What is Rocker DIP Switches - Global Market?

Rocker DIP switches are a type of electrical switch that is widely used in various electronic devices and systems. These switches are characterized by their rocker mechanism, which allows users to toggle between different positions, typically on and off. The global market for Rocker DIP switches is driven by their versatility and reliability in controlling electrical circuits. These switches are commonly found in consumer electronics, telecommunications, and industrial applications, where they serve as essential components for controlling power and signal flow. The market is influenced by the growing demand for electronic devices and the need for efficient and durable switching solutions. Manufacturers are continually innovating to improve the design and functionality of Rocker DIP switches, making them more user-friendly and adaptable to different applications. As technology advances, the market for these switches is expected to grow, driven by the increasing integration of electronic components in various industries. The global market for Rocker DIP switches is a dynamic and evolving sector, with opportunities for growth and development in the coming years.

Single Pole, Double Pole in the Rocker DIP Switches - Global Market:

Single Pole and Double Pole configurations are fundamental aspects of Rocker DIP switches, each serving distinct purposes in the global market. Single Pole Rocker DIP switches are designed to control a single circuit, making them ideal for applications where simplicity and cost-effectiveness are paramount. These switches are commonly used in consumer electronics, where they provide basic on/off functionality for devices like televisions, radios, and small appliances. The simplicity of Single Pole switches makes them easy to install and operate, contributing to their widespread adoption in various industries. On the other hand, Double Pole Rocker DIP switches offer more versatility by controlling two separate circuits simultaneously. This feature is particularly valuable in applications where multiple functions need to be managed with a single switch. For instance, in telecommunications equipment, Double Pole switches can be used to control both power and signal lines, ensuring efficient operation and reducing the need for additional components. The ability to handle multiple circuits makes Double Pole switches a preferred choice in complex systems where space and efficiency are critical considerations. The global market for Rocker DIP switches is influenced by the demand for both Single Pole and Double Pole configurations, with manufacturers focusing on enhancing the performance and reliability of these switches to meet the diverse needs of different industries. As technology continues to evolve, the market for Rocker DIP switches is expected to expand, driven by the increasing integration of electronic components in various applications. The versatility and adaptability of Single Pole and Double Pole Rocker DIP switches make them essential components in the global market, with opportunities for growth and innovation in the coming years.

Consumer Electronics & Appliances, Telecommunications, Others in the Rocker DIP Switches - Global Market:

Rocker DIP switches play a crucial role in various sectors, including consumer electronics and appliances, telecommunications, and other industries. In the consumer electronics and appliances sector, these switches are integral components in devices such as televisions, audio systems, and kitchen appliances. They provide users with a simple and reliable means of controlling power and functions, enhancing the overall user experience. The demand for Rocker DIP switches in this sector is driven by the continuous innovation and development of new electronic products, which require efficient and durable switching solutions. In the telecommunications industry, Rocker DIP switches are used in a wide range of equipment, including routers, modems, and communication devices. These switches are essential for managing power and signal flow, ensuring the smooth operation of telecommunications networks. The reliability and versatility of Rocker DIP switches make them a preferred choice for telecommunications companies looking to enhance the performance and efficiency of their equipment. In addition to consumer electronics and telecommunications, Rocker DIP switches are also used in various other industries, including automotive, industrial automation, and medical devices. In the automotive sector, these switches are used in dashboard controls and other electronic systems, providing drivers with easy access to essential functions. In industrial automation, Rocker DIP switches are used to control machinery and equipment, ensuring precise and reliable operation. In the medical field, these switches are used in diagnostic and monitoring equipment, where accuracy and reliability are critical. The global market for Rocker DIP switches is driven by the diverse applications and industries that rely on these components, with manufacturers continually innovating to meet the evolving needs of their customers. As technology advances and new applications emerge, the demand for Rocker DIP switches is expected to grow, creating opportunities for growth and development in the global market.

Rocker DIP Switches - Global Market Outlook:

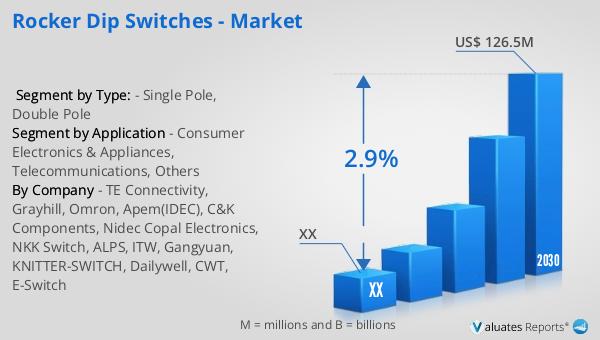

The global market for Rocker DIP switches was valued at approximately $103.5 million in 2023, with projections indicating a potential increase to around $126.5 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 2.9% during the forecast period from 2024 to 2030. This market outlook reflects the steady demand for Rocker DIP switches across various industries, driven by their versatility and reliability in controlling electrical circuits. The market's growth is supported by the increasing integration of electronic components in consumer electronics, telecommunications, and other sectors. Additionally, the construction machinery sector has shown significant growth, with sales in Europe increasing by 24% in 2021. In 2022, the construction machinery revenue in Europe was approximately $22 billion, while the U.S. market recorded sales of about $36 billion in construction machinery. This growth in the construction machinery sector highlights the broader trend of increasing demand for electronic components and switching solutions, which is expected to contribute to the expansion of the Rocker DIP switches market. As industries continue to innovate and develop new technologies, the global market for Rocker DIP switches is poised for growth, with opportunities for manufacturers to enhance their products and meet the evolving needs of their customers.

| Report Metric | Details |

| Report Name | Rocker DIP Switches - Market |

| Forecasted market size in 2030 | US$ 126.5 million |

| CAGR | 2.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | TE Connectivity, Grayhill, Omron, Apem(IDEC), C&K Components, Nidec Copal Electronics, NKK Switch, ALPS, ITW, Gangyuan, KNITTER-SWITCH, Dailywell, CWT, E-Switch |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |