What is Global Chinese Baijiu Bottle Caps Market?

The Global Chinese Baijiu Bottle Caps Market refers to the industry focused on producing and supplying bottle caps specifically designed for Baijiu, a traditional Chinese spirit. Baijiu is a highly popular alcoholic beverage in China, and its packaging plays a crucial role in maintaining its quality and appeal. The market for Baijiu bottle caps is driven by the demand for secure, tamper-proof, and aesthetically pleasing closures that preserve the spirit's flavor and aroma. These caps are manufactured using various materials, including aluminum and plastic, to cater to different consumer preferences and packaging requirements. The market is characterized by a mix of large-scale manufacturers and smaller enterprises, each contributing to the diverse range of products available. As Baijiu continues to gain popularity both domestically and internationally, the demand for high-quality bottle caps is expected to grow, making this market an essential component of the broader Baijiu industry. The market's growth is also influenced by innovations in packaging technology and design, which aim to enhance the consumer experience and ensure product integrity. Overall, the Global Chinese Baijiu Bottle Caps Market is a dynamic and evolving sector that plays a vital role in the packaging and distribution of Baijiu.

Aluminum Bottle Caps, Plastic Bottle Caps, Other in the Global Chinese Baijiu Bottle Caps Market:

Aluminum bottle caps are a significant segment within the Global Chinese Baijiu Bottle Caps Market, known for their durability, lightweight nature, and excellent sealing properties. These caps are favored for their ability to provide a secure closure that prevents leakage and contamination, ensuring the Baijiu remains fresh and flavorful. Aluminum caps are also valued for their recyclability, aligning with growing environmental concerns and sustainability efforts. The manufacturing process of aluminum caps involves precision engineering to create a perfect fit for Baijiu bottles, often incorporating tamper-evident features to enhance security. On the other hand, plastic bottle caps offer a cost-effective alternative, providing flexibility in design and color options. Plastic caps are lightweight and can be molded into various shapes, allowing for creative branding opportunities. They are also resistant to corrosion, making them suitable for long-term storage. However, the environmental impact of plastic caps is a concern, prompting manufacturers to explore biodegradable and eco-friendly materials. In addition to aluminum and plastic, the market also includes other types of bottle caps, such as those made from composite materials or featuring innovative designs like flip-tops or screw caps. These alternatives cater to niche markets or specific consumer preferences, offering unique functionalities or aesthetic appeal. The choice of bottle cap material and design is influenced by factors such as cost, brand image, and consumer convenience, with manufacturers continually innovating to meet evolving market demands. Overall, the diversity in bottle cap options reflects the dynamic nature of the Global Chinese Baijiu Bottle Caps Market, where functionality, sustainability, and consumer appeal are key considerations.

Large Enterprise, SMEs in the Global Chinese Baijiu Bottle Caps Market:

The usage of Global Chinese Baijiu Bottle Caps Market varies significantly between large enterprises and small to medium-sized enterprises (SMEs). Large enterprises, often involved in mass production and distribution of Baijiu, prioritize efficiency and consistency in their packaging solutions. For these companies, aluminum bottle caps are a popular choice due to their robustness and ability to maintain product integrity during transportation and storage. Large enterprises benefit from economies of scale, allowing them to invest in high-quality, tamper-evident caps that enhance brand reputation and consumer trust. These companies may also explore custom designs and branding on their bottle caps to differentiate their products in a competitive market. In contrast, SMEs may have different priorities when selecting bottle caps for their Baijiu products. Cost-effectiveness is often a primary consideration, leading many SMEs to opt for plastic bottle caps, which offer affordability and versatility. SMEs may also focus on niche markets or artisanal Baijiu, where unique or innovative cap designs can add value and appeal to consumers. The flexibility of plastic caps allows SMEs to experiment with different colors and shapes, aligning with their brand identity and target audience. Additionally, SMEs may prioritize sustainability, seeking eco-friendly cap options to appeal to environmentally conscious consumers. The choice of bottle caps for SMEs is often influenced by their production scale, budget constraints, and marketing strategies. Overall, the Global Chinese Baijiu Bottle Caps Market serves a diverse range of businesses, each with unique needs and preferences, highlighting the importance of adaptability and innovation in this sector.

Global Chinese Baijiu Bottle Caps Market Outlook:

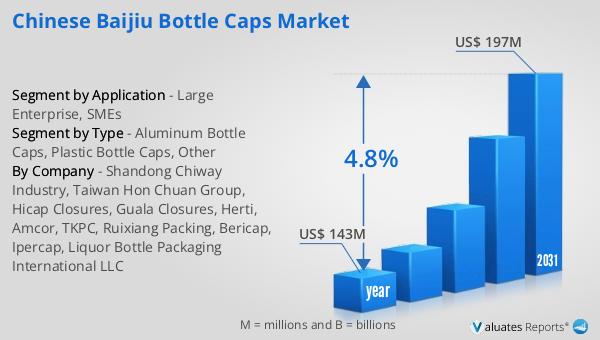

The global market for Chinese Baijiu Bottle Caps was valued at $143 million in 2024 and is anticipated to grow to a revised size of $197 million by 2031, with a compound annual growth rate (CAGR) of 4.8% during the forecast period. The market is dominated by five major manufacturers: Shandong Chiway Industry, Taiwan Hon Chuan Group, Hicap Closures, Guala Closures, and Herti, which collectively hold over 65% of the market share. Shandong Chiway Industry stands out as the largest manufacturer, commanding more than 40% of the market share. China leads the world in the production of Chinese Baijiu bottle caps, contributing to over 95% of the global market share. Among the different types of bottle caps, aluminum caps hold a significant portion, with a market share exceeding 60%. This dominance is attributed to their superior sealing capabilities and recyclability, which align with both consumer preferences and environmental considerations. The market's growth is driven by the increasing demand for Baijiu, both domestically and internationally, as well as advancements in packaging technology that enhance product appeal and security. As the market continues to evolve, manufacturers are likely to focus on innovation and sustainability to meet the changing needs of consumers and maintain their competitive edge.

| Report Metric | Details |

| Report Name | Chinese Baijiu Bottle Caps Market |

| Accounted market size in year | US$ 143 million |

| Forecasted market size in 2031 | US$ 197 million |

| CAGR | 4.8% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Shandong Chiway Industry, Taiwan Hon Chuan Group, Hicap Closures, Guala Closures, Herti, Amcor, TKPC, Ruixiang Packing, Bericap, Ipercap, Liquor Bottle Packaging International LLC |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |