What is Machine Condition Monitoring Software - Global Market?

Machine Condition Monitoring Software is a critical tool in the global market, designed to ensure the smooth operation of machinery by continuously assessing their condition. This software plays a pivotal role in predictive maintenance strategies, helping industries avoid unexpected equipment failures and costly downtime. By analyzing data from various sensors attached to machinery, the software can detect anomalies and predict potential failures before they occur. This proactive approach not only extends the lifespan of equipment but also enhances operational efficiency and safety. The global market for this software is expanding as industries increasingly recognize the value of maintaining optimal machine performance. With advancements in technology, these software solutions are becoming more sophisticated, offering real-time monitoring and advanced analytics capabilities. As industries strive for greater efficiency and reliability, the demand for machine condition monitoring software is expected to grow, driven by the need for cost-effective maintenance solutions and the integration of IoT and AI technologies.

Cloud Based, On-premise in the Machine Condition Monitoring Software - Global Market:

Machine Condition Monitoring Software can be deployed in two primary ways: cloud-based and on-premise solutions. Cloud-based solutions offer several advantages, particularly in terms of accessibility and scalability. These solutions allow users to access data and analytics from anywhere, provided they have an internet connection. This is particularly beneficial for companies with multiple locations or remote operations, as it enables centralized monitoring and management of machinery across different sites. Cloud-based solutions also offer the advantage of scalability, allowing businesses to easily adjust their monitoring capabilities as their needs change. Additionally, cloud solutions often come with lower upfront costs, as they do not require significant investment in hardware or infrastructure. On the other hand, on-premise solutions provide businesses with greater control over their data and systems. These solutions are installed directly on the company's servers, ensuring that sensitive data remains within the organization's control. This can be particularly important for industries with strict data security and compliance requirements. On-premise solutions also offer the advantage of customization, allowing businesses to tailor the software to their specific needs and integrate it with existing systems. However, they often come with higher upfront costs and require ongoing maintenance and updates. Despite these differences, both cloud-based and on-premise solutions are designed to provide comprehensive monitoring and analytics capabilities, helping businesses optimize their maintenance strategies and improve operational efficiency. As the global market for machine condition monitoring software continues to grow, businesses will need to carefully consider their specific needs and requirements when choosing between cloud-based and on-premise solutions. Factors such as budget, data security, and scalability will play a crucial role in determining the most suitable deployment option. Ultimately, the choice between cloud-based and on-premise solutions will depend on the unique needs and priorities of each organization.

Aerospace and Defense, Automotive and Transportation, Chemical and Petrochemical, Food & Beverage, Marine, Mining and Metal, Oil and Gas, Power Generation in the Machine Condition Monitoring Software - Global Market:

Machine Condition Monitoring Software is utilized across various industries, each with its unique requirements and challenges. In the Aerospace and Defense sector, this software is crucial for ensuring the reliability and safety of aircraft and defense equipment. By continuously monitoring the condition of critical components, the software helps prevent unexpected failures that could compromise safety and operational readiness. In the Automotive and Transportation industry, machine condition monitoring is used to maintain the performance and reliability of vehicles and transportation systems. This is particularly important for fleet management, where the software can help optimize maintenance schedules and reduce downtime. In the Chemical and Petrochemical industry, the software is used to monitor the condition of complex machinery and equipment, ensuring safe and efficient operations. This is critical in preventing costly shutdowns and ensuring compliance with safety regulations. In the Food & Beverage industry, machine condition monitoring helps maintain the efficiency and reliability of production equipment, ensuring consistent product quality and minimizing waste. In the Marine industry, the software is used to monitor the condition of ship engines and other critical systems, helping to prevent breakdowns and ensure safe and efficient operations. In the Mining and Metal industry, machine condition monitoring is used to maintain the performance and reliability of heavy machinery and equipment, reducing downtime and improving productivity. In the Oil and Gas industry, the software is used to monitor the condition of drilling and production equipment, ensuring safe and efficient operations in challenging environments. Finally, in the Power Generation industry, machine condition monitoring is used to maintain the reliability and efficiency of power generation equipment, ensuring a consistent and reliable supply of energy. Across all these industries, machine condition monitoring software plays a vital role in optimizing maintenance strategies, improving operational efficiency, and ensuring safety and reliability.

Machine Condition Monitoring Software - Global Market Outlook:

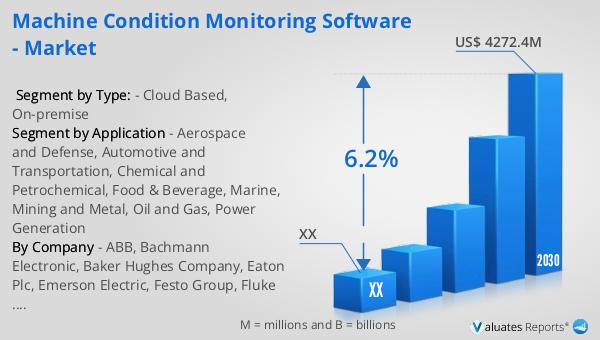

The global market for Machine Condition Monitoring Software was valued at approximately $2,812 million in 2023, and it is projected to grow to a revised size of $4,272.4 million by 2030. This growth represents a compound annual growth rate (CAGR) of 6.2% during the forecast period from 2024 to 2030. This upward trend highlights the increasing demand for advanced monitoring solutions across various industries. In North America, the market for this software was valued at a significant amount in 2023, with expectations of continued growth through 2030. The region's market dynamics are influenced by the widespread adoption of technology and the emphasis on predictive maintenance strategies. As industries in North America continue to prioritize operational efficiency and cost-effective maintenance solutions, the demand for machine condition monitoring software is expected to rise. This growth trajectory underscores the importance of these solutions in enhancing machinery performance, reducing downtime, and ensuring safety across diverse sectors. As the market evolves, businesses will need to stay abreast of technological advancements and industry trends to leverage the full potential of machine condition monitoring software.

| Report Metric | Details |

| Report Name | Machine Condition Monitoring Software - Market |

| Forecasted market size in 2030 | US$ 4272.4 million |

| CAGR | 6.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | ABB, Bachmann Electronic, Baker Hughes Company, Eaton Plc, Emerson Electric, Festo Group, Fluke Corporation, General Electric, Honeywell International, Ingeteam, Meggit, Parker Hannifin, PCE Instruments, Rockwell Automation, Schaeffler Technologies, Siemens AG |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |