What is Global Zero Liquid Discharge (ZLD) Market?

The Global Zero Liquid Discharge (ZLD) Market is a rapidly evolving sector focused on sustainable water management solutions. ZLD is a wastewater treatment process that ensures no liquid waste is discharged into the environment, thereby promoting water conservation and reducing pollution. This market is driven by increasing environmental regulations and the need for sustainable industrial practices. Industries such as power generation, chemicals, and textiles are major contributors to wastewater, and ZLD systems help these sectors comply with stringent discharge regulations. The market is characterized by the adoption of advanced technologies and innovative solutions to achieve complete water recycling and reuse. As industries strive to minimize their environmental footprint, the demand for ZLD systems is expected to grow. The market is also influenced by factors such as rising water scarcity, increasing industrialization, and the need for efficient water management systems. Companies operating in this market are focusing on developing cost-effective and energy-efficient ZLD solutions to cater to the diverse needs of various industries. Overall, the Global ZLD Market plays a crucial role in promoting sustainable water management practices and ensuring environmental compliance across industries.

Conventional ZLD System, Hybrid ZLD System in the Global Zero Liquid Discharge (ZLD) Market:

Conventional Zero Liquid Discharge (ZLD) systems are traditional methods used to treat and recycle wastewater, ensuring that no liquid waste is released into the environment. These systems typically involve a series of processes, including pretreatment, evaporation, and crystallization, to remove contaminants and recover clean water. Pretreatment involves the removal of suspended solids and other impurities from the wastewater, preparing it for further treatment. Evaporation is a key step in conventional ZLD systems, where the wastewater is heated to separate water from dissolved solids. This process often requires significant energy input, making it a costly option for some industries. Crystallization follows evaporation, where the remaining concentrated brine is further processed to extract solid salts, leaving behind minimal liquid waste. Conventional ZLD systems are widely used in industries with high wastewater discharge volumes, such as power plants and chemical manufacturing. However, the high energy consumption and operational costs associated with these systems have led to the development of more efficient alternatives. Hybrid ZLD systems, on the other hand, combine conventional methods with advanced technologies to enhance efficiency and reduce costs. These systems integrate processes such as membrane filtration, reverse osmosis, and forward osmosis to optimize water recovery and minimize energy usage. Membrane filtration is used to separate suspended solids and dissolved contaminants from the wastewater, reducing the load on subsequent treatment processes. Reverse osmosis is employed to concentrate the wastewater further, allowing for higher water recovery rates. Forward osmosis, a relatively newer technology, uses natural osmotic pressure to draw water through a semi-permeable membrane, leaving behind concentrated brine. By combining these technologies, hybrid ZLD systems offer a more sustainable and cost-effective solution for industries seeking to achieve zero liquid discharge. They are particularly beneficial for sectors with stringent environmental regulations and high water consumption, such as pharmaceuticals and textiles. The integration of advanced technologies in hybrid ZLD systems not only improves water recovery rates but also reduces the overall environmental impact of industrial operations. As industries continue to prioritize sustainability and resource efficiency, the adoption of hybrid ZLD systems is expected to increase. These systems provide a viable alternative to conventional methods, offering enhanced performance and reduced operational costs. In conclusion, both conventional and hybrid ZLD systems play a vital role in the Global ZLD Market, catering to the diverse needs of various industries and promoting sustainable water management practices.

Energy & Power, Food & Beverages, Chemicals & Petrochemicals, Textile, Pharmaceuticals, Others in the Global Zero Liquid Discharge (ZLD) Market:

The Global Zero Liquid Discharge (ZLD) Market finds extensive application across various industries, including Energy & Power, Food & Beverages, Chemicals & Petrochemicals, Textile, Pharmaceuticals, and others. In the Energy & Power sector, ZLD systems are crucial for managing the large volumes of wastewater generated during power generation processes. These systems help power plants comply with stringent environmental regulations by ensuring that no liquid waste is discharged into the environment. By recovering and reusing water, ZLD systems also contribute to reducing the overall water consumption of power plants, promoting sustainable operations. In the Food & Beverages industry, ZLD systems are used to treat wastewater generated during food processing and production. These systems help companies meet regulatory requirements and maintain high standards of hygiene and safety. By recycling water, ZLD systems also enable food and beverage manufacturers to reduce their water footprint and enhance their sustainability efforts. The Chemicals & Petrochemicals industry is another major user of ZLD systems, as it generates significant volumes of wastewater containing hazardous chemicals and pollutants. ZLD systems help these industries treat and recycle wastewater, ensuring compliance with environmental regulations and minimizing the risk of pollution. In the Textile industry, ZLD systems are used to manage the large volumes of wastewater generated during dyeing and finishing processes. These systems help textile manufacturers reduce their environmental impact by recovering and reusing water, as well as minimizing the discharge of harmful chemicals into the environment. The Pharmaceuticals industry also relies on ZLD systems to treat and recycle wastewater generated during drug manufacturing processes. These systems help pharmaceutical companies comply with stringent regulatory requirements and ensure the safe disposal of hazardous waste. Other industries, such as mining and pulp & paper, also benefit from the use of ZLD systems to manage their wastewater and promote sustainable operations. Overall, the Global ZLD Market plays a vital role in helping industries across various sectors achieve their sustainability goals and comply with environmental regulations. By promoting efficient water management practices, ZLD systems contribute to reducing the environmental impact of industrial operations and ensuring the responsible use of water resources.

Global Zero Liquid Discharge (ZLD) Market Outlook:

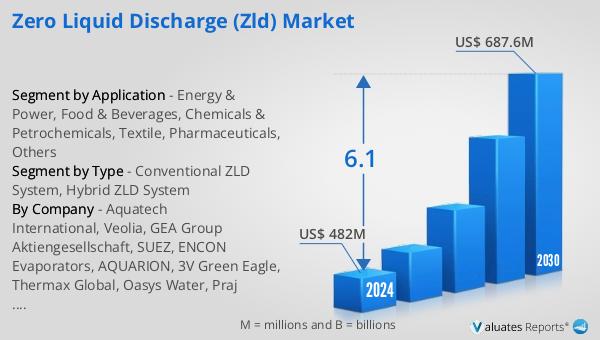

The global Zero Liquid Discharge (ZLD) market is anticipated to experience significant growth over the coming years. Starting from a valuation of US$ 482 million in 2024, it is expected to reach approximately US$ 687.6 million by 2030. This growth trajectory represents a Compound Annual Growth Rate (CAGR) of 6.1% throughout the forecast period. This upward trend is largely driven by increasing environmental regulations and the growing need for sustainable industrial practices. As industries across the globe face mounting pressure to reduce their environmental footprint, the demand for ZLD systems is expected to rise. These systems offer a viable solution for industries looking to comply with stringent discharge regulations while promoting water conservation and reducing pollution. The market is also influenced by factors such as rising water scarcity, increasing industrialization, and the need for efficient water management systems. Companies operating in this market are focusing on developing cost-effective and energy-efficient ZLD solutions to cater to the diverse needs of various industries. As a result, the Global ZLD Market is poised for substantial growth, playing a crucial role in promoting sustainable water management practices and ensuring environmental compliance across industries.

| Report Metric | Details |

| Report Name | Zero Liquid Discharge (ZLD) Market |

| Accounted market size in 2024 | US$ 482 million |

| Forecasted market size in 2030 | US$ 687.6 million |

| CAGR | 6.1 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Aquatech International, Veolia, GEA Group Aktiengesellschaft, SUEZ, ENCON Evaporators, AQUARION, 3V Green Eagle, Thermax Global, Oasys Water, Praj Industries, Kelvin Water Technologies, Transparent Energy System, Austro Chemicals & Bio Technologies, Bionics Advanced Filtration Systems, Dew Envirotech, Arvind Envisol |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |