What is Global Digital Agriculture Market?

The Global Digital Agriculture Market refers to the integration of advanced technologies into farming practices to enhance productivity, efficiency, and sustainability. This market encompasses a wide range of digital tools and solutions, including sensors, drones, GPS technology, and data analytics, which collectively transform traditional agricultural methods. By leveraging these technologies, farmers can monitor crop health, optimize resource usage, and make data-driven decisions to improve yields and reduce environmental impact. The digital agriculture market is driven by the increasing demand for food due to a growing global population, the need for sustainable farming practices, and the rising adoption of precision farming techniques. Additionally, government initiatives and investments in agricultural technology further propel the market's growth. As a result, digital agriculture is becoming an essential component of modern farming, offering solutions that address challenges such as climate change, resource scarcity, and the need for increased food production. This market is poised for significant expansion as more farmers and agricultural stakeholders recognize the benefits of integrating digital technologies into their operations.

Farming Equipment, Management Software, Other Service in the Global Digital Agriculture Market:

Farming equipment in the Global Digital Agriculture Market includes a variety of advanced machinery and tools designed to enhance agricultural productivity and efficiency. These include GPS-enabled tractors, automated harvesters, and precision seeders, which allow farmers to perform tasks with greater accuracy and less manual labor. GPS technology, for instance, enables tractors to follow precise paths, reducing overlap and ensuring even distribution of seeds and fertilizers. Automated harvesters can operate continuously, increasing the speed and efficiency of crop collection. Precision seeders ensure that seeds are planted at optimal depths and spacing, maximizing germination rates and crop yields. Management software is another critical component of the digital agriculture market, providing farmers with the ability to collect, analyze, and interpret data from various sources. This software helps in monitoring crop health, predicting weather patterns, and managing resources such as water and fertilizers. By using management software, farmers can make informed decisions that optimize their operations, reduce waste, and increase profitability. For example, data analytics can identify trends and patterns in crop growth, allowing farmers to adjust their practices accordingly. Other services in the digital agriculture market include consulting, training, and support services that help farmers implement and maintain digital technologies. These services ensure that farmers can effectively use digital tools and maximize their benefits. Consulting services provide expert advice on selecting and integrating the right technologies for specific farming needs. Training programs educate farmers on how to use digital tools and interpret data, while support services offer ongoing assistance to address any technical issues that may arise. Together, these components of the digital agriculture market work synergistically to transform traditional farming practices, making them more efficient, sustainable, and profitable. As the market continues to evolve, new innovations and technologies are expected to emerge, further enhancing the capabilities of digital agriculture.

Greenhouse, Farm, Other in the Global Digital Agriculture Market:

The usage of the Global Digital Agriculture Market in greenhouses, farms, and other areas is transforming the way agricultural activities are conducted. In greenhouses, digital agriculture technologies are used to monitor and control environmental conditions such as temperature, humidity, and light levels. Sensors and automated systems can adjust these parameters in real-time, ensuring optimal growing conditions for plants. This leads to increased yields, reduced resource consumption, and improved crop quality. Additionally, data analytics can help greenhouse operators predict and prevent issues such as pest infestations or diseases, further enhancing productivity. On farms, digital agriculture technologies enable precision farming practices that optimize resource usage and improve crop management. GPS-guided machinery ensures accurate planting, fertilization, and harvesting, reducing waste and increasing efficiency. Drones equipped with cameras and sensors can survey large areas quickly, providing valuable data on crop health and soil conditions. This information allows farmers to make informed decisions about irrigation, fertilization, and pest control, ultimately leading to higher yields and lower costs. Other areas where digital agriculture is making an impact include livestock management and supply chain optimization. In livestock management, sensors and monitoring systems track animal health, behavior, and environmental conditions, enabling farmers to improve animal welfare and productivity. For example, wearable devices can monitor vital signs and alert farmers to potential health issues before they become serious. In the supply chain, digital technologies enhance traceability and transparency, allowing consumers to access information about the origin and quality of their food. This not only improves food safety but also builds trust between producers and consumers. Overall, the Global Digital Agriculture Market is revolutionizing agricultural practices across various sectors, offering solutions that increase efficiency, sustainability, and profitability.

Global Digital Agriculture Market Outlook:

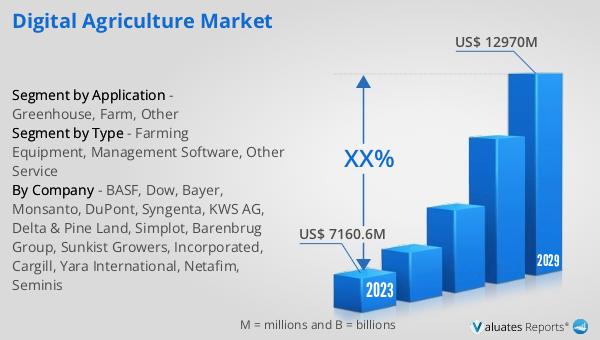

The global Digital Agriculture market is anticipated to experience significant growth over the coming years. Starting from a valuation of approximately US$ 7,160.6 million in 2024, it is expected to reach around US$ 12,970 million by 2030. This growth trajectory represents a Compound Annual Growth Rate (CAGR) of 10.4% during the forecast period. This substantial increase is driven by several factors, including the rising demand for food due to a growing global population and the need for sustainable farming practices. As more farmers and agricultural stakeholders recognize the benefits of digital technologies, the adoption of these solutions is expected to accelerate. The integration of advanced technologies such as sensors, drones, and data analytics into farming practices is transforming traditional agriculture, making it more efficient and productive. Additionally, government initiatives and investments in agricultural technology are further propelling the market's growth. As a result, the digital agriculture market is poised for significant expansion, offering innovative solutions that address challenges such as climate change, resource scarcity, and the need for increased food production. This growth not only benefits farmers by improving yields and reducing costs but also contributes to global food security and sustainability.

| Report Metric | Details |

| Report Name | Digital Agriculture Market |

| Accounted market size in 2024 | US$ 7160.6 in million |

| Forecasted market size in 2030 | US$ 12970 million |

| CAGR | 10.4 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | BASF, Dow, Bayer, Monsanto, DuPont, Syngenta, KWS AG, Delta & Pine Land, Simplot, Barenbrug Group, Sunkist Growers, Incorporated, Cargill, Yara International, Netafim, Seminis |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |