What is Global Acrylonitrile Butadiene Styrene (ABS) Resin Market?

The Global Acrylonitrile Butadiene Styrene (ABS) Resin Market is a significant segment within the broader plastics industry, known for its versatile applications and robust demand across various sectors. ABS resin is a thermoplastic polymer that combines the strength and rigidity of acrylonitrile and styrene polymers with the toughness of polybutadiene rubber. This unique combination results in a material that is both strong and flexible, making it ideal for a wide range of applications. The global market for ABS resin is driven by its extensive use in industries such as automotive, electronics, and consumer goods, where its properties of impact resistance, toughness, and ease of processing are highly valued. Additionally, ABS resin is favored for its ability to be easily machined and its excellent surface quality, which allows for high-quality finishes in end products. As industries continue to innovate and demand materials that offer both performance and cost-effectiveness, the ABS resin market is expected to maintain its growth trajectory. The market's expansion is further supported by advancements in production technologies and the development of new applications that leverage the unique properties of ABS resin.

Emulsion Graft Copolymerization, Bulk Copolymerization, Others in the Global Acrylonitrile Butadiene Styrene (ABS) Resin Market:

Emulsion Graft Copolymerization, Bulk Copolymerization, and other methods are pivotal in the production of Acrylonitrile Butadiene Styrene (ABS) resin, each offering distinct advantages and characteristics that cater to different industrial needs. Emulsion Graft Copolymerization is a process where the polymerization of styrene and acrylonitrile occurs in the presence of polybutadiene latex. This method is renowned for producing ABS with excellent impact resistance and toughness, making it suitable for applications requiring durability. The emulsion process allows for precise control over the polymer structure, resulting in a consistent product with desirable mechanical properties. This method is particularly advantageous for producing ABS with a high gloss finish, which is often required in consumer electronics and automotive interiors. On the other hand, Bulk Copolymerization involves the polymerization of monomers in a bulk phase without the use of solvents or dispersing agents. This method is efficient and cost-effective, producing ABS with a high degree of purity and uniformity. Bulk copolymerization is favored for applications where clarity and color consistency are critical, such as in the production of transparent or colored ABS products. Additionally, this method allows for the incorporation of various additives to enhance specific properties of the ABS resin, such as UV resistance or flame retardancy. Other methods of ABS production include suspension polymerization and continuous mass polymerization, each offering unique benefits. Suspension polymerization, for instance, provides excellent control over particle size and distribution, which is crucial for applications requiring precise dimensional stability. Continuous mass polymerization, meanwhile, is ideal for large-scale production, offering high throughput and reduced production costs. These diverse production methods enable manufacturers to tailor ABS resin to meet specific application requirements, ensuring that the material remains a versatile and indispensable component in various industries. As the demand for high-performance materials continues to grow, the development and optimization of these polymerization techniques will play a crucial role in the evolution of the ABS resin market.

Automobiles Industry, Electronic Industry, Other industry in the Global Acrylonitrile Butadiene Styrene (ABS) Resin Market:

The usage of Global Acrylonitrile Butadiene Styrene (ABS) Resin Market spans several key industries, each leveraging the material's unique properties to enhance product performance and durability. In the automotive industry, ABS resin is extensively used for manufacturing various components such as dashboards, wheel covers, and interior trim parts. Its impact resistance and toughness make it ideal for applications that require durability and safety. Additionally, ABS's ability to be easily molded and colored allows for greater design flexibility, enabling manufacturers to create aesthetically pleasing and functional automotive parts. The lightweight nature of ABS also contributes to improved fuel efficiency, aligning with the industry's push towards more sustainable and energy-efficient vehicles. In the electronics industry, ABS resin is a preferred material for producing casings and housings for devices such as televisions, computers, and smartphones. Its excellent electrical insulation properties and resistance to heat make it suitable for protecting sensitive electronic components. Furthermore, ABS's ability to be easily machined and finished ensures that electronic products have a high-quality appearance, which is crucial in a competitive market where aesthetics play a significant role in consumer choice. Beyond automotive and electronics, ABS resin finds applications in other industries such as consumer goods, construction, and healthcare. In the consumer goods sector, ABS is used to manufacture products like toys, kitchen appliances, and luggage due to its durability and ease of processing. The construction industry utilizes ABS for piping and fittings, taking advantage of its strength and resistance to chemicals. In healthcare, ABS is employed in the production of medical devices and equipment, where its biocompatibility and sterilization capabilities are essential. The versatility of ABS resin, combined with its cost-effectiveness, ensures its continued relevance across these diverse industries, driving innovation and enhancing product quality.

Global Acrylonitrile Butadiene Styrene (ABS) Resin Market Outlook:

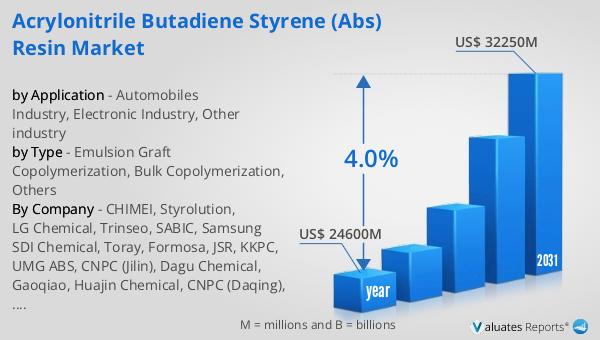

The global market for Acrylonitrile Butadiene Styrene (ABS) Resin was valued at $24.6 billion in 2024, with projections indicating a growth to approximately $32.25 billion by 2031. This anticipated growth reflects a compound annual growth rate (CAGR) of 4.0% over the forecast period. The steady increase in market size underscores the rising demand for ABS resin across various industries, driven by its unique properties and versatility. As industries continue to seek materials that offer a balance of performance, durability, and cost-effectiveness, ABS resin remains a preferred choice. The market's expansion is further supported by technological advancements in production processes and the development of new applications that capitalize on the material's strengths. This growth trajectory highlights the importance of ABS resin in meeting the evolving needs of industries such as automotive, electronics, and consumer goods. As the market continues to evolve, stakeholders are likely to focus on enhancing production efficiency and exploring sustainable practices to align with global environmental goals. The projected growth of the ABS resin market reflects its critical role in driving innovation and supporting the development of high-quality products across various sectors.

| Report Metric | Details |

| Report Name | Acrylonitrile Butadiene Styrene (ABS) Resin Market |

| Accounted market size in year | US$ 24600 million |

| Forecasted market size in 2031 | US$ 32250 million |

| CAGR | 4.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | CHIMEI, Styrolution, LG Chemical, Trinseo, SABIC, Samsung SDI Chemical, Toray, Formosa, JSR, KKPC, UMG ABS, CNPC (Jilin), Dagu Chemical, Gaoqiao, Huajin Chemical, CNPC (Daqing), Lejin Chemical, CNPC (Lanzhou) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |