What is Bucket Chain Excavator - Global Market?

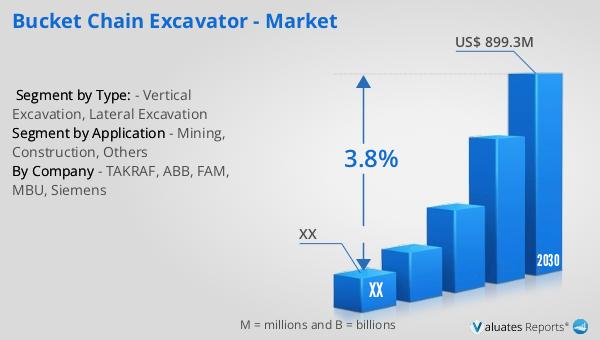

Bucket Chain Excavators (BCEs) are massive machines used primarily in large-scale excavation projects. These machines are designed to continuously dig and transport materials, making them highly efficient for tasks that require the removal of large volumes of earth or other materials. The global market for Bucket Chain Excavators is driven by the demand for efficient and cost-effective excavation solutions in industries such as mining, construction, and infrastructure development. These machines are particularly valued for their ability to operate in challenging environments, such as underwater or in areas with unstable ground conditions. The market is characterized by a mix of established manufacturers and emerging players, all striving to innovate and improve the efficiency and capabilities of their machines. As industries continue to expand and the need for large-scale excavation grows, the demand for Bucket Chain Excavators is expected to rise, making it a dynamic and evolving market. The global market for Bucket Chain Excavators was valued at approximately US$ 694 million in 2023, with projections indicating growth to US$ 899.3 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.8% during the forecast period from 2024 to 2030.

Vertical Excavation, Lateral Excavation in the Bucket Chain Excavator - Global Market:

Vertical excavation and lateral excavation are two primary methods employed in the operation of Bucket Chain Excavators (BCEs) within the global market. Vertical excavation involves the removal of materials in a downward direction, typically used in mining operations where deep pits or shafts are required. This method is advantageous for accessing mineral deposits located deep underground, allowing for efficient extraction without the need for extensive surface disruption. BCEs are particularly suited for vertical excavation due to their ability to continuously dig and transport materials, reducing the time and labor required for such operations. The design of BCEs allows them to maintain stability and efficiency even when operating at significant depths, making them a preferred choice for mining companies seeking to maximize productivity and minimize environmental impact. On the other hand, lateral excavation involves the removal of materials in a horizontal direction, often used in construction and infrastructure projects where large areas of land need to be cleared or leveled. This method is ideal for projects such as road construction, where a flat and stable surface is required. BCEs excel in lateral excavation due to their ability to cover large areas quickly and efficiently, reducing the time and cost associated with traditional excavation methods. The versatility of BCEs in both vertical and lateral excavation makes them a valuable asset in the global market, catering to a wide range of industries and applications. As the demand for efficient and cost-effective excavation solutions continues to grow, the market for BCEs is expected to expand, driven by advancements in technology and the increasing need for large-scale excavation projects. The ability of BCEs to adapt to different excavation methods and environments makes them a crucial tool for industries seeking to optimize their operations and achieve greater efficiency. With the global market for Bucket Chain Excavators projected to grow significantly in the coming years, the importance of understanding and utilizing both vertical and lateral excavation methods cannot be overstated. Companies that invest in BCEs and leverage their capabilities in both vertical and lateral excavation are likely to gain a competitive edge in the market, benefiting from increased productivity and reduced operational costs. As industries continue to evolve and the demand for large-scale excavation projects rises, the role of BCEs in vertical and lateral excavation will become increasingly important, shaping the future of the global market.

Mining, Construction, Others in the Bucket Chain Excavator - Global Market:

The usage of Bucket Chain Excavators (BCEs) in the global market spans several key areas, including mining, construction, and other industries. In the mining sector, BCEs are indispensable tools for the extraction of minerals and other valuable resources. Their ability to operate continuously and efficiently makes them ideal for large-scale mining operations, where the removal of vast quantities of earth is required. BCEs are particularly effective in open-pit mining, where they can be used to excavate deep pits and transport materials to the surface. Their robust design and ability to operate in challenging environments make them a preferred choice for mining companies seeking to maximize productivity and minimize environmental impact. In the construction industry, BCEs are used for a variety of tasks, including site preparation, road construction, and the excavation of foundations. Their ability to quickly and efficiently remove large volumes of earth makes them ideal for projects that require significant land clearing or leveling. BCEs are also used in the construction of infrastructure projects, such as dams and bridges, where their ability to operate in challenging conditions is highly valued. In addition to mining and construction, BCEs are used in other industries, such as dredging and land reclamation. In dredging operations, BCEs are used to remove sediment and debris from waterways, helping to maintain navigable channels and prevent flooding. Their ability to operate underwater and in challenging conditions makes them ideal for such tasks. In land reclamation projects, BCEs are used to excavate and transport materials, helping to create new land for development or agriculture. The versatility and efficiency of BCEs make them a valuable asset in the global market, catering to a wide range of industries and applications. As the demand for efficient and cost-effective excavation solutions continues to grow, the usage of BCEs in mining, construction, and other industries is expected to expand, driven by advancements in technology and the increasing need for large-scale excavation projects. The ability of BCEs to adapt to different environments and tasks makes them a crucial tool for industries seeking to optimize their operations and achieve greater efficiency. With the global market for Bucket Chain Excavators projected to grow significantly in the coming years, the importance of understanding and utilizing their capabilities in various industries cannot be overstated. Companies that invest in BCEs and leverage their capabilities in mining, construction, and other industries are likely to gain a competitive edge in the market, benefiting from increased productivity and reduced operational costs. As industries continue to evolve and the demand for large-scale excavation projects rises, the role of BCEs in mining, construction, and other industries will become increasingly important, shaping the future of the global market.

Bucket Chain Excavator - Global Market Outlook:

The global market for Bucket Chain Excavators was valued at approximately US$ 694 million in 2023, with projections indicating growth to US$ 899.3 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.8% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for efficient and cost-effective excavation solutions in industries such as mining, construction, and infrastructure development. The North American market for Bucket Chain Excavators is also expected to experience significant growth during this period, although specific figures for this region were not provided. The market is characterized by a mix of established manufacturers and emerging players, all striving to innovate and improve the efficiency and capabilities of their machines. As industries continue to expand and the need for large-scale excavation grows, the demand for Bucket Chain Excavators is expected to rise, making it a dynamic and evolving market. Companies that invest in BCEs and leverage their capabilities in various industries are likely to gain a competitive edge in the market, benefiting from increased productivity and reduced operational costs. As industries continue to evolve and the demand for large-scale excavation projects rises, the role of BCEs in the global market will become increasingly important, shaping the future of the industry.

| Report Metric | Details |

| Report Name | Bucket Chain Excavator - Market |

| Forecasted market size in 2030 | US$ 899.3 million |

| CAGR | 3.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | TAKRAF, ABB, FAM, MBU, Siemens |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |