What is Global Dew Point Analyzer Market?

The Global Dew Point Analyzer Market refers to the industry focused on the production and sale of devices that measure the dew point of gases. Dew point is the temperature at which air becomes saturated with moisture and water vapor begins to condense into liquid. These analyzers are crucial in various industries as they help in monitoring and controlling moisture levels, ensuring the quality and safety of products and processes. The market for dew point analyzers is expanding due to increasing demand across sectors such as oil and gas, pharmaceuticals, food and beverage, and more. These devices are essential for maintaining optimal conditions in manufacturing and processing environments, preventing corrosion, and ensuring the efficiency of operations. As industries continue to prioritize quality control and operational efficiency, the demand for accurate and reliable dew point measurement tools is expected to grow. The market is characterized by a range of products, including desktop, handheld, and in-line analyzers, each catering to different needs and applications. With technological advancements, these devices are becoming more sophisticated, offering enhanced accuracy and ease of use, further driving their adoption across various sectors.

Desktop, Handheld, In-line in the Global Dew Point Analyzer Market:

In the Global Dew Point Analyzer Market, there are three primary types of devices: desktop, handheld, and in-line analyzers. Each type serves specific purposes and is designed to meet the diverse needs of different industries. Desktop dew point analyzers are typically used in laboratory settings or fixed locations where precise and continuous monitoring is required. These devices are known for their high accuracy and ability to provide detailed analysis of moisture content in gases. They are often equipped with advanced features such as data logging, remote monitoring, and connectivity options, making them ideal for research and development applications. Handheld dew point analyzers, on the other hand, offer portability and convenience, allowing users to conduct on-site measurements quickly and efficiently. These devices are compact and lightweight, making them suitable for fieldwork and situations where mobility is essential. Handheld analyzers are commonly used in industries such as HVAC, where technicians need to assess moisture levels in various locations. Despite their smaller size, many handheld models offer impressive accuracy and functionality, often rivaling their desktop counterparts. In-line dew point analyzers are integrated directly into industrial processes, providing real-time monitoring and control of moisture levels. These devices are crucial in applications where continuous measurement is necessary to maintain product quality and process efficiency. In-line analyzers are often used in the oil and gas industry, where they help prevent pipeline corrosion and ensure the integrity of natural gas. They are also employed in manufacturing processes where moisture content can significantly impact product quality, such as in the production of plastics and chemicals. The choice between desktop, handheld, and in-line analyzers depends on factors such as the specific application, required accuracy, and operational environment. Each type of analyzer offers unique advantages, and the decision often involves balancing the need for precision, convenience, and integration with existing systems. As technology continues to advance, these devices are becoming more sophisticated, offering enhanced features and capabilities that cater to the evolving needs of various industries. The Global Dew Point Analyzer Market is thus characterized by a diverse range of products, each designed to meet the specific demands of different applications, ensuring that industries can effectively monitor and control moisture levels to maintain quality and efficiency.

Pharmaceuticals, Food and Beverage, Wood, Paper and Pulp, Others in the Global Dew Point Analyzer Market:

The Global Dew Point Analyzer Market finds extensive usage across various industries, including pharmaceuticals, food and beverage, wood, paper and pulp, and others. In the pharmaceutical industry, maintaining precise moisture levels is crucial for ensuring the stability and efficacy of drugs. Dew point analyzers are used to monitor and control humidity in manufacturing environments, preventing moisture-related issues such as degradation and contamination. These devices help ensure that pharmaceutical products meet stringent quality standards and regulatory requirements. In the food and beverage industry, dew point analyzers play a vital role in maintaining product quality and safety. Moisture control is essential in food processing and packaging to prevent spoilage, mold growth, and other quality issues. Dew point analyzers help manufacturers optimize their processes, ensuring that products remain fresh and safe for consumption. In the wood, paper, and pulp industry, controlling moisture content is critical for maintaining the quality and structural integrity of products. Dew point analyzers are used to monitor humidity levels during production and storage, preventing issues such as warping, cracking, and degradation. These devices help manufacturers produce high-quality products that meet industry standards and customer expectations. Beyond these industries, dew point analyzers are also used in sectors such as electronics, automotive, and aerospace, where moisture control is essential for ensuring the reliability and performance of products and systems. In electronics manufacturing, for example, controlling humidity is crucial to prevent corrosion and damage to sensitive components. In the automotive and aerospace industries, dew point analyzers help maintain optimal conditions for manufacturing and testing, ensuring the safety and performance of vehicles and aircraft. Overall, the Global Dew Point Analyzer Market serves a wide range of industries, providing essential tools for monitoring and controlling moisture levels to ensure product quality, safety, and efficiency. As industries continue to prioritize quality control and operational efficiency, the demand for accurate and reliable dew point measurement tools is expected to grow, driving the expansion of the market.

Global Dew Point Analyzer Market Outlook:

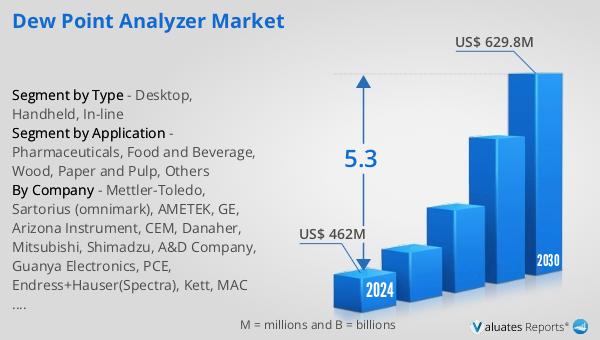

The outlook for the Global Dew Point Analyzer Market indicates a promising growth trajectory. It is anticipated that the market will expand from a valuation of $462 million in 2024 to approximately $629.8 million by 2030. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of 5.3% over the forecast period. This projected increase in market size reflects the rising demand for dew point analyzers across various industries, driven by the need for precise moisture measurement and control. As industries continue to prioritize quality assurance and operational efficiency, the adoption of advanced dew point analyzers is likely to increase. The market's growth is also supported by technological advancements that enhance the accuracy, reliability, and ease of use of these devices. With the ongoing emphasis on maintaining optimal conditions in manufacturing and processing environments, the Global Dew Point Analyzer Market is poised for significant expansion. This growth will be fueled by the increasing awareness of the importance of moisture control in ensuring product quality and safety, as well as the continuous development of innovative solutions that cater to the evolving needs of different industries. As a result, the market is expected to witness robust demand and investment, driving further advancements and opportunities in the field of dew point analysis.

| Report Metric | Details |

| Report Name | Dew Point Analyzer Market |

| Accounted market size in 2024 | US$ 462 million |

| Forecasted market size in 2030 | US$ 629.8 million |

| CAGR | 5.3 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Mettler-Toledo, Sartorius (omnimark), AMETEK, GE, Arizona Instrument, CEM, Danaher, Mitsubishi, Shimadzu, A&D Company, Guanya Electronics, PCE, Endress+Hauser(Spectra), Kett, MAC Instruments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |