What is Global Silicone Adhesives and Sealants Market?

The Global Silicone Adhesives and Sealants Market is a dynamic and rapidly evolving sector that plays a crucial role in various industries worldwide. Silicone adhesives and sealants are versatile materials known for their excellent bonding properties, flexibility, and resistance to extreme temperatures and environmental conditions. These characteristics make them indispensable in applications ranging from construction and automotive to electronics and healthcare. The market is driven by the increasing demand for high-performance adhesives and sealants that can withstand harsh conditions and provide long-lasting durability. As industries continue to innovate and develop new technologies, the need for advanced silicone-based solutions is expected to grow. This market is characterized by a diverse range of products, each tailored to meet specific industry requirements, and is supported by ongoing research and development efforts to enhance product performance and sustainability. The global reach of this market underscores its importance in supporting infrastructure development, technological advancements, and the overall growth of various sectors.

Silicone Adhesives, Silicone Sealants, Others in the Global Silicone Adhesives and Sealants Market:

Silicone adhesives, silicone sealants, and other related products form the backbone of the Global Silicone Adhesives and Sealants Market, each serving distinct purposes across different industries. Silicone adhesives are renowned for their strong bonding capabilities, making them ideal for applications where a durable and flexible bond is required. They are commonly used in the automotive industry for bonding components that experience significant vibration and temperature fluctuations. In electronics, silicone adhesives provide reliable connections between components, ensuring stability and performance even in high-temperature environments. Silicone sealants, on the other hand, are primarily used to fill gaps and seal joints, preventing the ingress of moisture, dust, and other contaminants. Their elasticity and resistance to weathering make them perfect for use in construction, where they are applied to seal windows, doors, and other building elements. Additionally, silicone sealants are used in the aerospace industry to seal aircraft components, ensuring safety and efficiency. Beyond adhesives and sealants, the market also includes other silicone-based products that offer unique properties for specialized applications. These products are continually being developed to meet the evolving needs of industries, with a focus on enhancing performance, sustainability, and cost-effectiveness. The versatility and adaptability of silicone-based solutions make them indispensable in modern manufacturing and construction processes, driving the growth and expansion of the Global Silicone Adhesives and Sealants Market.

Building & Construction, Automobiles, Medical, Marine & Aerospace, Electrical & Electronics, Others in the Global Silicone Adhesives and Sealants Market:

The usage of silicone adhesives and sealants spans a wide range of industries, each benefiting from the unique properties of these materials. In the building and construction sector, silicone sealants are essential for ensuring the integrity and longevity of structures. They are used to seal joints and gaps in buildings, providing protection against water, air, and dust infiltration. This not only enhances the energy efficiency of buildings but also contributes to their overall durability and safety. In the automotive industry, silicone adhesives and sealants are used to bond and seal various components, from engine parts to interior trim. Their ability to withstand high temperatures and vibrations makes them ideal for use in vehicles, where they help improve performance and reduce noise. In the medical field, silicone adhesives are used in the production of medical devices and equipment, where their biocompatibility and flexibility are crucial. They are used to bond components in devices such as catheters and respiratory masks, ensuring patient safety and comfort. The marine and aerospace industries also rely on silicone sealants for their ability to withstand harsh environmental conditions, such as saltwater exposure and extreme temperatures. In these sectors, silicone sealants are used to seal joints and seams in ships and aircraft, ensuring structural integrity and safety. The electrical and electronics industry benefits from silicone adhesives and sealants for their insulating properties and resistance to heat and moisture. They are used to protect sensitive electronic components from environmental damage, ensuring reliable performance. Overall, the versatility and reliability of silicone adhesives and sealants make them indispensable across a wide range of applications, driving their demand and growth in the global market.

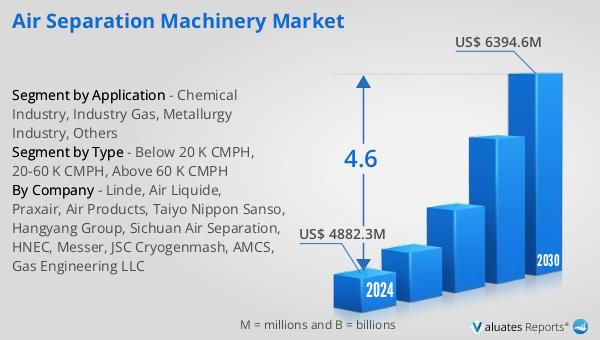

Global Silicone Adhesives and Sealants Market Outlook:

The outlook for the Global Silicone Adhesives and Sealants Market is promising, with significant growth anticipated over the coming years. According to projections, the market is expected to expand from $377.3 million in 2024 to $532.1 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.9% during the forecast period. This growth is driven by the increasing demand for high-performance adhesives and sealants across various industries, including construction, automotive, electronics, and healthcare. As these industries continue to evolve and innovate, the need for advanced silicone-based solutions that offer superior bonding, sealing, and insulating properties is expected to rise. The market's expansion is also supported by ongoing research and development efforts aimed at enhancing product performance and sustainability. Manufacturers are focusing on developing new formulations that meet the specific needs of different applications while also addressing environmental concerns. This includes the development of eco-friendly products that reduce the environmental impact of manufacturing and usage. The global reach of the market, combined with its diverse range of applications, underscores its importance in supporting infrastructure development, technological advancements, and the overall growth of various sectors. As the market continues to grow, it presents significant opportunities for manufacturers, suppliers, and end-users alike, driving innovation and progress across industries.

| Report Metric | Details |

| Report Name | Silicone Adhesives and Sealants Market |

| Accounted market size in 2024 | US$ 377.3 million |

| Forecasted market size in 2030 | US$ 532.1 million |

| CAGR | 5.9 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Henkel, 3M, Shin-Etsu Chemical, Wacker Chemie AG, Momentive, Bluestar, TEMPO Chemical, Hongda, ACC Silicones, Dow Corning |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |