What is Global Healthcare Inventory Management Market?

The Global Healthcare Inventory Management Market is a crucial component of the healthcare industry, focusing on the efficient management of medical supplies, pharmaceuticals, and equipment within healthcare facilities. This market encompasses a range of solutions designed to streamline inventory processes, reduce waste, and ensure the availability of necessary items when needed. By leveraging advanced technologies such as RFID (Radio Frequency Identification), barcode systems, and IoT (Internet of Things) devices, healthcare providers can track and manage their inventory in real-time. This not only helps in maintaining optimal stock levels but also minimizes the risk of stockouts or overstocking, which can lead to increased costs and compromised patient care. The market is driven by the growing demand for automation in healthcare settings, the need for cost reduction, and the increasing focus on patient safety and care quality. As healthcare facilities continue to expand and evolve, the importance of effective inventory management becomes even more critical, making this market an essential aspect of modern healthcare operations.

Hardware, Software, Service in the Global Healthcare Inventory Management Market:

In the Global Healthcare Inventory Management Market, hardware, software, and services play pivotal roles in ensuring the seamless operation of inventory systems. Hardware components include devices such as RFID tags, barcode scanners, and IoT sensors, which are essential for tracking and monitoring inventory items. These devices capture data that is crucial for maintaining accurate inventory records and ensuring that healthcare providers have the necessary supplies at their disposal. RFID technology, for instance, allows for the automatic identification and tracking of inventory items, reducing the need for manual counting and minimizing human error. Barcode scanners, on the other hand, provide a cost-effective solution for inventory management by enabling quick and accurate data entry. Software solutions in this market are designed to integrate with hardware components and provide a comprehensive platform for managing inventory data. These software systems offer features such as real-time tracking, automated reordering, and analytics, which help healthcare facilities optimize their inventory processes. By analyzing data collected from hardware devices, software solutions can generate insights into inventory usage patterns, identify inefficiencies, and suggest improvements. This not only enhances the overall efficiency of inventory management but also supports better decision-making by healthcare administrators. Services in the Global Healthcare Inventory Management Market encompass a range of offerings that support the implementation and maintenance of inventory systems. These services include consulting, training, and technical support, which are essential for ensuring that healthcare facilities can effectively utilize their inventory management solutions. Consulting services help organizations assess their current inventory processes and identify areas for improvement, while training programs equip staff with the necessary skills to operate new systems. Technical support ensures that any issues with hardware or software components are promptly addressed, minimizing downtime and maintaining the continuity of inventory operations. Together, hardware, software, and services form a comprehensive ecosystem that enables healthcare facilities to manage their inventory more effectively. By investing in these solutions, healthcare providers can reduce costs, improve patient care, and enhance operational efficiency. As the demand for healthcare services continues to grow, the importance of robust inventory management systems becomes increasingly apparent, making this market a critical area of focus for healthcare organizations worldwide.

Hospital, Large Clinic in the Global Healthcare Inventory Management Market:

The usage of the Global Healthcare Inventory Management Market in hospitals and large clinics is integral to their daily operations, ensuring that these facilities can provide high-quality care to patients. In hospitals, inventory management systems are used to track a wide range of items, including medical supplies, pharmaceuticals, and surgical instruments. By implementing advanced inventory solutions, hospitals can maintain optimal stock levels, reduce waste, and ensure that critical items are always available when needed. This is particularly important in emergency situations, where the timely availability of medical supplies can be a matter of life and death. Additionally, effective inventory management helps hospitals reduce costs by minimizing overstocking and preventing the expiration of unused items. Large clinics, which often operate with fewer resources than hospitals, also benefit significantly from robust inventory management systems. These clinics rely on inventory solutions to manage their supplies efficiently, ensuring that they can continue to provide care without interruption. By automating inventory processes, large clinics can reduce the time and effort required for manual inventory checks, allowing staff to focus more on patient care. Furthermore, inventory management systems provide clinics with valuable insights into their supply usage patterns, enabling them to make informed decisions about purchasing and stocking. Both hospitals and large clinics face the challenge of balancing cost control with the need to provide high-quality care. Inventory management systems help address this challenge by optimizing the use of resources and ensuring that supplies are used efficiently. By reducing waste and improving the accuracy of inventory records, these systems contribute to better financial management and support the overall sustainability of healthcare operations. As healthcare facilities continue to face increasing pressure to deliver cost-effective care, the role of inventory management in hospitals and large clinics becomes even more critical.

Global Healthcare Inventory Management Market Outlook:

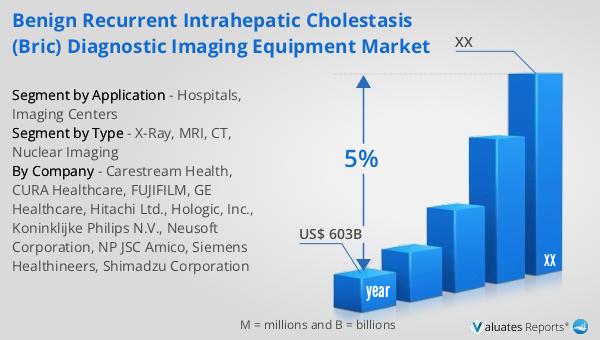

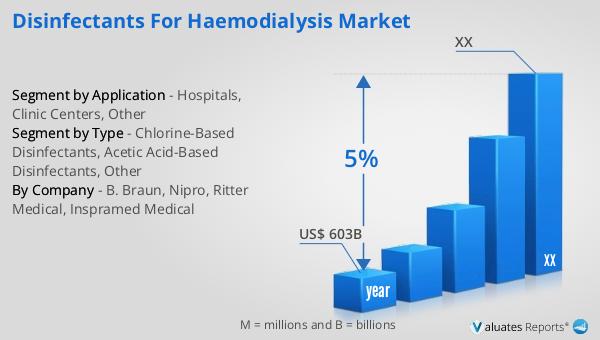

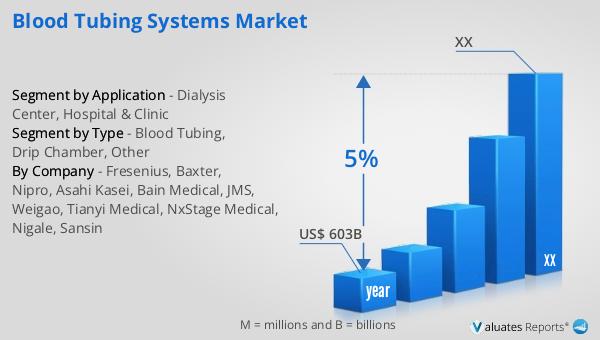

Our research indicates that the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth reflects the increasing demand for medical devices driven by advancements in healthcare technology, an aging population, and the rising prevalence of chronic diseases. As healthcare systems worldwide strive to improve patient outcomes and enhance the quality of care, the need for innovative medical devices continues to grow. This market expansion is also fueled by the ongoing development of new technologies, such as wearable devices, telemedicine solutions, and minimally invasive surgical instruments, which are transforming the way healthcare is delivered. Additionally, the increasing focus on personalized medicine and the integration of artificial intelligence in medical devices are expected to further drive market growth. As a result, healthcare providers and manufacturers are investing heavily in research and development to bring new and improved medical devices to market, ensuring that they can meet the evolving needs of patients and healthcare professionals alike.

| Report Metric | Details |

| Report Name | Healthcare Inventory Management Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | LogiTag Systems, Mobile Aspects, TAGSYS RFID, Terson Solutions, WaveMark, Sato Vicinity, Grifols, Skytron, Palex Medical, Nexess |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |