What is Global Sports Nutritional Supplements Market?

The Global Sports Nutritional Supplements Market is a rapidly expanding sector that caters to athletes, fitness enthusiasts, and individuals seeking to enhance their physical performance and overall health. These supplements are designed to provide essential nutrients that support muscle growth, improve endurance, and aid in recovery after intense physical activities. The market encompasses a wide range of products, including protein powders, amino acids, vitamins, minerals, and other performance-enhancing supplements. With the increasing awareness of health and fitness, there is a growing demand for these products across the globe. The market is driven by factors such as the rising number of health clubs and fitness centers, the growing trend of personalized nutrition, and the increasing participation in sports and fitness activities. Additionally, advancements in product formulations and the introduction of innovative supplements are further propelling the market's growth. As consumers become more health-conscious, the demand for sports nutritional supplements is expected to continue its upward trajectory, making it a lucrative market for manufacturers and retailers alike.

Creatine, Protein, Citrulline, L-carnitine, Branched Chain Amino Acids (BCAAs), Arginine, L-Glutamine, Beta-alanine, Others in the Global Sports Nutritional Supplements Market:

Creatine is one of the most popular supplements in the Global Sports Nutritional Supplements Market, known for its ability to enhance strength and muscle mass. It works by increasing the availability of ATP, the energy currency of cells, which helps improve performance during high-intensity workouts. Protein supplements, particularly whey and casein, are essential for muscle repair and growth. They provide the necessary amino acids that the body cannot produce on its own, making them a staple for athletes and bodybuilders. Citrulline is another supplement that aids in increasing blood flow to muscles, thereby enhancing endurance and reducing fatigue. L-carnitine is known for its role in fat metabolism, helping to convert fat into energy, which can be beneficial for weight management and endurance sports. Branched Chain Amino Acids (BCAAs), including leucine, isoleucine, and valine, are crucial for muscle protein synthesis and reducing muscle breakdown during exercise. Arginine is a precursor to nitric oxide, which helps in vasodilation and improving blood flow, thus enhancing performance and recovery. L-Glutamine is an amino acid that supports immune function and gut health, which can be compromised during intense training. Beta-alanine is known for its ability to buffer acid in muscles, reducing fatigue and improving performance in high-intensity exercises. Other supplements in the market include vitamins, minerals, and herbal extracts that support overall health and wellness. These supplements are available in various forms, such as powders, capsules, and bars, catering to the diverse preferences of consumers. The market is characterized by continuous innovation, with manufacturers focusing on developing products that are not only effective but also safe and compliant with regulatory standards. As the demand for sports nutritional supplements continues to grow, the market is witnessing increased competition, with new entrants and established players vying for market share. This has led to a focus on product differentiation, branding, and marketing strategies to capture the attention of consumers. Overall, the Global Sports Nutritional Supplements Market is a dynamic and evolving industry, driven by the increasing emphasis on health, fitness, and performance optimization.

Online Sales, Offline Sales in the Global Sports Nutritional Supplements Market:

The usage of Global Sports Nutritional Supplements Market is prominently divided into online and offline sales channels, each with its unique advantages and challenges. Online sales have gained significant traction in recent years, driven by the convenience and accessibility they offer to consumers. With the rise of e-commerce platforms and digital marketing, consumers can easily browse, compare, and purchase supplements from the comfort of their homes. Online sales channels provide a vast array of products, detailed information, and customer reviews, enabling consumers to make informed decisions. Additionally, online platforms often offer competitive pricing, discounts, and subscription models, making it an attractive option for regular users of sports nutritional supplements. The global reach of online sales also allows manufacturers to tap into international markets, expanding their customer base and increasing brand visibility. On the other hand, offline sales channels, such as health stores, pharmacies, and gyms, continue to play a crucial role in the distribution of sports nutritional supplements. These physical outlets provide consumers with the opportunity to physically examine products, seek personalized advice from knowledgeable staff, and enjoy immediate purchase gratification. Offline sales channels also foster brand loyalty and trust, as consumers can interact directly with products and receive expert guidance. Moreover, offline channels often host events, workshops, and promotions, creating a community-driven shopping experience that resonates with fitness enthusiasts. Despite the growing popularity of online sales, offline channels remain relevant, particularly for consumers who prefer a tactile shopping experience or require immediate product availability. The integration of online and offline sales strategies, known as omnichannel retailing, is becoming increasingly important for manufacturers and retailers in the Global Sports Nutritional Supplements Market. By leveraging both channels, companies can provide a seamless shopping experience, catering to the diverse preferences and needs of consumers. As the market continues to evolve, the balance between online and offline sales will be crucial in determining the success of brands in the competitive landscape of sports nutritional supplements.

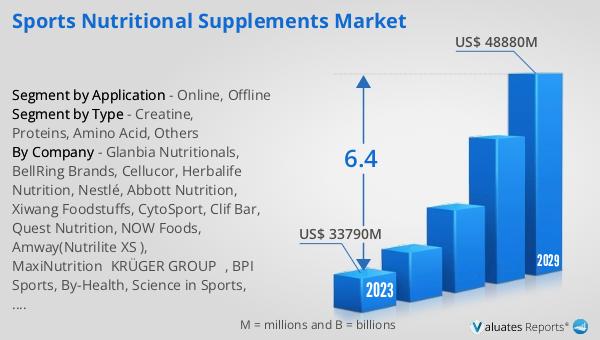

Global Sports Nutritional Supplements Market Outlook:

The global market for Sports Nutritional Supplements was valued at approximately $26,140 million in 2024 and is anticipated to grow to a revised size of around $44,920 million by 2031, reflecting a compound annual growth rate (CAGR) of 8.2% over the forecast period. Among the leading manufacturers in this market are Glanbia Nutritionals, BellRing Brands, Cellucor, Herbalife Nutrition, and Nestlé, collectively holding a market share exceeding 10%. Glanbia Nutritionals stands out as the largest manufacturer, commanding about 4% of the market share. North America emerges as the largest consumer market for sports nutritional supplements, accounting for over 45% of the global consumption. In terms of sales channels, online sales dominate, representing more than 65% of the market. This significant online presence underscores the shift in consumer purchasing behavior towards digital platforms, driven by the convenience and accessibility they offer. The robust growth of the sports nutritional supplements market is fueled by increasing health consciousness, the rising popularity of fitness activities, and the continuous innovation in product offerings. As the market expands, manufacturers are focusing on enhancing their product portfolios and strengthening their distribution networks to capture a larger share of this lucrative market.

| Report Metric | Details |

| Report Name | Sports Nutritional Supplements Market |

| Accounted market size in year | US$ 26140 million |

| Forecasted market size in 2031 | US$ 44920 million |

| CAGR | 8.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Glanbia Nutritionals, BellRing Brands, Cellucor, Herbalife, Nestlé, Abbott Nutrition, Xiwang Foodstuffs, CytoSport, Clif Bar, Quest Nutrition, NOW Foods, Amway(Nutrilite XS ), MaxiNutrition(KRÜGER GROUP), BPI Sports, By-Health, Science in Sports, Competitor Sports |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |