What is Global Steam Meters Market?

The Global Steam Meters Market is a specialized segment within the broader field of flow measurement technology. Steam meters are essential devices used to measure the flow rate of steam in various industrial processes. These meters are crucial for industries that rely on steam for heating, power generation, and other applications, as they help in monitoring and optimizing steam usage, thereby improving efficiency and reducing costs. The market for steam meters is driven by the increasing demand for energy efficiency and the need to reduce carbon emissions across industries. As industries strive to meet regulatory requirements and sustainability goals, the adoption of steam meters is expected to rise. The market encompasses a range of technologies, including orifice plate flow meters, ultrasonic flow meters, and others, each offering unique advantages depending on the specific application. The global steam meters market is characterized by technological advancements, with manufacturers focusing on developing more accurate and reliable meters to meet the evolving needs of industries. As a result, the market is poised for steady growth, driven by the ongoing industrialization and the increasing emphasis on energy management and conservation.

Orifice Plate Flow Meters, Ultrasonic Flow Meters, Other in the Global Steam Meters Market:

Orifice plate flow meters, ultrasonic flow meters, and other types of steam meters each play a significant role in the Global Steam Meters Market, catering to diverse industrial needs. Orifice plate flow meters are among the most traditional and widely used types of steam meters. They operate on the principle of differential pressure, where a plate with a specific orifice is placed in the flow path, causing a drop in pressure that is proportional to the flow rate. These meters are valued for their simplicity, durability, and cost-effectiveness, making them suitable for a wide range of applications. However, they may not be as accurate as some modern alternatives and can suffer from pressure loss, which is a consideration for industries focused on energy efficiency. Ultrasonic flow meters, on the other hand, represent a more advanced technology. They use sound waves to measure the velocity of steam as it passes through a pipe. By calculating the time it takes for the sound waves to travel upstream and downstream, the flow rate can be determined. Ultrasonic meters are known for their high accuracy, low maintenance requirements, and ability to handle a wide range of flow conditions. They are particularly useful in applications where precision is critical, such as in the pharmaceutical or chemical industries. Additionally, ultrasonic meters do not cause pressure loss, making them an energy-efficient choice. Other types of steam meters include vortex flow meters, Coriolis flow meters, and thermal mass flow meters. Vortex flow meters work by detecting the vortices shed by a bluff body placed in the flow path. They are robust and can handle high temperatures and pressures, making them suitable for harsh industrial environments. Coriolis flow meters measure the mass flow rate of steam by detecting the force exerted by the flow on a vibrating tube. They offer high accuracy and are ideal for applications requiring precise mass flow measurements. Thermal mass flow meters measure the flow rate based on the heat transfer from a heated element to the steam. They are effective for low flow rates and are often used in applications where other types of meters may not perform well. Each type of steam meter has its own set of advantages and limitations, and the choice of meter depends on factors such as the specific application, required accuracy, installation conditions, and budget. As industries continue to evolve and demand more efficient and accurate flow measurement solutions, the Global Steam Meters Market is expected to see continued innovation and growth.

Chemical, Oil & Gas, Pharmaceutical, Other in the Global Steam Meters Market:

The Global Steam Meters Market finds extensive usage across various industries, including chemical, oil & gas, pharmaceutical, and others, each with unique requirements and challenges. In the chemical industry, steam meters are crucial for monitoring and controlling steam flow in processes such as distillation, evaporation, and heating. Accurate steam measurement is essential to ensure product quality, optimize energy usage, and maintain safety standards. The ability to precisely measure steam flow helps chemical manufacturers reduce waste, lower operational costs, and comply with environmental regulations. In the oil & gas industry, steam meters are used in processes such as enhanced oil recovery, refining, and petrochemical production. Steam is often used to heat crude oil, improve its flow properties, and facilitate extraction. Accurate steam measurement is vital to optimize these processes, improve efficiency, and reduce emissions. The harsh operating conditions in the oil & gas sector require steam meters that are robust, reliable, and capable of handling high temperatures and pressures. In the pharmaceutical industry, steam is used for sterilization, heating, and other critical processes. The precise measurement of steam flow is essential to ensure the efficacy and safety of pharmaceutical products. Steam meters help pharmaceutical manufacturers maintain strict quality control, optimize energy usage, and comply with stringent regulatory requirements. The need for high accuracy and reliability in steam measurement makes ultrasonic and Coriolis flow meters popular choices in this industry. Other industries that utilize steam meters include food and beverage, pulp and paper, and power generation. In the food and beverage industry, steam is used for cooking, sterilization, and cleaning processes. Accurate steam measurement helps ensure product quality, improve energy efficiency, and reduce costs. In the pulp and paper industry, steam is used for drying and heating processes, and precise steam measurement is essential to optimize production and reduce energy consumption. In power generation, steam meters are used to monitor and control steam flow in boilers and turbines, helping to improve efficiency and reduce emissions. Overall, the Global Steam Meters Market plays a critical role in helping industries optimize their steam usage, improve efficiency, and meet regulatory requirements. As industries continue to focus on sustainability and energy management, the demand for accurate and reliable steam meters is expected to grow.

Global Steam Meters Market Outlook:

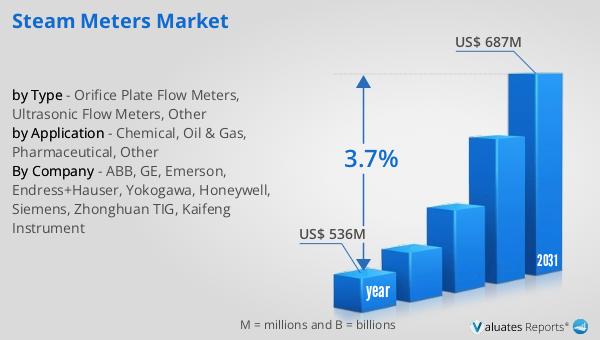

The outlook for the Global Steam Meters Market indicates a promising future, with significant growth anticipated over the coming years. In 2024, the market was valued at approximately US$ 536 million, and it is projected to expand to a revised size of US$ 687 million by 2031. This growth represents a compound annual growth rate (CAGR) of 3.7% during the forecast period. China emerges as the largest market for steam meters, capturing around 21% of the global market share. This is followed closely by North America, which accounts for approximately 20% of the market share. The dominance of these regions can be attributed to their robust industrial sectors and the increasing emphasis on energy efficiency and sustainability. Furthermore, the market is characterized by a high level of competition, with the top three companies holding about 30% of the market share. This competitive landscape drives innovation and the development of advanced steam metering technologies to meet the evolving needs of industries. As industries across the globe continue to prioritize energy management and regulatory compliance, the demand for steam meters is expected to rise, contributing to the market's steady growth. The Global Steam Meters Market is poised to play a crucial role in helping industries optimize their steam usage, reduce costs, and achieve their sustainability goals.

| Report Metric | Details |

| Report Name | Steam Meters Market |

| Accounted market size in year | US$ 536 million |

| Forecasted market size in 2031 | US$ 687 million |

| CAGR | 3.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | ABB, GE, Emerson, Endress+Hauser, Yokogawa, Honeywell, Siemens, Zhonghuan TIG, Kaifeng Instrument |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |