What is Virtual Healthcare - Global Market?

Virtual healthcare is a rapidly evolving sector within the global market, offering a range of services that allow patients to receive medical care without the need for physical visits to healthcare facilities. This innovative approach leverages technology to provide healthcare services remotely, making it more accessible and convenient for patients worldwide. Virtual healthcare encompasses a variety of services, including video consultations, audio consultations, and the use of kiosks, which are designed to cater to different healthcare needs. The global market for virtual healthcare is driven by the increasing demand for efficient and cost-effective healthcare solutions, especially in regions with limited access to traditional healthcare facilities. The integration of advanced technologies such as artificial intelligence, machine learning, and the Internet of Things (IoT) has further enhanced the capabilities of virtual healthcare, enabling more accurate diagnoses and personalized treatment plans. As the world continues to embrace digital transformation, the virtual healthcare market is expected to grow significantly, offering new opportunities for healthcare providers and patients alike. This growth is fueled by the need for continuous healthcare delivery, especially in the wake of global challenges such as pandemics, which have highlighted the importance of remote healthcare solutions.

Video Consulation, Audio Consulation, KIOSKS in the Virtual Healthcare - Global Market:

Video consultations are a cornerstone of virtual healthcare, providing patients with the ability to connect with healthcare professionals through video conferencing platforms. This method allows for real-time interaction, enabling doctors to assess patients visually and discuss symptoms, treatment plans, and follow-up care. Video consultations are particularly beneficial for patients with mobility issues or those living in remote areas, as they eliminate the need for travel and reduce the time spent in waiting rooms. Additionally, video consultations can be used for a wide range of medical services, from routine check-ups to specialist consultations, making healthcare more accessible and efficient. Audio consultations, on the other hand, offer a more straightforward approach to virtual healthcare, allowing patients to speak with healthcare providers over the phone. This method is ideal for situations where visual assessment is not necessary, such as discussing test results, medication management, or providing general health advice. Audio consultations are also beneficial for patients who may not have access to video conferencing technology or prefer a more traditional approach to communication. Kiosks represent another innovative aspect of virtual healthcare, providing patients with access to healthcare services in public or semi-public locations such as pharmacies, shopping centers, or workplaces. These kiosks are equipped with various medical devices and technology that allow patients to conduct self-assessments, measure vital signs, and connect with healthcare professionals remotely. Kiosks are particularly useful for providing healthcare services in underserved areas, where access to traditional healthcare facilities may be limited. They also offer a convenient option for patients who require quick consultations or follow-up care without the need for a full clinic visit. The integration of video consultations, audio consultations, and kiosks within the virtual healthcare market highlights the versatility and adaptability of this sector, catering to diverse patient needs and preferences. As technology continues to advance, these virtual healthcare solutions are expected to become even more sophisticated, offering enhanced capabilities and improved patient outcomes. The global market for virtual healthcare is poised for significant growth, driven by the increasing demand for accessible, efficient, and cost-effective healthcare solutions.

Everyday Care, Urgent Care, Mental Health, Others in the Virtual Healthcare - Global Market:

The usage of virtual healthcare in everyday care has transformed the way patients manage their health, offering a convenient and efficient alternative to traditional healthcare visits. For routine check-ups and ongoing health management, virtual healthcare provides patients with the flexibility to schedule appointments at their convenience, reducing the need for time-consuming travel and waiting room delays. This approach is particularly beneficial for individuals with chronic conditions who require regular monitoring and consultations, as it allows them to maintain consistent communication with their healthcare providers without the hassle of frequent in-person visits. In urgent care situations, virtual healthcare offers a rapid response solution, enabling patients to connect with healthcare professionals quickly and receive timely advice and treatment. This is especially important in cases where immediate medical attention is required, but a physical visit to a healthcare facility is not feasible. Virtual urgent care services can help triage patients, provide initial assessments, and determine the appropriate course of action, ensuring that patients receive the care they need promptly. In the realm of mental health, virtual healthcare has opened up new avenues for support and treatment, making mental health services more accessible to a broader population. Through video and audio consultations, patients can connect with mental health professionals from the comfort of their own homes, reducing the stigma and barriers associated with seeking mental health care. This approach allows for more frequent and flexible therapy sessions, enabling patients to receive consistent support and guidance. Additionally, virtual healthcare can facilitate group therapy sessions and support groups, providing patients with a sense of community and shared experience. Beyond everyday care, urgent care, and mental health, virtual healthcare is also being utilized in various other areas, such as rehabilitation, preventive care, and disease management. For rehabilitation, virtual healthcare offers patients the ability to participate in physical therapy sessions remotely, guided by healthcare professionals through video consultations. This approach ensures that patients can continue their rehabilitation programs without interruption, even if they are unable to attend in-person sessions. In preventive care, virtual healthcare enables patients to access educational resources, wellness programs, and health screenings, empowering them to take a proactive approach to their health. Disease management is another area where virtual healthcare is making a significant impact, providing patients with tools and resources to monitor and manage their conditions effectively. Through remote monitoring devices and virtual consultations, patients can track their health metrics, receive personalized feedback, and adjust their treatment plans as needed. The versatility and adaptability of virtual healthcare make it a valuable tool in addressing a wide range of healthcare needs, offering patients greater control over their health and well-being.

Virtual Healthcare - Global Market Outlook:

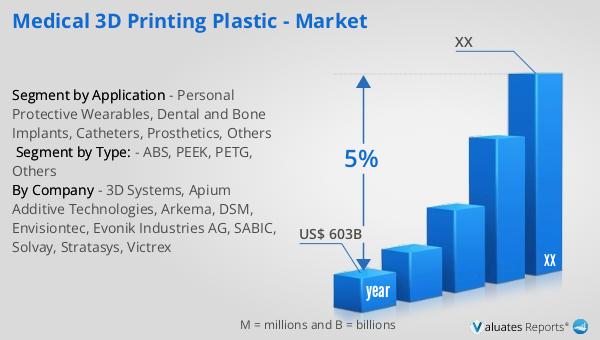

Our research indicates that the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth trajectory underscores the increasing demand for medical devices across various healthcare sectors, driven by technological advancements and the rising prevalence of chronic diseases. The expansion of the medical device market is also fueled by the growing adoption of digital health solutions, including telemedicine and remote monitoring, which are integral components of the broader virtual healthcare landscape. As healthcare systems worldwide continue to evolve, the integration of medical devices into virtual healthcare platforms is expected to enhance patient care and improve health outcomes. The projected growth of the medical device market reflects the ongoing shift towards more personalized and efficient healthcare delivery, as well as the increasing emphasis on preventive care and early intervention. This trend is likely to drive innovation and investment in the development of new medical devices and technologies, further expanding the capabilities of virtual healthcare solutions. As the global market for medical devices continues to grow, it will play a crucial role in shaping the future of healthcare, providing patients with access to cutting-edge technologies and improving the overall quality of care.

| Report Metric | Details |

| Report Name | Virtual Healthcare - Market |

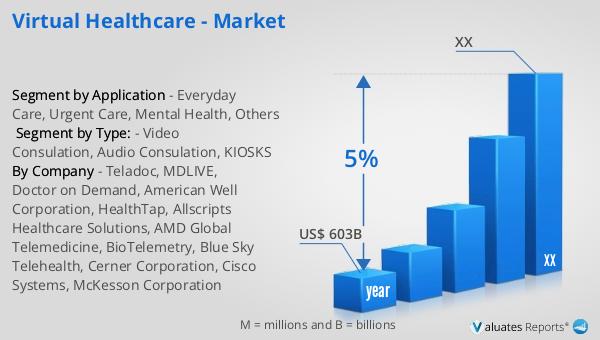

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Teladoc, MDLIVE, Doctor on Demand, American Well Corporation, HealthTap, Allscripts Healthcare Solutions, AMD Global Telemedicine, BioTelemetry, Blue Sky Telehealth, Cerner Corporation, Cisco Systems, McKesson Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |