What is Global Medical Surgical Headlight Market?

The Global Medical Surgical Headlight Market is a specialized segment within the broader medical equipment industry, focusing on the production and distribution of headlights used in surgical settings. These headlights are essential tools for surgeons, providing focused and adjustable illumination during procedures, which is crucial for precision and safety. The market encompasses a variety of headlight types, including corded and cordless models, each offering distinct advantages depending on the surgical environment and specific needs of the medical professionals. The demand for medical surgical headlights is driven by the increasing number of surgical procedures worldwide, advancements in medical technology, and the growing emphasis on improving surgical outcomes. Additionally, the market is influenced by factors such as the rising prevalence of chronic diseases, an aging population, and the expansion of healthcare infrastructure in emerging economies. As healthcare providers seek to enhance operational efficiency and patient care, the adoption of advanced surgical headlights is expected to rise, further propelling market growth. The market is characterized by intense competition among key players, who are continually innovating to offer products with improved functionality, ergonomics, and energy efficiency.

Corded, Cordless in the Global Medical Surgical Headlight Market:

In the Global Medical Surgical Headlight Market, corded and cordless headlights represent two primary categories, each with unique features and benefits. Corded surgical headlights are traditionally favored in settings where consistent power supply is crucial. These headlights are connected to a power source via a cord, ensuring uninterrupted illumination during lengthy surgical procedures. The reliability of corded headlights makes them a preferred choice in high-stakes environments where any interruption in light could compromise the outcome of a surgery. They are often equipped with high-intensity bulbs and advanced optics to provide bright, focused light, which is essential for intricate surgical tasks. However, the presence of a cord can sometimes limit mobility and flexibility for the surgeon, potentially leading to inconvenience or entanglement during complex procedures. On the other hand, cordless surgical headlights offer enhanced mobility and ease of use, as they are powered by rechargeable batteries. This feature allows surgeons to move freely without being tethered to a power source, which can be particularly advantageous in dynamic surgical environments or when performing procedures that require frequent repositioning. Cordless headlights are designed to be lightweight and ergonomically balanced, reducing strain on the surgeon's head and neck during prolonged use. Advances in battery technology have significantly improved the performance of cordless headlights, with many models now offering extended battery life and quick recharge capabilities. Despite these advantages, cordless headlights may require careful management of battery life to avoid power depletion during critical moments. The choice between corded and cordless headlights often depends on the specific needs of the surgical team, the nature of the procedures being performed, and the infrastructure of the healthcare facility. Both types of headlights are integral to modern surgical practice, and ongoing innovations continue to enhance their functionality, efficiency, and user experience.

Surgical, Dental, Others in the Global Medical Surgical Headlight Market:

The usage of medical surgical headlights spans various areas, including surgical, dental, and other medical fields, each benefiting from the precise illumination these devices provide. In surgical settings, headlights are indispensable tools that enhance visibility and accuracy during operations. Surgeons rely on these devices to illuminate the surgical site, allowing them to perform intricate procedures with greater precision and confidence. The focused light helps in identifying anatomical structures, minimizing the risk of errors, and improving overall surgical outcomes. In dental practices, surgical headlights are equally valuable, providing dentists with the necessary illumination to conduct detailed examinations and procedures. The ability to direct light precisely onto the area of interest is crucial for tasks such as cavity preparation, root canal treatment, and cosmetic dentistry. Dental professionals benefit from the ergonomic design of these headlights, which reduces fatigue and enhances comfort during long procedures. Beyond surgical and dental applications, medical surgical headlights find use in various other medical fields, including veterinary medicine, emergency care, and outpatient procedures. In veterinary settings, these headlights assist veterinarians in performing surgeries and examinations on animals, where clear visibility is essential for accurate diagnosis and treatment. In emergency care, portable and cordless headlights are particularly useful, providing medical personnel with the flexibility to deliver care in diverse and often challenging environments. The versatility and adaptability of medical surgical headlights make them valuable assets across a wide range of medical disciplines, contributing to improved patient care and outcomes.

Global Medical Surgical Headlight Market Outlook:

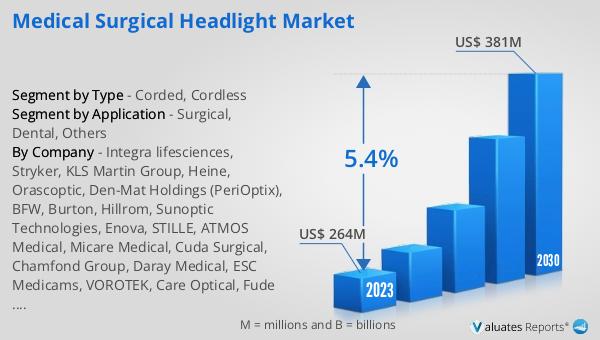

The global market for medical surgical headlights was valued at $264 million in 2024 and is anticipated to grow to a revised size of $381 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.4% over the forecast period. This growth is driven by the increasing demand for advanced surgical equipment and the continuous innovation by leading manufacturers. The top five manufacturers in this market, namely Integra Lifesciences, Stryker, KLS Martin, Heine, and Orascoptic, collectively hold over 45% of the market share, with Integra Lifesciences leading the pack with a market share exceeding 15%. In terms of product type, cordless surgical headlights dominate the market, accounting for more than 50% of the market share. This preference for cordless models is attributed to their enhanced mobility and convenience, which are highly valued in modern surgical environments. In the application segment, surgical procedures represent the largest share, with over 60% of the market, underscoring the critical role of surgical headlights in ensuring precision and safety during operations. The market's growth trajectory is supported by the ongoing advancements in medical technology and the increasing focus on improving surgical outcomes worldwide.

| Report Metric | Details |

| Report Name | Medical Surgical Headlight Market |

| Accounted market size in year | US$ 264 million |

| Forecasted market size in 2031 | US$ 381 million |

| CAGR | 5.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Integra lifesciences, Stryker, KLS Martin Group, Heine, Orascoptic, Den-Mat Holdings (PeriOptix), BFW, Burton, Hillrom, Sunoptic Technologies, Enova, STILLE, ATMOS Medical, Micare Medical, Cuda Surgical, Chamfond Group, Daray Medical, ESC Medicams, VOROTEK, Care Optical, Fude Medical Optoelectronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |