What is Global 4-inch GaN Substrates Market?

The Global 4-inch GaN Substrates Market refers to the worldwide industry focused on the production and distribution of gallium nitride (GaN) substrates that are precisely 4 inches in diameter. GaN substrates are crucial components in the semiconductor industry, known for their superior electronic properties, such as high thermal conductivity, high breakdown voltage, and high electron mobility. These characteristics make them ideal for use in high-power and high-frequency applications. The market for these substrates is driven by the increasing demand for efficient power electronics, RF components, and optoelectronic devices. As industries like telecommunications, automotive, and consumer electronics continue to grow, the need for advanced materials like GaN substrates becomes more pronounced. The 4-inch size is particularly significant as it represents a balance between cost-effectiveness and performance, making it a popular choice for manufacturers looking to optimize production efficiency while maintaining high-quality standards. The market is characterized by ongoing research and development efforts aimed at improving substrate quality and reducing production costs, which are essential for meeting the evolving demands of various high-tech industries.

GaN Substrate on Sapphire, GaN Substrate on Si, GaN Substrate on SiC, GaN Substrate on GaN in the Global 4-inch GaN Substrates Market:

GaN substrates are versatile and can be grown on different materials, each offering unique advantages and challenges. GaN on Sapphire is one of the most common configurations due to sapphire's availability and cost-effectiveness. Sapphire provides a stable base for GaN growth, although it has a lattice mismatch with GaN, which can lead to defects in the crystal structure. Despite this, GaN on Sapphire is widely used in LED production, where the defects do not significantly impact performance. GaN on Silicon (Si) is another popular configuration, primarily because silicon is abundant and inexpensive. The integration of GaN with silicon substrates allows for the potential of combining GaN's superior electronic properties with silicon's well-established manufacturing processes. However, the lattice mismatch and thermal expansion differences between GaN and silicon pose challenges that require advanced engineering solutions. GaN on Silicon Carbide (SiC) offers a different set of advantages, particularly for high-power applications. SiC has a closer lattice match to GaN, which reduces defects and improves the performance of the resulting devices. This configuration is particularly beneficial for RF and power electronics, where efficiency and thermal management are critical. Lastly, GaN on GaN substrates represent the ideal scenario, as there is no lattice mismatch, resulting in high-quality crystals with minimal defects. This configuration is perfect for high-performance applications, but the cost of GaN substrates is significantly higher, limiting their widespread use. Each of these substrate configurations plays a vital role in the Global 4-inch GaN Substrates Market, catering to different industry needs and technological requirements.

Healthcare, Automotive, Military and Communication, General Lighting, Consumer Electronics, Telecom in the Global 4-inch GaN Substrates Market:

The Global 4-inch GaN Substrates Market finds applications across various sectors, each benefiting from the unique properties of GaN. In healthcare, GaN substrates are used in medical imaging devices and diagnostic equipment, where their high efficiency and reliability are crucial for accurate results. The automotive industry leverages GaN substrates for electric vehicles and advanced driver-assistance systems (ADAS), where they contribute to improved power efficiency and performance. In the military and communication sectors, GaN substrates are essential for radar systems and satellite communications, providing high-frequency operation and robustness in harsh environments. General lighting applications, such as LED lighting, benefit from GaN substrates due to their energy efficiency and long lifespan, making them a sustainable choice for both residential and commercial use. Consumer electronics, including smartphones and laptops, utilize GaN substrates in power adapters and chargers, where their compact size and fast charging capabilities are highly valued. In the telecom industry, GaN substrates are used in base stations and network infrastructure, supporting the growing demand for high-speed data transmission and connectivity. Each of these applications highlights the versatility and importance of GaN substrates in modern technology, driving the growth and innovation within the Global 4-inch GaN Substrates Market.

Global 4-inch GaN Substrates Market Outlook:

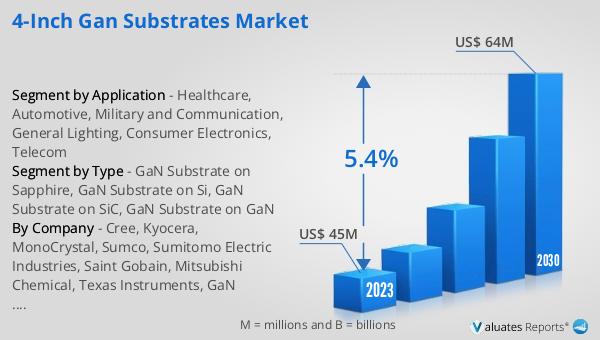

The global market for 4-inch GaN Substrates was valued at $49 million in 2024 and is anticipated to expand to a revised size of $70.4 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.4% over the forecast period. This growth trajectory underscores the increasing demand for GaN substrates across various industries, driven by their superior performance characteristics and the ongoing advancements in semiconductor technology. The market's expansion is fueled by the rising adoption of GaN-based devices in sectors such as telecommunications, automotive, and consumer electronics, where efficiency and performance are paramount. As industries continue to seek innovative solutions to meet the demands of modern technology, the role of GaN substrates becomes increasingly significant. The projected growth also highlights the importance of continued research and development efforts to enhance substrate quality and reduce production costs, ensuring that GaN substrates remain a competitive and viable option for manufacturers worldwide. This positive outlook for the Global 4-inch GaN Substrates Market reflects the broader trends in the semiconductor industry, where the pursuit of efficiency and performance drives innovation and market expansion.

| Report Metric | Details |

| Report Name | 4-inch GaN Substrates Market |

| Accounted market size in year | US$ 49 million |

| Forecasted market size in 2031 | US$ 70.4 million |

| CAGR | 5.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Cree, Kyocera, MonoCrystal, Sumco, Sumitomo Electric Industries, Saint Gobain, Mitsubishi Chemical, Texas Instruments, GaN Systems, MTI Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |