What is Global Honey Wine Market?

The global honey wine market, also known as mead, is a fascinating segment of the alcoholic beverage industry that has been gaining traction worldwide. Honey wine is an ancient drink, often considered the oldest alcoholic beverage known to humanity, made by fermenting honey with water, and sometimes with various fruits, spices, grains, or hops. This market is characterized by its artisanal and craft nature, with many small producers creating unique and diverse flavors that appeal to a wide range of consumers. The growing interest in natural and organic products has also contributed to the rising popularity of honey wine, as it is often perceived as a more natural alternative to other alcoholic beverages. Additionally, the global honey wine market is driven by the increasing consumer demand for premium and exotic drinks, as well as the rising trend of home brewing. As more people become aware of honey wine and its rich history, the market is expected to continue its growth trajectory, attracting both traditional wine enthusiasts and new consumers looking for something different. The market's expansion is further supported by the increasing availability of honey wine in various retail channels, including online platforms, which makes it more accessible to a broader audience.

Herbs Type, Spices Type, Fruits Type in the Global Honey Wine Market:

The global honey wine market is diverse, with various types of honey wine being produced based on the ingredients used, such as herbs, spices, and fruits. Each type offers a unique flavor profile and appeals to different consumer preferences. Herb-based honey wines are crafted by infusing the mead with various herbs, which can add complexity and depth to the flavor. Common herbs used in honey wine production include lavender, rosemary, and thyme, each imparting its distinct aroma and taste. These herb-infused honey wines are often sought after by consumers who appreciate the subtle and sophisticated flavors that herbs can bring to the beverage. On the other hand, spice-based honey wines are made by adding spices such as cinnamon, cloves, or ginger during the fermentation process. These spices can add warmth and richness to the honey wine, making it a popular choice for those who enjoy bold and robust flavors. Spice-infused honey wines are particularly popular during the colder months, as they can provide a comforting and warming experience. Fruit-based honey wines, also known as melomels, are created by fermenting honey with various fruits, such as berries, apples, or citrus. The addition of fruits can enhance the sweetness and complexity of the honey wine, resulting in a refreshing and fruity beverage that is perfect for summer sipping. Fruit-infused honey wines are often favored by consumers who enjoy the natural sweetness and vibrant flavors that fruits can offer. The diversity of honey wine types based on herbs, spices, and fruits allows producers to cater to a wide range of consumer tastes and preferences, contributing to the overall growth and expansion of the global honey wine market. As consumers continue to seek out unique and innovative flavors, the demand for herb, spice, and fruit-based honey wines is expected to rise, further driving the market's development.

Convenience Store, Supermarket and Hypermarket, Bars, Others in the Global Honey Wine Market:

The global honey wine market finds its usage across various retail and hospitality sectors, including convenience stores, supermarkets and hypermarkets, bars, and other venues. Convenience stores play a crucial role in the distribution of honey wine, offering consumers easy access to this unique beverage. These stores often stock a limited selection of honey wines, catering to consumers looking for a quick and convenient purchase. The presence of honey wine in convenience stores helps increase its visibility and accessibility, attracting new consumers who may not have previously considered trying this ancient beverage. Supermarkets and hypermarkets, on the other hand, provide a more extensive selection of honey wines, allowing consumers to explore different brands and flavors. These large retail outlets often dedicate specific sections to alcoholic beverages, including honey wine, making it easier for consumers to discover and purchase this unique drink. The availability of honey wine in supermarkets and hypermarkets also helps to increase its popularity, as consumers are more likely to try new products when they are readily available in familiar shopping environments. Bars and other hospitality venues also play a significant role in the global honey wine market, offering consumers the opportunity to enjoy this beverage in a social setting. Many bars and restaurants have started to include honey wine on their drink menus, often pairing it with specific dishes to enhance the dining experience. The inclusion of honey wine in bars and restaurants helps to introduce this ancient beverage to a wider audience, as patrons are more likely to try new drinks when they are recommended by knowledgeable staff. Additionally, the global honey wine market is also expanding into other areas, such as online retail platforms, which provide consumers with the convenience of purchasing honey wine from the comfort of their homes. The increasing availability of honey wine across various retail and hospitality sectors is a testament to its growing popularity and demand, as more consumers seek out unique and exotic beverages to enjoy.

Global Honey Wine Market Outlook:

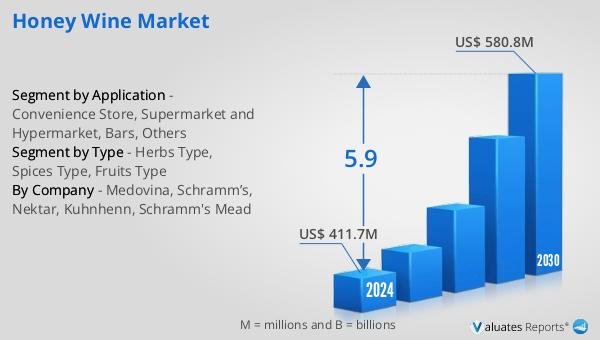

The outlook for the global honey wine market is promising, with projections indicating significant growth in the coming years. The market is expected to expand from a valuation of approximately $411.7 million in 2024 to an impressive $580.8 million by 2030. This growth trajectory represents a compound annual growth rate (CAGR) of 5.9% over the forecast period. This anticipated growth can be attributed to several factors, including the increasing consumer interest in natural and artisanal products, as well as the rising demand for premium and exotic beverages. As more consumers become aware of honey wine and its unique flavor profiles, the market is likely to attract a broader audience, including both traditional wine enthusiasts and those seeking new and innovative drink options. The expansion of the global honey wine market is also supported by the growing availability of honey wine in various retail channels, including online platforms, which make it more accessible to consumers worldwide. As the market continues to evolve, producers are likely to explore new flavors and ingredients, further driving consumer interest and demand. Overall, the global honey wine market is poised for significant growth, offering exciting opportunities for producers and consumers alike.

| Report Metric | Details |

| Report Name | Honey Wine Market |

| Accounted market size in 2024 | US$ 411.7 million |

| Forecasted market size in 2030 | US$ 580.8 million |

| CAGR | 5.9 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Medovina, Schramm’s, Nektar, Kuhnhenn, Schramm's Mead |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |