What is Global Liquid Milk Aseptic Packaging Market?

The Global Liquid Milk Aseptic Packaging Market refers to the industry focused on packaging liquid milk in a way that ensures it remains sterile and safe for consumption over an extended period without refrigeration. This market is driven by the need to extend the shelf life of milk, reduce spoilage, and maintain nutritional quality. Aseptic packaging involves a process where both the packaging and the milk are sterilized separately and then combined in a sterile environment. This method is particularly beneficial for regions with limited refrigeration infrastructure, as it allows milk to be stored and transported at room temperature. The market encompasses various packaging types, including cartons, bottles, and pouches, each designed to meet specific consumer preferences and logistical requirements. As consumer demand for convenient and long-lasting dairy products grows, the Global Liquid Milk Aseptic Packaging Market continues to expand, offering innovative solutions to meet these needs. The market's growth is also fueled by advancements in packaging technology and increased awareness of food safety and sustainability. Overall, this market plays a crucial role in the global dairy industry by ensuring that milk remains fresh and safe for consumption across diverse geographical regions.

Cup Type Aseptic Packaging, Bag Type Aseptic Packaging, Other in the Global Liquid Milk Aseptic Packaging Market:

Cup Type Aseptic Packaging is a popular choice within the Global Liquid Milk Aseptic Packaging Market due to its convenience and versatility. These cups are typically made from a combination of plastic and aluminum, providing a lightweight yet durable solution for milk packaging. The aseptic process ensures that the milk inside remains free from bacteria and other contaminants, allowing it to be stored at room temperature for extended periods. This type of packaging is particularly appealing to consumers who prefer single-serving portions, making it ideal for on-the-go consumption. Additionally, cup type packaging often includes features such as easy-open lids and resealable options, enhancing user convenience. On the other hand, Bag Type Aseptic Packaging offers a flexible and cost-effective alternative for liquid milk storage. These bags are usually made from multi-layered materials that provide excellent barrier properties, protecting the milk from light, oxygen, and moisture. Bag type packaging is often used for larger quantities of milk, making it suitable for family-sized servings or institutional use. The lightweight nature of bags also reduces transportation costs and environmental impact, aligning with the growing demand for sustainable packaging solutions. Other forms of aseptic packaging in the market include cartons and bottles, each offering unique benefits. Cartons, for instance, are widely recognized for their eco-friendly attributes, as they are often made from renewable resources and are recyclable. They provide a sturdy and protective barrier for milk, ensuring freshness and quality. Bottles, on the other hand, offer a familiar and user-friendly option for consumers, with the added advantage of being resealable and reusable. The choice of packaging type often depends on factors such as consumer preferences, distribution channels, and regional market trends. As the Global Liquid Milk Aseptic Packaging Market continues to evolve, manufacturers are exploring innovative materials and designs to enhance the functionality and sustainability of their products. This includes the development of biodegradable and compostable packaging options, as well as the incorporation of smart packaging technologies that provide real-time information on product freshness and quality. Overall, the diverse range of packaging types within the market reflects the industry's commitment to meeting the varied needs of consumers while addressing environmental concerns.

Room Temperature Milk, Low Temperature Milk in the Global Liquid Milk Aseptic Packaging Market:

The usage of Global Liquid Milk Aseptic Packaging Market in room temperature milk is a significant aspect of its application. Room temperature milk, also known as shelf-stable milk, is processed and packaged in a way that allows it to be stored without refrigeration until opened. This is achieved through the aseptic packaging process, which involves sterilizing the milk and the packaging separately before sealing them in a sterile environment. The result is a product that can be safely stored at room temperature for several months, making it an ideal choice for regions with limited access to refrigeration or for consumers seeking convenience. Room temperature milk is particularly popular in countries with warm climates, where maintaining a cold supply chain can be challenging. It is also favored by consumers who appreciate the extended shelf life and reduced risk of spoilage. The aseptic packaging used for room temperature milk typically includes cartons, bottles, and pouches, each designed to protect the milk from light, oxygen, and other external factors that could compromise its quality. In contrast, low temperature milk, also known as refrigerated milk, is processed and packaged to be stored at cooler temperatures. While aseptic packaging is not a requirement for low temperature milk, it can still be beneficial in extending the product's shelf life and ensuring safety. The aseptic process helps to eliminate harmful bacteria and microorganisms, reducing the risk of spoilage and enhancing the milk's nutritional value. For low temperature milk, aseptic packaging often involves the use of cartons and bottles that provide a robust barrier against external contaminants. These packaging solutions are designed to withstand the rigors of cold storage and transportation, ensuring that the milk remains fresh and safe for consumption. The choice between room temperature and low temperature milk often depends on consumer preferences, lifestyle, and regional market conditions. While room temperature milk offers the advantage of convenience and extended shelf life, low temperature milk is often perceived as fresher and more closely aligned with traditional dairy consumption habits. As the Global Liquid Milk Aseptic Packaging Market continues to grow, manufacturers are exploring ways to optimize packaging solutions for both room temperature and low temperature milk, balancing the need for convenience, safety, and sustainability. This includes the development of innovative materials and designs that enhance the functionality and environmental impact of packaging, as well as the incorporation of smart technologies that provide consumers with real-time information on product freshness and quality.

Global Liquid Milk Aseptic Packaging Market Outlook:

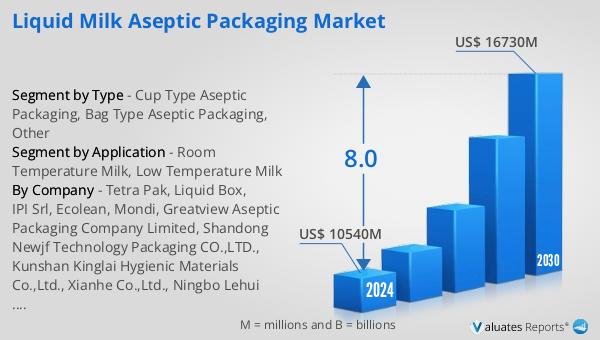

The outlook for the Global Liquid Milk Aseptic Packaging Market indicates a promising growth trajectory. According to projections, the market is expected to expand from a valuation of $10,540 million in 2024 to $16,730 million by 2030. This growth is anticipated to occur at a Compound Annual Growth Rate (CAGR) of 8.0% over the forecast period. This upward trend reflects the increasing demand for aseptic packaging solutions in the dairy industry, driven by factors such as the need for extended shelf life, food safety, and convenience. As consumers become more health-conscious and environmentally aware, there is a growing preference for packaging that not only preserves the quality and safety of milk but also minimizes environmental impact. The market's expansion is also supported by advancements in packaging technology, which have led to the development of innovative materials and designs that enhance the functionality and sustainability of aseptic packaging. Additionally, the rise in global population and urbanization has contributed to the increased consumption of dairy products, further fueling the demand for aseptic packaging solutions. As the market continues to evolve, manufacturers are likely to focus on optimizing their packaging offerings to meet the diverse needs of consumers and address emerging trends in the dairy industry.

| Report Metric | Details |

| Report Name | Liquid Milk Aseptic Packaging Market |

| Accounted market size in 2024 | US$ 10540 million |

| Forecasted market size in 2030 | US$ 16730 million |

| CAGR | 8.0 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Tetra Pak, Liquid Box, IPI Srl, Ecolean, Mondi, Greatview Aseptic Packaging Company Limited, Shandong Newjf Technology Packaging CO.,LTD., Kunshan Kinglai Hygienic Materials Co.,Ltd., Xianhe Co.,Ltd., Ningbo Lehui International Engineering Equipment Co.,ltd., Hangzhou Youngsun Intelligent Equipment Co.,Ltd., Xinjiang Western Animal Husbandry Co.,ltd., Guangdong Yantang Dairy Co.,Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |