What is Global Portable Household Dehumidifier Market?

The Global Portable Household Dehumidifier Market refers to the industry focused on the production and sale of portable devices designed to reduce humidity levels in residential spaces. These dehumidifiers are essential for maintaining indoor air quality, preventing mold growth, and ensuring comfort in homes, especially in regions with high humidity. The market encompasses a variety of dehumidifiers, each catering to different consumer needs and preferences. Factors driving the market include increasing awareness of health issues related to excessive humidity, technological advancements in dehumidifier design, and the growing demand for energy-efficient appliances. Additionally, the rise in disposable income and the expansion of the real estate sector contribute to the market's growth, as more homeowners seek to improve their living environments. The market is characterized by a diverse range of products, from basic models to advanced units with smart features, catering to a wide spectrum of consumers. As the demand for portable household dehumidifiers continues to rise, manufacturers are focusing on innovation and sustainability to meet consumer expectations and regulatory standards. This dynamic market is poised for significant growth, driven by the increasing need for effective humidity control solutions in homes worldwide.

Condensation or Mechanical Refrigeration Dehumidifier, Hygroscopic Dehumidifier, Other in the Global Portable Household Dehumidifier Market:

Condensation or Mechanical Refrigeration Dehumidifiers are among the most common types of dehumidifiers used in households. These devices operate by drawing in moist air and passing it over a refrigerated coil. As the air cools, moisture condenses into water droplets, which are then collected in a tank or drained away. This process effectively reduces humidity levels in the air, making it more comfortable and healthier to breathe. These dehumidifiers are particularly effective in warm, humid climates where moisture levels are high. They are available in various sizes and capacities, allowing consumers to choose a model that best suits their needs. Hygroscopic Dehumidifiers, on the other hand, use materials that naturally absorb moisture from the air. These materials, known as desiccants, can be silica gel, activated alumina, or other hygroscopic substances. Unlike mechanical dehumidifiers, hygroscopic dehumidifiers do not rely on refrigeration, making them quieter and more energy-efficient. They are ideal for use in cooler climates or in spaces where noise is a concern, such as bedrooms or offices. Hygroscopic dehumidifiers are also portable and easy to maintain, as they do not require a compressor or refrigerant. Other types of dehumidifiers in the market include thermoelectric and ionic membrane dehumidifiers. Thermoelectric dehumidifiers use the Peltier effect to create a temperature difference across a semiconductor, causing moisture to condense on a cold surface. These dehumidifiers are compact and silent, making them suitable for small spaces. Ionic membrane dehumidifiers, meanwhile, use ionic membranes to separate water vapor from the air. These advanced devices are still relatively new to the market but offer promising potential for energy-efficient dehumidification. Each type of dehumidifier has its own advantages and limitations, and the choice of which to use depends on factors such as climate, space, and personal preferences. As technology continues to evolve, the Global Portable Household Dehumidifier Market is likely to see further innovations and improvements in dehumidifier design and functionality.

Online Sales, Offline Sales in the Global Portable Household Dehumidifier Market:

The Global Portable Household Dehumidifier Market serves a wide range of consumers through both online and offline sales channels. Online sales have become increasingly popular due to the convenience and accessibility they offer. Consumers can browse a vast selection of dehumidifiers from the comfort of their homes, compare prices, read reviews, and make informed purchasing decisions. E-commerce platforms and online retailers often provide detailed product descriptions, specifications, and customer feedback, helping buyers choose the right dehumidifier for their needs. Additionally, online sales often come with competitive pricing, discounts, and promotions, making them an attractive option for budget-conscious consumers. The rise of digital marketing and social media has further boosted online sales, as manufacturers and retailers can reach a broader audience and engage with potential customers through targeted advertising and interactive content. On the other hand, offline sales remain a significant part of the market, particularly for consumers who prefer a hands-on shopping experience. Physical stores allow customers to see and test dehumidifiers in person, providing a tactile experience that online shopping cannot replicate. Sales representatives in stores can offer personalized advice and recommendations, helping customers find the best product for their specific needs. Offline sales channels include appliance stores, home improvement centers, and department stores, where consumers can explore a variety of brands and models. Some consumers also prefer offline shopping for the immediate availability of products, as they can purchase and take home a dehumidifier on the same day. Both online and offline sales channels play a crucial role in the distribution of portable household dehumidifiers, catering to different consumer preferences and shopping habits. As the market continues to grow, manufacturers and retailers are likely to adopt an omnichannel approach, integrating both online and offline strategies to enhance customer experience and drive sales.

Global Portable Household Dehumidifier Market Outlook:

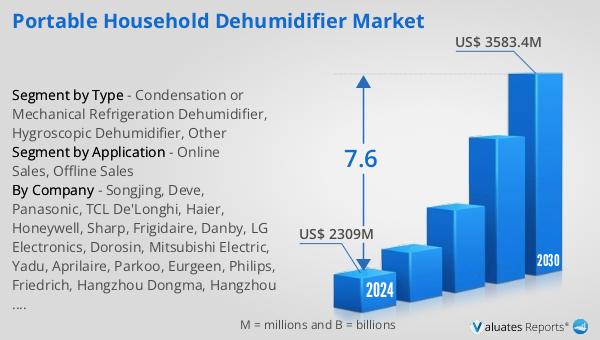

The outlook for the Global Portable Household Dehumidifier Market indicates a promising growth trajectory. The market is expected to expand from a valuation of approximately $2,309 million in 2024 to around $3,583.4 million by 2030. This growth is projected to occur at a Compound Annual Growth Rate (CAGR) of 7.6% over the forecast period. This upward trend reflects the increasing demand for effective humidity control solutions in residential settings. Several factors contribute to this growth, including rising awareness of the health benefits associated with maintaining optimal humidity levels, advancements in dehumidifier technology, and the growing emphasis on energy efficiency. As consumers become more conscious of indoor air quality and its impact on health, the demand for portable household dehumidifiers is likely to rise. Additionally, the expansion of the real estate sector and the increasing number of households worldwide further drive the market's growth. Manufacturers are focusing on innovation and sustainability to meet consumer expectations and regulatory standards, offering a diverse range of products with advanced features and improved energy efficiency. As a result, the Global Portable Household Dehumidifier Market is poised for significant growth, providing ample opportunities for industry players to capitalize on the increasing demand for humidity control solutions.

| Report Metric | Details |

| Report Name | Portable Household Dehumidifier Market |

| Accounted market size in 2024 | US$ 2309 million |

| Forecasted market size in 2030 | US$ 3583.4 million |

| CAGR | 7.6 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Songjing, Deve, Panasonic, TCL De'Longhi, Haier, Honeywell, Sharp, Frigidaire, Danby, LG Electronics, Dorosin, Mitsubishi Electric, Yadu, Aprilaire, Parkoo, Eurgeen, Philips, Friedrich, Hangzhou Dongma, Hangzhou Chuanjing Electrical Co., Ltd., Fudan Shenhua Purifying Technology Co.,Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |