What is Global Alkyl Benzo Sulfonate Market?

The Global Alkyl Benzo Sulfonate Market refers to the worldwide industry focused on the production, distribution, and application of alkyl benzo sulfonates, which are a type of anionic surfactant. These compounds are primarily used in the formulation of detergents and cleaning products due to their excellent ability to lower the surface tension of water, thereby enhancing the cleaning efficiency. The market encompasses a wide range of industries, including household cleaning, industrial cleaning, and personal care products, where these surfactants play a crucial role. The demand for alkyl benzo sulfonates is driven by their effectiveness in removing dirt and grease, their biodegradability, and their relatively low cost compared to other surfactants. As environmental concerns and regulations become more stringent, the market is also seeing a shift towards more sustainable and eco-friendly formulations. This has led to increased research and development efforts to improve the environmental profile of these compounds while maintaining their performance. The market is characterized by a mix of established players and new entrants, with competition based on product performance, price, and environmental impact. Overall, the Global Alkyl Benzo Sulfonate Market is a dynamic and evolving sector that plays a vital role in the global cleaning and personal care industries.

Linear Alkylbenzene Sulfonate, Branched Alkylbenzene Sulfonate in the Global Alkyl Benzo Sulfonate Market:

Linear Alkylbenzene Sulfonate (LAS) and Branched Alkylbenzene Sulfonate (BAS) are two primary types of alkyl benzo sulfonates that dominate the Global Alkyl Benzo Sulfonate Market. LAS is the most widely used due to its superior biodegradability and cost-effectiveness. It is derived from linear alkylbenzene (LAB), which is produced through the alkylation of benzene with linear paraffins. The linear structure of LAS allows it to break down more easily in the environment, making it a preferred choice for manufacturers aiming to meet environmental regulations. LAS is commonly used in household detergents, industrial cleaners, and personal care products. Its ability to produce a rich lather and effectively remove dirt and grease makes it a staple in the cleaning industry. On the other hand, BAS, which is derived from branched alkylbenzene, was once popular due to its excellent cleaning properties and ability to produce a stable foam. However, its branched structure makes it less biodegradable, leading to environmental concerns and a decline in its usage. Despite this, BAS is still used in some industrial applications where its specific properties are required. The market for BAS is more niche compared to LAS, with demand driven by specific industrial needs rather than mass-market consumer products. The shift towards more environmentally friendly products has led to increased research into alternative surfactants that can match the performance of BAS without the environmental drawbacks. Both LAS and BAS are integral to the Global Alkyl Benzo Sulfonate Market, with their usage determined by a balance of performance, cost, and environmental impact. As the market continues to evolve, the focus is on developing new formulations that offer the cleaning power of traditional surfactants while minimizing their ecological footprint. This has led to innovations in production processes and the exploration of renewable raw materials to produce more sustainable surfactants. The competition between LAS and BAS highlights the broader trends in the market, where environmental considerations are increasingly influencing product development and consumer preferences. As regulations become stricter and consumer awareness grows, the market is likely to see a continued shift towards more sustainable and biodegradable products. This presents both challenges and opportunities for manufacturers, who must balance the need for effective cleaning solutions with the demand for environmentally responsible products. Overall, the Global Alkyl Benzo Sulfonate Market is a complex and dynamic industry, with LAS and BAS playing key roles in its development and evolution.

Detergent, Emulsifier, Coupling Agent, Others in the Global Alkyl Benzo Sulfonate Market:

The Global Alkyl Benzo Sulfonate Market finds its applications in various areas, including detergents, emulsifiers, coupling agents, and other specialized uses. In the detergent industry, alkyl benzo sulfonates are prized for their ability to effectively remove dirt, grease, and stains from fabrics and surfaces. They are a key ingredient in both household and industrial cleaning products, where their surfactant properties help to break down and disperse oils and fats. The ability of these compounds to produce a rich lather and enhance the cleaning power of detergents makes them indispensable in the formulation of laundry detergents, dishwashing liquids, and all-purpose cleaners. In addition to their cleaning capabilities, alkyl benzo sulfonates also act as emulsifiers, helping to stabilize mixtures of oil and water. This property is particularly valuable in the formulation of personal care products, such as shampoos, conditioners, and lotions, where they help to create a smooth and consistent texture. As emulsifiers, they enable the blending of ingredients that would otherwise separate, ensuring that products maintain their desired consistency and performance. Alkyl benzo sulfonates also serve as coupling agents, which are used to enhance the compatibility of different ingredients in a formulation. This is especially important in complex formulations where multiple active ingredients need to work together effectively. By improving the solubility and dispersion of these ingredients, coupling agents help to optimize the performance of the final product. Beyond these primary applications, alkyl benzo sulfonates are also used in a variety of other industries, including agriculture, textiles, and construction. In agriculture, they are used as wetting agents to improve the distribution and absorption of pesticides and fertilizers. In the textile industry, they aid in the dyeing and finishing processes by enhancing the penetration of dyes and finishes into fabrics. In construction, they are used as additives in concrete and mortar to improve workability and reduce water content. The versatility of alkyl benzo sulfonates makes them a valuable component in a wide range of products and industries. As the market continues to evolve, there is a growing emphasis on developing more sustainable and environmentally friendly formulations. This has led to increased research into alternative raw materials and production processes that can reduce the environmental impact of these compounds while maintaining their performance. Overall, the Global Alkyl Benzo Sulfonate Market plays a crucial role in the development of effective and sustainable solutions across a diverse range of applications.

Global Alkyl Benzo Sulfonate Market Outlook:

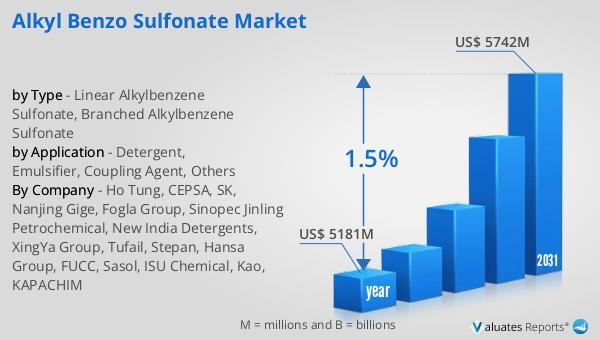

In 2024, the global market for Alkyl Benzo Sulfonate was valued at approximately $5,181 million. Looking ahead, this market is expected to grow, reaching an estimated size of $5,742 million by 2031. This growth represents a compound annual growth rate (CAGR) of 1.5% over the forecast period. This steady growth can be attributed to several factors, including the increasing demand for effective cleaning products and the ongoing shift towards more sustainable and environmentally friendly formulations. As consumers become more aware of the environmental impact of cleaning products, there is a growing preference for products that offer both performance and sustainability. This has led to increased research and development efforts to improve the environmental profile of alkyl benzo sulfonates while maintaining their effectiveness. The market is also influenced by regulatory changes, with stricter environmental regulations driving the demand for biodegradable and eco-friendly surfactants. As a result, manufacturers are focusing on developing new formulations that meet these requirements while offering the cleaning power that consumers expect. The competition in the market is intense, with established players and new entrants vying for market share based on product performance, price, and environmental impact. Overall, the Global Alkyl Benzo Sulfonate Market is poised for steady growth, driven by the demand for effective and sustainable cleaning solutions.

| Report Metric | Details |

| Report Name | Alkyl Benzo Sulfonate Market |

| Accounted market size in year | US$ 5181 million |

| Forecasted market size in 2031 | US$ 5742 million |

| CAGR | 1.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Ho Tung, CEPSA, SK, Nanjing Gige, Fogla Group, Sinopec Jinling Petrochemical, New India Detergents, XingYa Group, Tufail, Stepan, Hansa Group, FUCC, Sasol, ISU Chemical, Kao, KAPACHIM |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |