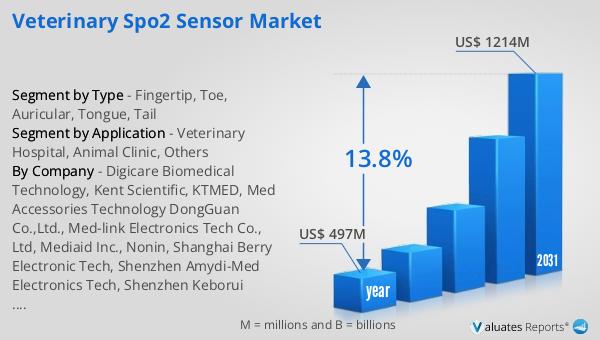

The global market for Veterinary SpO2 Sensors was valued at approximately $497 million in 2024, with projections indicating a significant growth trajectory. By 2031, the market is expected to reach a revised size of around $1,214 million, reflecting a robust compound annual growth rate (CAGR) of 13.8% over the forecast period. This growth is indicative of the increasing demand for advanced veterinary care and monitoring solutions. According to data from Our PET Supplies Research Center, the global pet industry experienced substantial growth, reaching $261 billion in 2022, marking an 11.3% increase from the previous year. This surge in the pet industry underscores the rising trend of pet ownership and the corresponding demand for high-quality veterinary services. As pet owners become more aware of the importance of regular health check-ups and the role of SpO2 sensors in maintaining animal health, the market for these devices is poised for continued expansion. The increasing emphasis on animal health and welfare, coupled with technological advancements in sensor design and functionality, is expected to drive further growth in the Global Veterinary SpO2 Sensor Market.

| Report Metric | Details |

| Report Name | Veterinary SpO2 Sensor Market |

| Accounted market size in year | US$ 497 million |

| Forecasted market size in 2031 | US$ 1214 million |

| CAGR | 13.8% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Digicare Biomedical Technology, Kent Scientific, KTMED, Med Accessories Technology DongGuan Co.,Ltd., Med-link Electronics Tech Co., Ltd, Mediaid Inc., Nonin, Shanghai Berry Electronic Tech, Shenzhen Amydi-Med Electronics Tech, Shenzhen Keborui Electronics Co., Ltd, Shenzhen Raysintone Technology Co.,Ltd, Shenzhen Medke Technology Co., Ltd, Smiths Medical Surgivet, Thames Medical, Medtronic, Shenzhen Pray-Med Technology Co.,Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |