What is Global Semiconductor Digital Mass Flow Controller Market?

The Global Semiconductor Digital Mass Flow Controller Market is a specialized segment within the broader semiconductor industry, focusing on devices that precisely measure and control the flow of gases and liquids in semiconductor manufacturing processes. These controllers are crucial for ensuring the accuracy and efficiency of processes such as chemical vapor deposition, etching, and other fabrication steps that require precise gas flow control. The market for these controllers is driven by the increasing demand for semiconductors in various applications, including consumer electronics, automotive, and industrial sectors. As technology advances, the need for more sophisticated and reliable mass flow controllers grows, leading to innovations in digital control systems that offer enhanced precision and flexibility. The market is characterized by a mix of established players and new entrants, all striving to offer solutions that meet the evolving needs of semiconductor manufacturers. With the semiconductor industry poised for continued growth, the demand for digital mass flow controllers is expected to rise, making this market an essential component of the global semiconductor supply chain.

Thermal Type, Pressure Type in the Global Semiconductor Digital Mass Flow Controller Market:

In the Global Semiconductor Digital Mass Flow Controller Market, two primary types of controllers are prevalent: Thermal Type and Pressure Type. Thermal mass flow controllers operate based on the principle of heat transfer. They measure the flow of gas by detecting changes in temperature as the gas passes over a heated sensor. This type of controller is highly accurate and is widely used in applications where precise control of gas flow is critical. Thermal mass flow controllers are favored for their ability to handle a wide range of flow rates and their robustness in various environmental conditions. They are particularly useful in semiconductor processes that require stable and repeatable gas flow, such as chemical vapor deposition and etching. On the other hand, Pressure Type mass flow controllers measure flow based on the pressure drop across a restriction in the flow path. These controllers are often used in applications where the flow rate is relatively constant, and the primary concern is maintaining a specific pressure level. Pressure Type controllers are known for their simplicity and reliability, making them suitable for processes where the flow rate does not vary significantly. In the semiconductor industry, these controllers are often used in applications where maintaining a consistent pressure is more critical than precise flow measurement. Both Thermal and Pressure Type controllers have their unique advantages and are chosen based on the specific requirements of the semiconductor manufacturing process. As the demand for semiconductors continues to grow, the need for advanced mass flow controllers that can offer both precision and reliability becomes increasingly important. Manufacturers are continually innovating to develop controllers that can meet the stringent demands of modern semiconductor fabrication, ensuring that both Thermal and Pressure Type controllers remain integral to the industry.

Semiconductor Processing Furnace, PVD&CVD equipment, Etching equipment, Others in the Global Semiconductor Digital Mass Flow Controller Market:

The Global Semiconductor Digital Mass Flow Controller Market finds its applications in various critical areas of semiconductor manufacturing, including Semiconductor Processing Furnace, PVD&CVD equipment, Etching equipment, and others. In Semiconductor Processing Furnaces, digital mass flow controllers are essential for maintaining the precise flow of gases required for processes such as oxidation, diffusion, and annealing. These processes are crucial for altering the electrical properties of semiconductor materials, and any deviation in gas flow can lead to defects in the final product. Digital mass flow controllers ensure that the gas flow remains consistent and accurate, thereby enhancing the quality and yield of semiconductor devices. In PVD (Physical Vapor Deposition) and CVD (Chemical Vapor Deposition) equipment, mass flow controllers play a vital role in controlling the deposition of thin films on semiconductor wafers. These films are essential for creating the various layers of a semiconductor device, and precise control of gas flow is necessary to achieve the desired film thickness and composition. Digital mass flow controllers provide the accuracy and repeatability needed for these processes, ensuring that the films are deposited uniformly across the wafer. In Etching equipment, mass flow controllers are used to regulate the flow of etching gases that remove material from the wafer surface. This process is critical for defining the intricate patterns and structures on a semiconductor device. Accurate control of gas flow is essential to ensure that the etching process is uniform and does not damage the underlying layers. Digital mass flow controllers offer the precision required for these delicate processes, helping to improve the overall quality and performance of semiconductor devices. Beyond these specific applications, digital mass flow controllers are also used in other areas of semiconductor manufacturing, such as gas mixing and distribution systems. These controllers help maintain the correct gas composition and flow rates, ensuring that the manufacturing environment remains stable and conducive to high-quality semiconductor production. As the semiconductor industry continues to evolve, the demand for advanced digital mass flow controllers that can meet the stringent requirements of modern manufacturing processes is expected to grow.

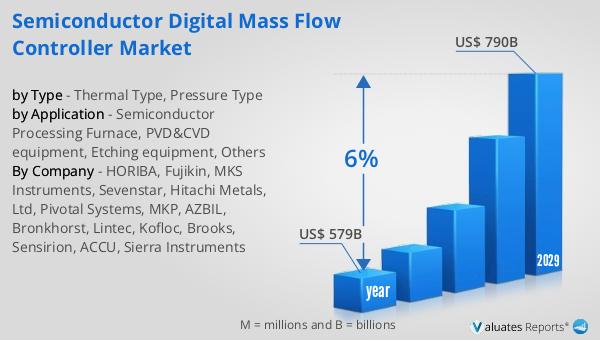

Global Semiconductor Digital Mass Flow Controller Market Outlook:

The global semiconductor market, valued at approximately $579 billion in 2022, is on a trajectory to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is driven by the increasing demand for semiconductors across various sectors, including consumer electronics, automotive, and industrial applications. As technology continues to advance, the need for more sophisticated and efficient semiconductor devices is rising, fueling the expansion of the market. The semiconductor industry is characterized by rapid innovation and intense competition, with companies constantly striving to develop new technologies and improve existing products. This dynamic environment presents both opportunities and challenges for market participants, as they seek to capitalize on emerging trends and address the evolving needs of their customers. The projected growth of the semiconductor market underscores the critical role that these devices play in modern society, powering everything from smartphones and computers to advanced automotive systems and industrial machinery. As the market continues to expand, the demand for high-quality, reliable semiconductors is expected to increase, driving further investment and innovation in the industry.

| Report Metric | Details |

| Report Name | Semiconductor Digital Mass Flow Controller Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | HORIBA, Fujikin, MKS Instruments, Sevenstar, Hitachi Metals, Ltd, Pivotal Systems, MKP, AZBIL, Bronkhorst, Lintec, Kofloc, Brooks, Sensirion, ACCU, Sierra Instruments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |