What is Alumina Ceramic Package - Global Market?

Alumina Ceramic Package is a specialized component used in various electronic applications, known for its excellent thermal and electrical insulation properties. These packages are made from alumina, a type of ceramic material that is highly resistant to heat and corrosion, making it ideal for protecting sensitive electronic components. The global market for Alumina Ceramic Packages is driven by the increasing demand for reliable and durable electronic packaging solutions in industries such as automotive, aerospace, and consumer electronics. As technology advances, the need for components that can withstand high temperatures and harsh environments grows, further propelling the market. The versatility of alumina ceramics, combined with their cost-effectiveness and performance, makes them a preferred choice for manufacturers looking to enhance the longevity and efficiency of their products. With ongoing research and development, the market is expected to continue evolving, offering new opportunities for innovation and application in various sectors.

Black Ceramic, White Ceramic in the Alumina Ceramic Package - Global Market:

In the realm of Alumina Ceramic Packages, black and white ceramics play distinct roles, each offering unique benefits and applications. Black ceramic, often used for its aesthetic appeal, also provides excellent thermal management properties. It is particularly favored in applications where heat dissipation is crucial, such as in high-power LED lighting and advanced communication devices. The dark color of black ceramic helps in absorbing and radiating heat efficiently, making it a preferred choice in environments where temperature control is paramount. Additionally, black ceramic's robust nature ensures that it can withstand mechanical stress and harsh conditions, making it suitable for use in automotive electronics and aeronautics. On the other hand, white ceramic, known for its purity and high dielectric strength, is widely used in applications requiring superior electrical insulation. Its ability to maintain stability under high-frequency conditions makes it ideal for use in consumer electronics and communication devices. White ceramic's reflective properties also make it a popular choice in optical applications, where light management is essential. The global market for alumina ceramic packages sees a balanced demand for both black and white ceramics, as each type caters to specific industry needs. Manufacturers are continually exploring ways to enhance the properties of these ceramics, aiming to improve their performance and expand their application range. As industries evolve and new technologies emerge, the demand for both black and white alumina ceramics is expected to grow, driven by the need for reliable, efficient, and aesthetically pleasing electronic packaging solutions. The ongoing advancements in material science and engineering are likely to lead to the development of new ceramic formulations, further broadening the scope of applications for alumina ceramic packages. This dynamic market landscape presents numerous opportunities for innovation and growth, as companies strive to meet the ever-changing demands of modern technology.

Automotive Electronics, Communication Devices, Aeronautics and Astronautics, High Power LED, Consumer Electronics, Others in the Alumina Ceramic Package - Global Market:

Alumina Ceramic Packages find extensive usage across various sectors, each leveraging the material's unique properties to enhance performance and reliability. In automotive electronics, these packages are crucial for protecting sensitive components from the harsh conditions of the automotive environment. Their ability to withstand high temperatures and resist corrosion makes them ideal for use in engine control units, sensors, and other critical electronic systems. In communication devices, alumina ceramic packages provide excellent thermal management and electrical insulation, ensuring the efficient operation of components such as RF modules and power amplifiers. The aeronautics and astronautics industries also benefit from the durability and lightweight nature of alumina ceramics, using them in applications where weight reduction and reliability are paramount. High power LED applications utilize alumina ceramic packages for their superior heat dissipation capabilities, which help extend the lifespan of the LEDs and improve their performance. In consumer electronics, these packages are used to protect delicate components in devices such as smartphones, tablets, and laptops, where space is limited, and performance is critical. Beyond these specific applications, alumina ceramic packages are also employed in various other industries, including medical devices, industrial equipment, and renewable energy systems. Their versatility and adaptability make them a valuable component in any application requiring robust and reliable electronic packaging solutions. As technology continues to advance, the demand for alumina ceramic packages is expected to grow, driven by the need for components that can meet the increasing performance and reliability standards of modern electronic systems.

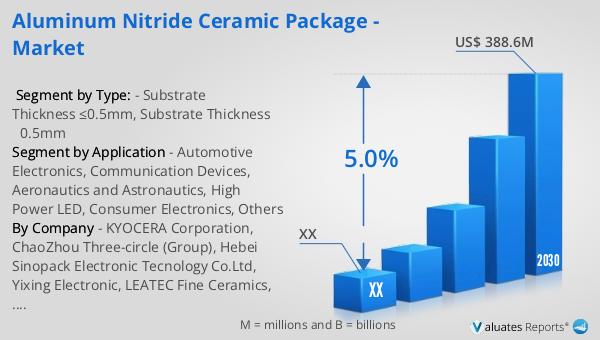

Alumina Ceramic Package - Global Market Outlook:

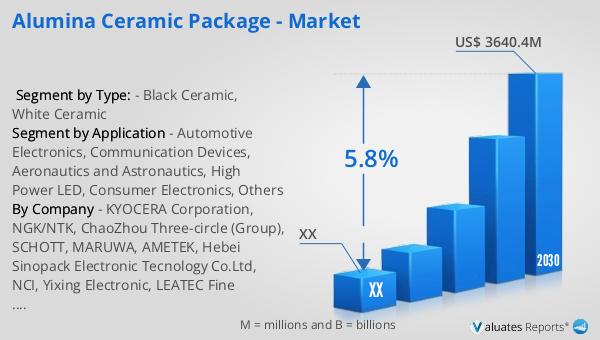

The global market for Alumina Ceramic Packages was valued at approximately $2,458.7 million in 2023. It is anticipated to grow to a revised size of $3,640.4 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for advanced electronic packaging solutions across various industries. In parallel, the semiconductor market, which was valued at $579 billion in 2022, is projected to reach $790 billion by 2029, growing at a CAGR of 6% during the forecast period. The growth in the semiconductor market is closely linked to the demand for alumina ceramic packages, as these components play a critical role in ensuring the performance and reliability of semiconductor devices. The synergy between these markets highlights the importance of alumina ceramic packages in the broader context of electronic component manufacturing and underscores the potential for continued growth and innovation in this field. As industries continue to evolve and new technologies emerge, the demand for high-performance, reliable, and cost-effective electronic packaging solutions is expected to drive the market for alumina ceramic packages, offering numerous opportunities for growth and development.

| Report Metric | Details |

| Report Name | Alumina Ceramic Package - Market |

| Forecasted market size in 2030 | US$ 3640.4 million |

| CAGR | 5.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | KYOCERA Corporation, NGK/NTK, ChaoZhou Three-circle (Group), SCHOTT, MARUWA, AMETEK, Hebei Sinopack Electronic Tecnology Co.Ltd, NCI, Yixing Electronic, LEATEC Fine Ceramics, Shengda Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |