What is Global AI Video Monitoring Chip Market?

The Global AI Video Monitoring Chip Market is a rapidly evolving sector that focuses on the development and deployment of specialized semiconductor chips designed to enhance video monitoring systems through artificial intelligence (AI). These chips are integral to processing and analyzing video data in real-time, enabling advanced functionalities such as facial recognition, object detection, and behavioral analysis. The market is driven by the increasing demand for intelligent surveillance systems across various industries, including security, automotive, and robotics. As AI technology continues to advance, these chips are becoming more sophisticated, offering improved processing power, energy efficiency, and integration capabilities. The global market for these chips is poised for significant growth, fueled by technological advancements and the rising need for enhanced security measures. Companies operating in this space are investing heavily in research and development to innovate and stay competitive. The market's expansion is also supported by the growing adoption of AI-driven solutions in emerging economies, where infrastructure development and urbanization are on the rise. Overall, the Global AI Video Monitoring Chip Market represents a dynamic and promising field with substantial opportunities for growth and innovation.

Front-end Chip, Back-end Chip in the Global AI Video Monitoring Chip Market:

In the Global AI Video Monitoring Chip Market, chips are typically categorized into two main types: front-end chips and back-end chips. Front-end chips are primarily responsible for capturing and processing raw video data from cameras and sensors. These chips are designed to handle high volumes of data with minimal latency, ensuring that video feeds are captured in real-time and with high fidelity. They often incorporate advanced image processing algorithms to enhance video quality, reduce noise, and adjust for varying lighting conditions. Front-end chips are crucial in applications where immediate data processing is required, such as in security cameras that need to quickly identify and track moving objects or individuals. On the other hand, back-end chips focus on analyzing and interpreting the processed video data. These chips leverage AI algorithms to perform complex tasks such as pattern recognition, anomaly detection, and predictive analytics. In security applications, back-end chips can identify potential threats by analyzing behavioral patterns and alerting authorities in real-time. In the automotive industry, they play a critical role in enabling autonomous driving features by interpreting video data from multiple sensors to make informed decisions. The integration of AI capabilities into back-end chips allows for more accurate and efficient data analysis, reducing the need for human intervention and enhancing overall system performance. Both front-end and back-end chips are essential components of AI video monitoring systems, working in tandem to deliver comprehensive and intelligent video analysis solutions. As the demand for AI-driven video monitoring continues to grow, the development of more advanced and specialized chips will be crucial in meeting the evolving needs of various industries.

Security, Autopilot, Robot, Other in the Global AI Video Monitoring Chip Market:

The Global AI Video Monitoring Chip Market finds extensive applications across several key areas, including security, autopilot systems, robotics, and other sectors. In the realm of security, AI video monitoring chips are revolutionizing surveillance systems by enabling real-time analysis of video feeds. These chips can detect unusual activities, recognize faces, and even predict potential security threats, thereby enhancing the effectiveness of security measures. In autopilot systems, particularly in the automotive industry, AI video monitoring chips are integral to the development of self-driving cars. They process video data from cameras and sensors to interpret the vehicle's surroundings, identify obstacles, and make real-time driving decisions. This capability is crucial for ensuring the safety and reliability of autonomous vehicles. In robotics, AI video monitoring chips enable robots to perceive and interact with their environment more intelligently. They allow robots to recognize objects, navigate complex terrains, and perform tasks with greater precision and autonomy. Beyond these areas, AI video monitoring chips are also being utilized in various other sectors, such as healthcare, where they assist in patient monitoring and diagnostic imaging, and in retail, where they enhance customer experience through personalized services and inventory management. The versatility and adaptability of AI video monitoring chips make them a valuable asset in numerous applications, driving innovation and efficiency across different industries.

Global AI Video Monitoring Chip Market Outlook:

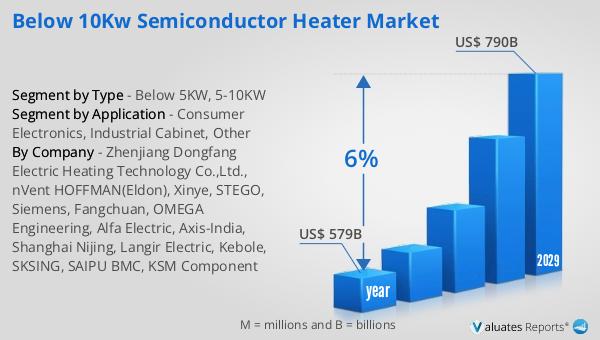

The outlook for the Global AI Video Monitoring Chip Market indicates a robust growth trajectory, with projections suggesting an increase from $5,061 million in 2024 to $10,430 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 12.8% over the forecast period. This expansion reflects the increasing demand for AI-enhanced video monitoring solutions across various sectors. In parallel, the broader semiconductor market, which was valued at $579 billion in 2022, is anticipated to reach $790 billion by 2029, growing at a CAGR of 6%. This growth in the semiconductor market underscores the rising importance of advanced chips in powering next-generation technologies. The synergy between the AI video monitoring chip market and the overall semiconductor industry highlights the critical role of these chips in driving technological advancements and meeting the evolving needs of industries worldwide. As AI continues to permeate various aspects of daily life and business operations, the demand for specialized chips that can efficiently process and analyze video data is expected to rise, further fueling market growth. The outlook for the Global AI Video Monitoring Chip Market is promising, with significant opportunities for innovation and expansion in the coming years.

| Report Metric | Details |

| Report Name | AI Video Monitoring Chip Market |

| Accounted market size in 2024 | US$ 5061 in million |

| Forecasted market size in 2030 | US$ 10430 million |

| CAGR | 12.8 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Qualcomm, STMicroelectronics, Marvell, Texas Instruments, AMBARELLA TAIWAN LTD., Intel, Samsung, Sony, Nextchip Co. Ltd., Hailo, Omnivision, Hisilicon, NXP Semiconductors Taiwan Ltd., Sigmastar Technology Ltd, Ingenic Semiconductor Co.,Ltd., Hunan Goke Microelectronics Co.,Ltd., Shanghai Fullhan Microelectronics Co.,Ltd., Uniview Technologies Co.,Ltd., Vimicro, Grain Media Inc., Corerain, All Winner Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |