What is Global PACS Systems Market?

The Global PACS Systems Market refers to the worldwide market for Picture Archiving and Communication Systems (PACS), which are medical imaging technology solutions used to securely store, retrieve, manage, distribute, and present medical images. These systems are crucial in healthcare settings as they replace traditional film-based methods of managing medical images with digital alternatives, thereby improving efficiency and accessibility. PACS systems are used extensively in radiology, cardiology, oncology, and other medical fields that rely heavily on imaging for diagnosis and treatment planning. The market encompasses various types of PACS solutions, including web-based, cloud-based, and on-premise systems, each offering different advantages in terms of accessibility, cost, and data management. The growth of this market is driven by the increasing demand for efficient and scalable imaging solutions, advancements in medical imaging technologies, and the rising prevalence of chronic diseases that require regular imaging for monitoring and treatment. Additionally, the integration of PACS with other healthcare IT systems, such as Electronic Health Records (EHRs), enhances the overall efficiency of healthcare delivery, further propelling market growth. As healthcare providers continue to seek ways to improve patient care and streamline operations, the adoption of PACS systems is expected to rise globally.

Web-based, Cloud-based in the Global PACS Systems Market:

Web-based and cloud-based PACS systems are two prominent types of solutions within the Global PACS Systems Market, each offering unique benefits and addressing specific needs of healthcare providers. Web-based PACS systems are designed to be accessed through a web browser, allowing healthcare professionals to view and manage medical images from any location with internet connectivity. This flexibility is particularly beneficial for healthcare facilities with multiple locations or for specialists who need to consult on cases remotely. Web-based systems typically require less upfront investment compared to traditional on-premise solutions, as they do not necessitate extensive hardware installations. Instead, they rely on centralized servers that store and manage the data, which can be accessed by authorized users through secure login credentials. This setup not only reduces costs but also simplifies maintenance and updates, as these can be managed centrally by the service provider.

Diagnostic Centers, Hospitals, Clinics in the Global PACS Systems Market:

Cloud-based PACS systems take the concept of web-based solutions a step further by leveraging cloud computing technology to store and manage medical images. In a cloud-based setup, images are stored on remote servers maintained by third-party cloud service providers, which can offer significant advantages in terms of scalability, data redundancy, and disaster recovery. Cloud-based PACS systems allow healthcare providers to scale their storage needs up or down based on demand, without the need for additional physical infrastructure. This scalability is particularly advantageous for large healthcare networks or facilities experiencing rapid growth. Additionally, cloud-based systems often come with robust data backup and recovery solutions, ensuring that medical images are protected against data loss due to hardware failures or other unforeseen events.

Global PACS Systems Market Outlook:

One of the key benefits of cloud-based PACS is the ability to facilitate collaboration among healthcare professionals. Since images can be accessed from any location with internet connectivity, specialists from different geographic locations can easily collaborate on patient cases, leading to more informed decision-making and improved patient outcomes. Furthermore, cloud-based systems often offer advanced analytics and artificial intelligence (AI) capabilities, enabling healthcare providers to gain deeper insights from medical images and improve diagnostic accuracy. However, the adoption of cloud-based PACS systems also raises concerns about data security and privacy, as sensitive patient information is stored on external servers. To address these concerns, cloud service providers implement stringent security measures, such as encryption, access controls, and regular security audits, to ensure that patient data is protected.

| Report Metric | Details |

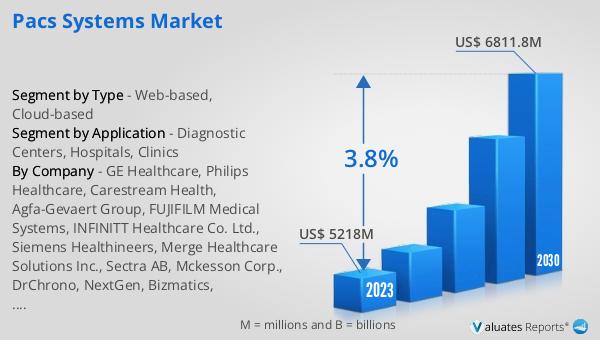

| Report Name | PACS Systems Market |

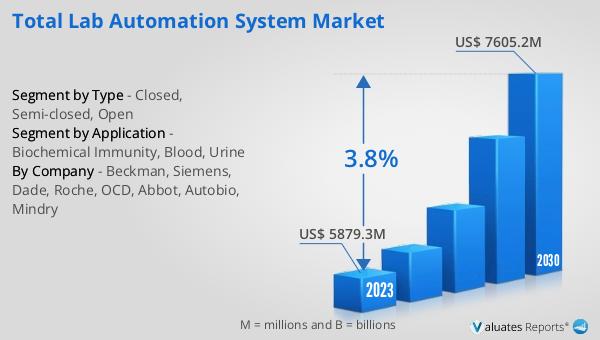

| Accounted market size in 2024 | US$ 5446 million |

| Forecasted market size in 2030 | US$ 6811.8 million |

| CAGR | 3.8 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | GE Healthcare, Philips Healthcare, Carestream Health, Agfa-Gevaert Group, FUJIFILM Medical Systems, INFINITT Healthcare Co. Ltd., Siemens Healthineers, Merge Healthcare Solutions Inc., Sectra AB, Mckesson Corp., DrChrono, NextGen, Bizmatics, Compulink Healthcare Solutions, zHealth, Modernizing Medicine, Remedly, ReLi Med Solutions |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |