What is Global Interactive Voice Response Systems Market?

The Global Interactive Voice Response (IVR) Systems Market refers to the industry focused on the development, deployment, and utilization of IVR technology worldwide. IVR systems are automated telephony systems that interact with callers, gather information, and route calls to the appropriate recipient. These systems use pre-recorded or dynamically generated audio to guide users through a menu of options, allowing them to input responses via voice or keypad. The market for IVR systems is driven by the need for businesses and organizations to enhance customer service, reduce operational costs, and improve efficiency. IVR systems are widely used across various sectors, including banking, healthcare, telecommunications, and retail, to handle high volumes of calls, provide 24/7 customer support, and streamline processes. As technology advances, IVR systems are becoming more sophisticated, incorporating features like natural language processing and integration with other digital platforms. This evolution is expanding the capabilities and applications of IVR systems, making them an essential tool for modern businesses seeking to optimize their customer interaction strategies. The global market for IVR systems is expected to continue growing as more organizations recognize the benefits of automating customer interactions and enhancing user experiences.

On-premises, Cloud-based in the Global Interactive Voice Response Systems Market:

In the realm of Global Interactive Voice Response Systems, two primary deployment models are prevalent: On-premises and Cloud-based solutions. On-premises IVR systems are installed and operated from within an organization's own infrastructure. This model offers businesses complete control over their IVR systems, allowing for extensive customization and integration with existing systems. Organizations that prioritize data security and have the necessary IT resources often prefer on-premises solutions, as they can manage and secure their data internally. However, this model requires significant upfront investment in hardware and software, as well as ongoing maintenance and upgrades. On the other hand, Cloud-based IVR systems are hosted on the service provider's infrastructure and accessed via the internet. This model offers several advantages, including lower initial costs, scalability, and ease of deployment. Businesses can quickly implement and scale their IVR systems without the need for extensive IT resources. Cloud-based solutions also provide flexibility, allowing organizations to pay for only the resources they use and easily adjust their capacity based on demand. Additionally, cloud providers often offer robust security measures and regular updates, ensuring that the IVR systems remain secure and up-to-date. The choice between on-premises and cloud-based IVR systems depends on various factors, including an organization's budget, IT capabilities, and specific needs. While on-premises solutions offer greater control and customization, cloud-based systems provide flexibility, scalability, and cost-effectiveness. As the market for IVR systems continues to evolve, many organizations are opting for hybrid models that combine the benefits of both on-premises and cloud-based solutions. This approach allows businesses to leverage the strengths of each model, optimizing their IVR systems to meet their unique requirements. The decision to adopt an on-premises or cloud-based IVR system ultimately depends on an organization's strategic goals, resources, and priorities. As technology advances and the demand for efficient customer interaction solutions grows, the Global Interactive Voice Response Systems Market is likely to see continued innovation and diversification in deployment models.

Government/Public Sector, BFSI, IT and Telecommunication, Energy and Power, Retail and E-Commerce, Manufacturing, Healthcare, Others in the Global Interactive Voice Response Systems Market:

The Global Interactive Voice Response Systems Market finds extensive application across various sectors, each leveraging the technology to enhance operational efficiency and customer interaction. In the Government and Public Sector, IVR systems are used to manage high volumes of citizen inquiries, streamline service delivery, and provide 24/7 access to information. These systems help government agencies reduce wait times, improve service accessibility, and efficiently allocate resources. In the Banking, Financial Services, and Insurance (BFSI) sector, IVR systems play a crucial role in automating customer service processes, such as balance inquiries, transaction details, and loan applications. By providing quick and secure access to information, IVR systems enhance customer satisfaction and reduce the workload on human agents. The IT and Telecommunication industry utilizes IVR systems to manage customer support, troubleshoot technical issues, and offer self-service options. These systems help telecom companies handle large volumes of calls, reduce operational costs, and improve customer experience. In the Energy and Power sector, IVR systems are used to manage customer inquiries, report outages, and provide billing information. By automating routine tasks, energy companies can focus on critical operations and improve service reliability. The Retail and E-Commerce industry leverages IVR systems to handle customer inquiries, process orders, and provide product information. These systems enable retailers to offer personalized customer experiences, streamline operations, and enhance customer loyalty. In the Manufacturing sector, IVR systems are used to manage supply chain inquiries, track orders, and provide real-time updates. By automating communication processes, manufacturers can improve efficiency and reduce operational costs. The Healthcare industry utilizes IVR systems to manage patient appointments, provide medical information, and handle billing inquiries. These systems help healthcare providers improve patient engagement, reduce administrative workload, and enhance service delivery. Other sectors, such as travel, hospitality, and education, also benefit from IVR systems by automating customer interactions and improving service efficiency. As the demand for efficient and cost-effective communication solutions grows, the Global Interactive Voice Response Systems Market is expected to see continued adoption across various industries.

Global Interactive Voice Response Systems Market Outlook:

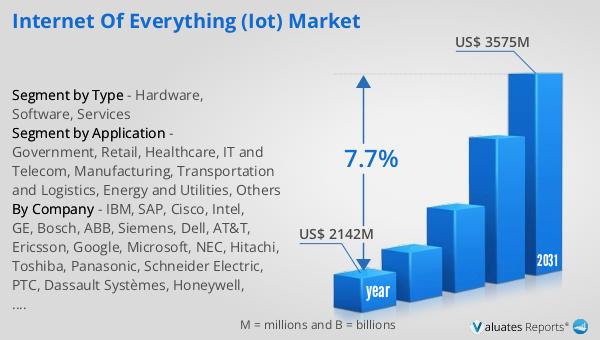

The global market for Interactive Voice Response Systems was valued at $4,597 million in 2024 and is anticipated to grow significantly, reaching an estimated value of $6,395 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 4.9% over the forecast period. The increasing adoption of IVR systems across various industries is a key driver of this market expansion. Organizations are recognizing the benefits of automating customer interactions, which include improved efficiency, reduced operational costs, and enhanced customer satisfaction. As businesses strive to provide seamless and personalized customer experiences, the demand for advanced IVR systems is expected to rise. Additionally, technological advancements, such as the integration of artificial intelligence and natural language processing, are enhancing the capabilities of IVR systems, making them more intuitive and user-friendly. These innovations are likely to further fuel market growth as organizations seek to leverage cutting-edge technology to optimize their customer service operations. The projected growth of the Global Interactive Voice Response Systems Market underscores the increasing importance of efficient communication solutions in today's fast-paced business environment. As more organizations invest in IVR technology, the market is poised for continued expansion and innovation.

| Report Metric | Details |

| Report Name | Interactive Voice Response Systems Market |

| Accounted market size in year | US$ 4597 million |

| Forecasted market size in 2031 | US$ 6395 million |

| CAGR | 4.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | IBM, Accenture, Cisco, CrowdStrike, FireEye, McAfee, NTT, Optiv, Rapid7, Symantec, Trustwave, Verizon, Booz Allen Hamilton, Stroz Friedberg (AON), Check Point, Secureworks (Dell), BAE Systems, PricewaterhouseCoopers (PWC), Cylance, DXC, RSA, Deloitte, KPMG International, Ernst & Young |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |