What is Medical Grade UPS System - Global Market?

Medical Grade UPS Systems are specialized uninterruptible power supply units designed to meet the stringent requirements of healthcare environments. These systems ensure a continuous power supply to critical medical equipment, safeguarding against power interruptions that could compromise patient care or data integrity. In hospitals, clinics, and laboratories, where equipment like ventilators, imaging machines, and diagnostic tools are vital, a reliable power source is non-negotiable. Medical Grade UPS Systems are engineered to provide clean and stable power, filtering out surges and fluctuations that could damage sensitive equipment. They are built to comply with medical safety standards, ensuring they can operate in environments where electromagnetic interference must be minimized. The global market for these systems is expanding as healthcare facilities increasingly recognize the importance of reliable power solutions. With advancements in medical technology and the growing reliance on electronic health records, the demand for robust power backup systems is on the rise. This market growth is driven by the need to protect expensive medical equipment and ensure uninterrupted patient care, making Medical Grade UPS Systems an essential component in modern healthcare infrastructure.

Less Than 100 KVA, 100-200 KVA, More Than 200 KVA in the Medical Grade UPS System - Global Market:

Medical Grade UPS Systems are categorized based on their power capacity, which determines their suitability for different healthcare settings. Systems with less than 100 KVA are typically used in smaller facilities or for individual pieces of equipment. These units are compact and cost-effective, making them ideal for medical clinics or small laboratories where space and budget constraints are significant considerations. They provide sufficient power to support essential devices like patient monitors, small imaging machines, and laboratory equipment, ensuring that these critical tools remain operational during power outages. Systems in the 100-200 KVA range are more robust and are often deployed in medium-sized hospitals or larger clinics. They can support a broader range of equipment, including more advanced imaging systems and multiple diagnostic machines. These UPS systems offer a balance between capacity and cost, providing reliable power backup for facilities that require more extensive coverage but do not have the demands of a large hospital. For large hospitals and medical centers, systems with more than 200 KVA are necessary. These high-capacity units can support entire departments, including operating rooms, intensive care units, and emergency departments. They are designed to handle the significant power demands of large-scale medical equipment and ensure that critical care areas remain fully operational during power disruptions. The choice of UPS system capacity is crucial, as it directly impacts the facility's ability to maintain uninterrupted operations and protect patient safety. As healthcare facilities continue to expand and integrate more advanced technologies, the demand for higher-capacity UPS systems is expected to grow, driving innovation and development in this market segment.

Hospital, Medical Clinic, Research Laboratory, Medical Data Center, Others in the Medical Grade UPS System - Global Market:

Medical Grade UPS Systems play a vital role in various healthcare settings, ensuring that critical operations can continue without interruption. In hospitals, these systems are essential for maintaining power to life-saving equipment such as ventilators, dialysis machines, and surgical tools. During surgeries or in intensive care units, any power disruption could have dire consequences, making reliable UPS systems indispensable. In medical clinics, UPS systems support diagnostic equipment and patient monitoring devices, ensuring that tests and treatments can proceed without delay. Clinics often operate with limited resources, so a dependable power backup system is crucial to maintaining service quality and patient trust. Research laboratories rely on Medical Grade UPS Systems to protect sensitive experiments and data. Power interruptions can lead to the loss of valuable research, making UPS systems a critical component in maintaining the integrity of scientific investigations. In medical data centers, where electronic health records and other critical data are stored, UPS systems ensure that information remains accessible and secure. Data centers require a stable power supply to prevent data loss and maintain the confidentiality and availability of patient information. Other healthcare facilities, such as nursing homes and rehabilitation centers, also benefit from Medical Grade UPS Systems. These systems ensure that essential services, like heating, ventilation, and communication systems, remain operational, providing a safe and comfortable environment for patients and staff. Across all these settings, the use of Medical Grade UPS Systems underscores the importance of reliable power solutions in maintaining the quality and continuity of healthcare services.

Medical Grade UPS System - Global Market Outlook:

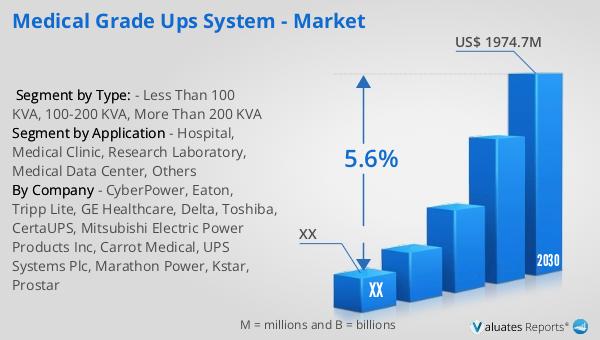

The global market for Medical Grade UPS Systems was valued at approximately $1,375 million in 2023. It is projected to grow to a revised size of $1,974.7 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.6% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for reliable power solutions in healthcare settings worldwide. As medical facilities continue to adopt advanced technologies and electronic health records, the need for robust power backup systems becomes more critical. The market for medical devices, which was estimated at $603 billion in 2023, is also expected to grow at a CAGR of 5% over the next six years. This growth in the medical device market further underscores the importance of Medical Grade UPS Systems, as they provide the necessary power stability to support these devices. The expansion of both markets highlights the ongoing investment in healthcare infrastructure and the prioritization of patient safety and data integrity. As healthcare providers strive to improve service quality and operational efficiency, the demand for Medical Grade UPS Systems is likely to continue its upward trajectory, making it a key area of focus for industry stakeholders.

| Report Metric | Details |

| Report Name | Medical Grade UPS System - Market |

| Forecasted market size in 2030 | US$ 1974.7 million |

| CAGR | 5.6% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | CyberPower, Eaton, Tripp Lite, GE Healthcare, Delta, Toshiba, CertaUPS, Mitsubishi Electric Power Products Inc, Carrot Medical, UPS Systems Plc, Marathon Power, Kstar, Prostar |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |