What is USB Data Connector - Global Market?

The USB Data Connector - Global Market is a rapidly evolving sector that plays a crucial role in the seamless transfer of data across various devices worldwide. USB, which stands for Universal Serial Bus, is a standard that defines cables, connectors, and protocols for connection, communication, and power supply between computers and electronic devices. The global market for USB data connectors is driven by the increasing demand for efficient data transfer solutions in consumer electronics, automotive, and industrial applications. As technology advances, the need for faster data transfer speeds and more reliable connections has led to the development of various types of USB connectors, including USB-A, USB-B, and USB-C. These connectors are designed to cater to different requirements, such as power delivery, data transfer speed, and compatibility with various devices. The market is characterized by continuous innovation and the introduction of new products to meet the ever-growing demands of consumers and industries. With the proliferation of smart devices and the Internet of Things (IoT), the USB data connector market is expected to witness significant growth in the coming years, driven by the need for efficient and reliable data transfer solutions.

USB-A, USB-B, USB-C in the USB Data Connector - Global Market:

USB-A, USB-B, and USB-C are the primary types of USB connectors that dominate the global market, each serving distinct purposes and applications. USB-A is the original USB connector, characterized by its rectangular shape and widespread use in computers and peripherals. It is commonly found in devices such as keyboards, mice, and flash drives. Despite its slower data transfer speeds compared to newer standards, USB-A remains popular due to its compatibility with a wide range of devices. USB-B, on the other hand, is typically used in larger devices like printers and external hard drives. It comes in various forms, including the standard USB-B, mini USB-B, and micro USB-B, each designed for specific applications. The mini and micro versions are often used in portable devices like cameras and smartphones. USB-C is the latest and most versatile USB connector, known for its reversible design and high-speed data transfer capabilities. It supports faster charging and data transfer rates, making it ideal for modern devices such as laptops, smartphones, and tablets. USB-C is also capable of delivering power, data, and video signals simultaneously, making it a preferred choice for manufacturers looking to streamline their product designs. The adoption of USB-C is rapidly increasing, driven by its ability to support a wide range of devices and its compatibility with emerging technologies like Thunderbolt 3. As the global market for USB data connectors continues to grow, the demand for USB-C is expected to rise, driven by its versatility and superior performance. The transition from older USB standards to USB-C is also facilitated by the increasing number of devices that support this connector, further boosting its adoption in various industries. Overall, the USB data connector market is characterized by a diverse range of products, each catering to specific needs and applications, with USB-C leading the charge in terms of innovation and adoption.

Automobile, Military, Consumer Electronics, Aerospace, Others in the USB Data Connector - Global Market:

The usage of USB Data Connectors in the global market spans across various sectors, including automobiles, military, consumer electronics, aerospace, and others, each leveraging the technology for its unique benefits. In the automobile industry, USB connectors are integral for infotainment systems, enabling seamless connectivity between smartphones and car audio systems. They facilitate charging and data transfer, allowing drivers and passengers to access music, navigation, and other applications on the go. The military sector utilizes USB connectors for secure data transfer and communication between devices in the field. The rugged design of certain USB connectors ensures durability and reliability in harsh environments, making them suitable for military applications. In consumer electronics, USB connectors are ubiquitous, found in devices ranging from smartphones and tablets to laptops and gaming consoles. They enable fast charging and data transfer, enhancing the user experience by providing quick and efficient connectivity. The aerospace industry also benefits from USB connectors, using them for data transfer and communication between various onboard systems. The reliability and speed of USB connectors are crucial in ensuring the smooth operation of aircraft systems. Other sectors, such as healthcare and industrial automation, also rely on USB connectors for efficient data transfer and device connectivity. In healthcare, USB connectors are used in medical devices for data collection and analysis, while in industrial automation, they facilitate communication between machines and control systems. Overall, the versatility and reliability of USB data connectors make them indispensable across various industries, driving their adoption and growth in the global market.

USB Data Connector - Global Market Outlook:

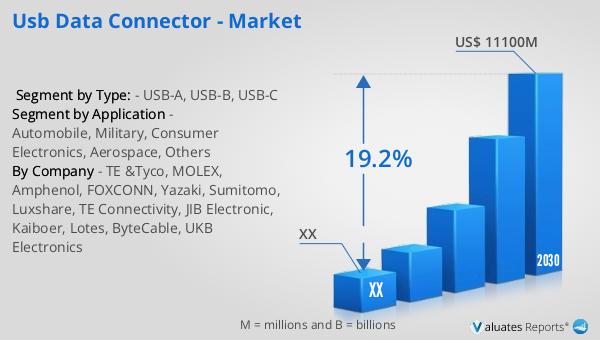

The global market for USB Data Connectors was valued at approximately $3.19 billion in 2023, with projections indicating a significant expansion to around $11.1 billion by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 19.2% from 2024 to 2030. This remarkable growth trajectory underscores the increasing demand for USB data connectors across various sectors, driven by technological advancements and the proliferation of smart devices. In North America, the market for USB Data Connectors is also poised for substantial growth, although specific figures for 2023 and 2030 are not provided. The region is expected to experience a robust CAGR during the forecast period, reflecting the widespread adoption of USB connectors in consumer electronics, automotive, and other industries. The increasing need for efficient data transfer solutions and the growing popularity of USB-C connectors are key factors contributing to the market's expansion. As industries continue to embrace digital transformation and connectivity, the demand for reliable and high-speed data transfer solutions like USB connectors is expected to rise, further fueling the market's growth. Overall, the USB Data Connector market is set to experience significant growth in the coming years, driven by the increasing demand for efficient and reliable data transfer solutions across various industries.

| Report Metric | Details |

| Report Name | USB Data Connector - Market |

| Forecasted market size in 2030 | US$ 11100 million |

| CAGR | 19.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | TE &Tyco, MOLEX, Amphenol, FOXCONN, Yazaki, Sumitomo, Luxshare, TE Connectivity, JIB Electronic, Kaiboer, Lotes, ByteCable, UKB Electronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |