What is Global Big Data in Automotive Market?

Global Big Data in the Automotive Market refers to the extensive use of large volumes of data generated by vehicles and related systems to enhance various aspects of the automotive industry. This data is collected from numerous sources, including sensors, GPS devices, social media, and customer feedback, and is used to improve vehicle performance, safety, and customer satisfaction. By analyzing this data, automotive companies can gain valuable insights into consumer preferences, driving patterns, and vehicle usage, which can inform product development and marketing strategies. Additionally, Big Data helps in predictive maintenance, reducing downtime by anticipating potential issues before they occur. It also plays a crucial role in the development of autonomous vehicles by providing the necessary data for machine learning algorithms to improve decision-making processes. Overall, the integration of Big Data in the automotive sector is transforming the industry by enabling more efficient operations, personalized customer experiences, and innovative technological advancements.

Hardware, Software, Professional Services in the Global Big Data in Automotive Market:

In the Global Big Data in Automotive Market, hardware, software, and professional services play pivotal roles in harnessing the power of data. Hardware components include sensors, GPS devices, and onboard diagnostics systems that collect real-time data from vehicles. These devices are crucial for gathering information on vehicle performance, location, and environmental conditions. The data collected by these hardware components is then transmitted to centralized systems for analysis. Software solutions are equally important, as they process and analyze the vast amounts of data generated by the hardware. Advanced analytics software, machine learning algorithms, and artificial intelligence tools are employed to extract meaningful insights from the data. These insights can be used to optimize vehicle performance, enhance safety features, and improve customer experiences. For instance, predictive analytics can identify patterns in vehicle data to anticipate maintenance needs, reducing the risk of breakdowns and improving overall reliability. Furthermore, software platforms enable seamless integration of data from various sources, facilitating a comprehensive view of vehicle operations and customer interactions. Professional services, on the other hand, encompass a range of activities that support the implementation and management of Big Data solutions in the automotive industry. These services include consulting, system integration, and data management. Consulting services help automotive companies identify the most effective strategies for leveraging Big Data to achieve their business objectives. System integration services ensure that hardware and software components work together seamlessly, enabling efficient data collection and analysis. Data management services focus on organizing and maintaining the vast amounts of data generated by vehicles, ensuring its accuracy, security, and accessibility. Additionally, professional services provide training and support to help automotive companies maximize the value of their Big Data investments. By combining hardware, software, and professional services, the Global Big Data in Automotive Market enables automotive companies to unlock the full potential of data-driven insights, driving innovation and competitiveness in the industry.

Customer, Automobile Manufacturer, Automobile Service Provider, Transportation Management Company, Other in the Global Big Data in Automotive Market:

The usage of Global Big Data in the Automotive Market spans various areas, including customers, automobile manufacturers, automobile service providers, transportation management companies, and others. For customers, Big Data offers personalized experiences by analyzing their preferences and driving habits. This data-driven approach allows automotive companies to tailor their offerings to individual needs, enhancing customer satisfaction and loyalty. For instance, by analyzing data from connected vehicles, companies can offer personalized maintenance reminders, route suggestions, and infotainment options. Automobile manufacturers leverage Big Data to optimize production processes and improve product quality. By analyzing data from the manufacturing floor, companies can identify inefficiencies and implement corrective measures, reducing waste and enhancing productivity. Additionally, Big Data enables manufacturers to monitor the performance of vehicles in real-time, allowing for proactive maintenance and timely recalls if necessary. This not only improves vehicle reliability but also enhances brand reputation. Automobile service providers benefit from Big Data by offering predictive maintenance services. By analyzing data from vehicle sensors, service providers can anticipate potential issues and address them before they lead to costly repairs. This proactive approach reduces downtime for customers and increases the efficiency of service operations. Transportation management companies use Big Data to optimize logistics and fleet management. By analyzing data on traffic patterns, fuel consumption, and vehicle performance, these companies can make informed decisions to improve route planning, reduce fuel costs, and enhance overall operational efficiency. Furthermore, Big Data enables transportation companies to monitor driver behavior, ensuring compliance with safety regulations and reducing the risk of accidents. Other areas where Big Data is utilized include insurance companies, which use data to assess risk and determine premiums, and government agencies, which leverage data to improve traffic management and infrastructure planning. Overall, the integration of Big Data in the automotive market is transforming the industry by enabling more efficient operations, personalized customer experiences, and innovative technological advancements.

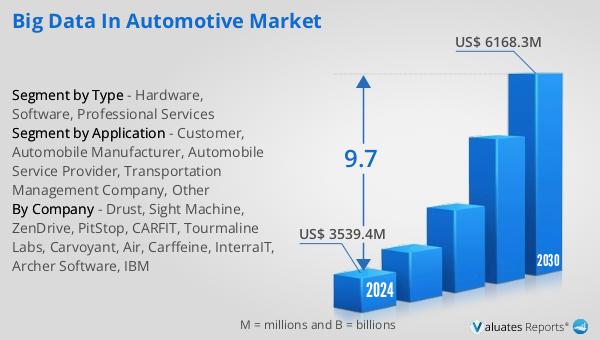

Global Big Data in Automotive Market Outlook:

The outlook for the Global Big Data in Automotive Market indicates a significant growth trajectory over the coming years. The market is expected to expand from a valuation of US$ 3539.4 million in 2024 to US$ 6168.3 million by 2030. This growth represents a Compound Annual Growth Rate (CAGR) of 9.7% during the forecast period. Such a robust growth rate underscores the increasing importance of Big Data in the automotive industry. As automotive companies continue to recognize the value of data-driven insights, investments in Big Data technologies are expected to rise. This growth is driven by several factors, including the increasing adoption of connected vehicles, advancements in data analytics technologies, and the growing demand for personalized customer experiences. Additionally, the rise of autonomous vehicles and the need for real-time data processing are expected to further fuel the demand for Big Data solutions in the automotive sector. As the market continues to evolve, companies that effectively leverage Big Data will be well-positioned to gain a competitive edge, driving innovation and enhancing customer satisfaction. Overall, the Global Big Data in Automotive Market is poised for substantial growth, offering numerous opportunities for companies to capitalize on the power of data-driven insights.

| Report Metric | Details |

| Report Name | Big Data in Automotive Market |

| Accounted market size in 2024 | US$ 3539.4 million |

| Forecasted market size in 2030 | US$ 6168.3 million |

| CAGR | 9.7 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Drust, Sight Machine, ZenDrive, PitStop, CARFIT, Tourmaline Labs, Carvoyant, Air, Carffeine, InterraIT, Archer Software, IBM |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |