What is LiDAR Point Cloud Processing Software - Global Market?

LiDAR Point Cloud Processing Software is a specialized tool used to interpret and manage data collected by LiDAR (Light Detection and Ranging) technology. This software is crucial in transforming raw LiDAR data into meaningful information, which can be used for various applications such as mapping, 3D modeling, and analysis. The global market for this software is expanding rapidly due to the increasing adoption of LiDAR technology across different industries. LiDAR systems generate vast amounts of data in the form of point clouds, which are essentially a collection of data points in space representing the external surface of objects. Processing this data requires sophisticated software that can handle large datasets, perform complex calculations, and produce accurate results. The software is designed to filter, segment, and classify point clouds, making it easier for users to extract valuable insights. As industries like construction, automotive, and environmental monitoring continue to leverage LiDAR technology, the demand for efficient point cloud processing software is expected to grow. This growth is driven by the need for precise data analysis and the ability to create detailed 3D models, which are essential for planning, decision-making, and innovation in various sectors.

Cloud-based, On-premise in the LiDAR Point Cloud Processing Software - Global Market:

LiDAR Point Cloud Processing Software can be deployed in two main ways: cloud-based and on-premise solutions. Cloud-based LiDAR processing software offers several advantages, particularly in terms of scalability and accessibility. Users can access the software from anywhere with an internet connection, making it ideal for teams that are distributed across different locations. This model also allows for easy collaboration, as multiple users can work on the same project simultaneously. Additionally, cloud-based solutions often come with automatic updates and maintenance, reducing the burden on IT departments. They are also scalable, meaning that as the volume of data increases, users can easily upgrade their storage and processing capabilities without significant upfront costs. On the other hand, on-premise LiDAR processing software is installed directly on a user's local servers or computers. This model provides greater control over data security and privacy, as all data is stored and processed within the organization's own infrastructure. It is often preferred by industries that handle sensitive information or operate in areas with limited internet connectivity. On-premise solutions can be customized to meet specific organizational needs, offering flexibility in terms of software configuration and integration with existing systems. However, they require a significant initial investment in hardware and ongoing maintenance, which can be a drawback for some organizations. Despite these differences, both cloud-based and on-premise LiDAR processing software aim to provide users with the tools they need to efficiently process and analyze LiDAR data. The choice between the two often depends on factors such as budget, data security requirements, and the specific needs of the organization. As the global market for LiDAR Point Cloud Processing Software continues to grow, both deployment models are expected to evolve, offering more advanced features and capabilities to meet the diverse needs of users across various industries.

Achitechive, Land Survey, Forestry, Mines and Quarries, Others in the LiDAR Point Cloud Processing Software - Global Market:

LiDAR Point Cloud Processing Software is utilized in a variety of fields, each benefiting from its ability to provide detailed and accurate spatial data. In architecture, the software is used to create precise 3D models of buildings and structures. This allows architects and engineers to visualize projects in detail, identify potential issues, and make informed decisions during the design and construction phases. The software's ability to handle large datasets and produce high-resolution models makes it an invaluable tool in modern architectural practices. In land surveying, LiDAR Point Cloud Processing Software is used to generate accurate topographical maps and models. Surveyors can quickly and efficiently collect data over large areas, reducing the time and cost associated with traditional surveying methods. The software's ability to process and analyze this data ensures that surveyors have access to reliable information for planning and development purposes. In forestry, the software is used to monitor and manage forest resources. By analyzing LiDAR data, foresters can assess tree height, density, and health, enabling them to make informed decisions about forest management and conservation. The software's ability to provide detailed insights into forest structure and composition is crucial for sustainable forestry practices. In mines and quarries, LiDAR Point Cloud Processing Software is used to create detailed 3D models of mining sites. This allows operators to monitor changes in the landscape, assess the volume of extracted materials, and ensure the safety and efficiency of mining operations. The software's ability to provide accurate and up-to-date information is essential for effective resource management and planning. Beyond these specific applications, LiDAR Point Cloud Processing Software is also used in other areas such as environmental monitoring, urban planning, and disaster management. Its ability to provide detailed and accurate spatial data makes it a valuable tool for a wide range of industries and applications.

LiDAR Point Cloud Processing Software - Global Market Outlook:

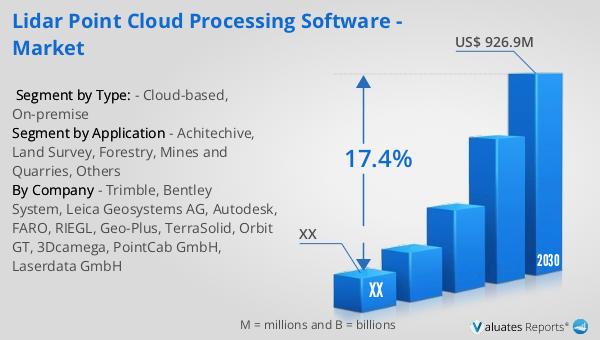

The global market for LiDAR Point Cloud Processing Software was valued at approximately $317 million in 2023. It is projected to grow significantly, reaching an estimated $926.9 million by 2030. This represents a compound annual growth rate (CAGR) of 17.4% during the forecast period from 2024 to 2030. This growth is driven by the increasing adoption of LiDAR technology across various industries, as well as the need for efficient data processing and analysis tools. In North America, the market for LiDAR Point Cloud Processing Software is also expected to experience substantial growth. Although specific figures for the North American market were not provided, it is anticipated that the region will see a similar upward trend in demand for this software. The growth in North America can be attributed to the presence of key industry players, technological advancements, and the increasing use of LiDAR technology in sectors such as construction, automotive, and environmental monitoring. As the global and regional markets continue to expand, LiDAR Point Cloud Processing Software is expected to play a crucial role in enabling organizations to harness the full potential of LiDAR data, driving innovation and efficiency across various industries.

| Report Metric | Details |

| Report Name | LiDAR Point Cloud Processing Software - Market |

| Forecasted market size in 2030 | US$ 926.9 million |

| CAGR | 17.4% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Trimble, Bentley System, Leica Geosystems AG, Autodesk, FARO, RIEGL, Geo-Plus, TerraSolid, Orbit GT, 3Dcamega, PointCab GmbH, Laserdata GmbH |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |