What is Global Land-bottom Seismograph Market?

The Global Land-bottom Seismograph Market is a specialized segment within the broader field of geophysical instrumentation, focusing on devices that are deployed on the ocean floor to monitor seismic activity. These seismographs are crucial for understanding the dynamics of the Earth's crust beneath the ocean, which is essential for both scientific research and practical applications such as earthquake monitoring and tsunami warning systems. The market for these devices is driven by the increasing need for accurate and reliable data on seismic activities, especially in regions prone to earthquakes and other geological disturbances. Advances in technology have made these instruments more sophisticated, allowing for better data collection and analysis. The market is also influenced by the growing interest in offshore oil and gas exploration, as well as the need for better disaster preparedness and response strategies. As a result, the Global Land-bottom Seismograph Market is expected to see significant growth in the coming years, driven by both technological advancements and increasing demand from various sectors.

Broadband Seismograph, Short and Long Period Seismograph in the Global Land-bottom Seismograph Market:

Broadband seismographs, short-period seismographs, and long-period seismographs are integral components of the Global Land-bottom Seismograph Market, each serving distinct purposes based on their frequency range and application. Broadband seismographs are designed to record a wide range of frequencies, making them versatile tools for capturing both high-frequency and low-frequency seismic waves. This capability allows them to be used in a variety of settings, from monitoring local earthquakes to studying global seismic events. They are particularly valuable in research settings where comprehensive data collection is essential for understanding complex seismic phenomena. Short-period seismographs, on the other hand, are optimized for detecting high-frequency seismic waves, typically those generated by local or regional earthquakes. These instruments are crucial for early warning systems and rapid response efforts, as they can quickly detect and report seismic activity, allowing for timely alerts and potentially saving lives. Long-period seismographs focus on capturing low-frequency seismic waves, which are often associated with large-scale tectonic movements and deep Earth processes. These instruments are essential for studying the Earth's interior and understanding the dynamics of plate tectonics. In the context of the Global Land-bottom Seismograph Market, each type of seismograph plays a critical role in providing comprehensive seismic data, enabling researchers and decision-makers to better understand and respond to seismic events. The integration of these different types of seismographs into a cohesive monitoring network enhances the overall capability of the market to deliver accurate and timely seismic information. As technology continues to advance, the capabilities of these seismographs are expected to improve, further expanding their applications and effectiveness in various fields. The demand for these instruments is likely to grow as the need for precise and reliable seismic data becomes increasingly important in a world facing the challenges of natural disasters and the exploration of new energy resources.

Urban Early Warning, Geological Prospecting, Oil and Gas Collection, Transportation, Other in the Global Land-bottom Seismograph Market:

The Global Land-bottom Seismograph Market finds its applications in several critical areas, including urban early warning systems, geological prospecting, oil and gas collection, transportation, and other sectors. In urban early warning systems, land-bottom seismographs play a vital role in detecting seismic activity that could potentially impact densely populated areas. By providing real-time data on seismic events, these instruments enable authorities to issue timely warnings, allowing residents to take necessary precautions and reducing the risk of casualties and damage. In geological prospecting, seismographs are used to map the Earth's subsurface structures, providing valuable information for identifying mineral deposits and other geological features. This application is particularly important for the mining industry, where accurate data on the location and composition of mineral resources can significantly impact the success of exploration efforts. In the oil and gas sector, land-bottom seismographs are used to monitor seismic activity related to drilling and extraction processes. By providing detailed information on the Earth's subsurface, these instruments help companies optimize their operations, reduce risks, and improve safety. In transportation, seismographs are used to monitor the structural integrity of critical infrastructure, such as bridges and tunnels, by detecting vibrations and movements that could indicate potential issues. This application is essential for ensuring the safety and reliability of transportation networks, particularly in regions prone to seismic activity. Additionally, land-bottom seismographs are used in various other sectors, such as environmental monitoring and research, where they provide valuable data for understanding the Earth's dynamic processes and their impact on the environment. Overall, the Global Land-bottom Seismograph Market plays a crucial role in enhancing safety, efficiency, and understanding across a wide range of applications, making it an essential component of modern society's efforts to manage and mitigate the risks associated with seismic activity.

Global Land-bottom Seismograph Market Outlook:

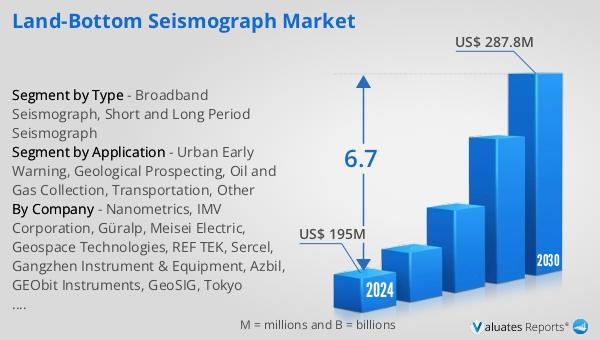

The outlook for the Global Land-bottom Seismograph Market indicates a promising trajectory, with expectations of growth from $195 million in 2024 to $287.8 million by 2030. This represents a compound annual growth rate (CAGR) of 6.7% over the forecast period. This growth is driven by several factors, including the increasing demand for accurate and reliable seismic data across various sectors. As the world becomes more aware of the risks associated with seismic activity, the need for advanced monitoring systems becomes more critical. The market is also benefiting from technological advancements that are enhancing the capabilities of seismographs, making them more effective and efficient in capturing seismic data. Additionally, the growing interest in offshore oil and gas exploration is contributing to the demand for land-bottom seismographs, as these instruments provide valuable data for optimizing exploration and extraction processes. The market's growth is further supported by the increasing focus on disaster preparedness and response strategies, which rely heavily on accurate and timely seismic information. As a result, the Global Land-bottom Seismograph Market is expected to continue its upward trajectory, driven by both technological advancements and increasing demand from various sectors. This growth presents significant opportunities for companies operating in this market, as they seek to develop and deliver innovative solutions that meet the evolving needs of their customers.

| Report Metric | Details |

| Report Name | Land-bottom Seismograph Market |

| Accounted market size in 2024 | US$ 195 in million |

| Forecasted market size in 2030 | US$ 287.8 million |

| CAGR | 6.7 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Nanometrics, IMV Corporation, Güralp, Meisei Electric, Geospace Technologies, REF TEK, Sercel, Gangzhen Instrument & Equipment, Azbil, GEObit Instruments, GeoSIG, Tokyo Sokushin, SmartSolo |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |