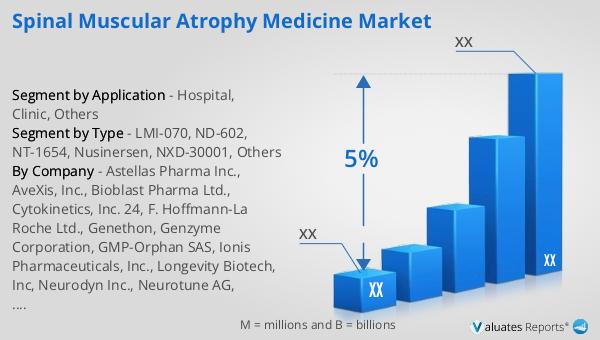

What is Global Spinal Muscular Atrophy Medicine Market?

The Global Spinal Muscular Atrophy (SMA) Medicine Market is a specialized segment within the broader pharmaceutical industry, focusing on treatments for Spinal Muscular Atrophy, a genetic disorder characterized by the loss of motor neurons and progressive muscle wasting. This market is driven by the increasing prevalence of SMA, advancements in genetic research, and the development of innovative therapies aimed at improving the quality of life for patients. The market encompasses a range of therapeutic options, including gene therapies, small molecule drugs, and biologics, each targeting different aspects of the disease's pathology. The demand for effective SMA treatments is further fueled by the growing awareness among healthcare professionals and patients, as well as supportive government initiatives and funding for rare diseases. As a result, the Global SMA Medicine Market is witnessing significant growth, with pharmaceutical companies investing heavily in research and development to bring new and improved therapies to market. This dynamic landscape is characterized by intense competition, with key players striving to gain a competitive edge through strategic collaborations, mergers, and acquisitions. Overall, the Global SMA Medicine Market represents a critical area of focus within the pharmaceutical industry, offering hope and improved outcomes for individuals affected by this debilitating condition.

LMI-070, ND-602, NT-1654, Nusinersen, NXD-30001, Others in the Global Spinal Muscular Atrophy Medicine Market:

LMI-070, ND-602, NT-1654, Nusinersen, NXD-30001, and other treatments are pivotal components of the Global Spinal Muscular Atrophy Medicine Market, each contributing uniquely to the management of SMA. LMI-070, also known as Branaplam, is an investigational small molecule drug that modulates the splicing of the SMN2 gene, thereby increasing the production of functional SMN protein, which is deficient in SMA patients. This approach aims to address the underlying genetic cause of the disease, offering a potential therapeutic benefit. ND-602 is another promising candidate, focusing on enhancing the stability and function of the SMN protein. By targeting the molecular mechanisms involved in SMA, ND-602 seeks to improve motor function and slow disease progression. NT-1654, on the other hand, is a biologic therapy designed to promote muscle growth and strength in SMA patients. It works by stimulating the production of muscle-specific proteins, thereby counteracting the muscle wasting characteristic of the disease. Nusinersen, marketed under the brand name Spinraza, is one of the most well-known treatments for SMA. It is an antisense oligonucleotide that modifies the splicing of the SMN2 gene, leading to increased production of the SMN protein. Administered via intrathecal injection, Nusinersen has demonstrated significant efficacy in improving motor function and survival in SMA patients, making it a cornerstone of SMA therapy. NXD-30001 is an emerging therapeutic option that targets the neuroprotective pathways involved in SMA. By enhancing neuronal survival and function, NXD-30001 aims to preserve motor neurons and improve patient outcomes. In addition to these specific treatments, the Global SMA Medicine Market includes a range of other therapies and supportive care options that address the diverse needs of SMA patients. These may include physical therapy, nutritional support, and respiratory care, all of which play a crucial role in managing the symptoms and complications associated with SMA. The development and availability of these treatments reflect the ongoing commitment of the pharmaceutical industry to advance SMA care and improve the lives of those affected by this challenging condition.

Hospital, Clinic, Others in the Global Spinal Muscular Atrophy Medicine Market:

The usage of Global Spinal Muscular Atrophy Medicine Market extends across various healthcare settings, including hospitals, clinics, and other specialized care facilities. In hospitals, SMA treatments are often administered as part of a comprehensive care plan that involves a multidisciplinary team of healthcare professionals. This team may include neurologists, geneticists, physical therapists, and respiratory therapists, all working together to provide holistic care for SMA patients. Hospitals serve as critical hubs for the administration of advanced therapies, such as gene therapies and intrathecal injections like Nusinersen, which require specialized equipment and expertise. In clinics, SMA treatments are typically provided in a more outpatient-focused setting, allowing for regular monitoring and follow-up care. Clinics play a vital role in the ongoing management of SMA, offering patients access to routine assessments, physical therapy, and supportive care services. These settings are often more accessible for patients and their families, providing a convenient option for receiving necessary treatments and interventions. Beyond hospitals and clinics, the Global SMA Medicine Market also encompasses other care environments, such as home healthcare services and specialized rehabilitation centers. Home healthcare services enable patients to receive certain treatments and therapies in the comfort of their own homes, reducing the need for frequent hospital visits and enhancing the overall quality of life. Specialized rehabilitation centers focus on providing intensive physical and occupational therapy to help SMA patients maintain and improve their motor function. These centers often collaborate with hospitals and clinics to ensure a seamless continuum of care for patients. Overall, the diverse usage of SMA treatments across these various settings highlights the importance of a coordinated and patient-centered approach to managing this complex condition. By leveraging the strengths of different healthcare environments, the Global SMA Medicine Market aims to deliver comprehensive and effective care for individuals living with SMA.

Global Spinal Muscular Atrophy Medicine Market Outlook:

The global pharmaceutical market was valued at approximately 1,475 billion USD in 2022, and it is projected to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth trajectory underscores the robust expansion and dynamic nature of the pharmaceutical industry, driven by factors such as increasing healthcare demands, technological advancements, and the continuous development of innovative therapies. In comparison, the chemical drug market, a significant subset of the broader pharmaceutical sector, has shown a steady increase from 1,005 billion USD in 2018 to an estimated 1,094 billion USD in 2022. This growth reflects the ongoing demand for chemical-based medications, which continue to play a crucial role in treating a wide range of medical conditions. The chemical drug market's expansion is supported by the development of new formulations, improved drug delivery systems, and the rising prevalence of chronic diseases that require long-term medication management. Together, these figures highlight the substantial economic impact and growth potential of the pharmaceutical and chemical drug markets, emphasizing their importance in addressing global healthcare needs and improving patient outcomes.

| Report Metric | Details |

| Report Name | Spinal Muscular Atrophy Medicine Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Astellas Pharma Inc., AveXis, Inc., Bioblast Pharma Ltd., Cytokinetics, Inc. 24, F. Hoffmann-La Roche Ltd., Genethon, Genzyme Corporation, GMP-Orphan SAS, Ionis Pharmaceuticals, Inc., Longevity Biotech, Inc, Neurodyn Inc., Neurotune AG, Novartis AG, Sarepta Therapeutics, Inc., Voyager Therapeutics, Inc., Vybion, Inc., WAVE Life Sciences Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |