What is Blood Glucose and Ketone Meters - Global Market?

Blood glucose and ketone meters are essential tools in the global healthcare market, designed to help individuals monitor their blood sugar and ketone levels. These devices are crucial for people with diabetes, as they provide real-time data that can help manage the condition effectively. Blood glucose meters measure the concentration of glucose in the blood, while ketone meters assess the level of ketones, which are chemicals produced when the body burns fat for energy. The global market for these devices is expanding due to the increasing prevalence of diabetes and the growing awareness of the importance of regular monitoring. Technological advancements have also played a significant role in the market's growth, with newer models offering more accurate readings, user-friendly interfaces, and connectivity features that allow data to be shared with healthcare providers. As the demand for these devices continues to rise, manufacturers are focusing on innovation and affordability to cater to a broader audience. The global market for blood glucose and ketone meters is poised for significant growth, driven by the need for better diabetes management solutions and the increasing adoption of health monitoring technologies.

Standard Blood Glucose and Ketone Meters, Continuous Monitoring Blood Glucose and Ketone Meters in the Blood Glucose and Ketone Meters - Global Market:

Standard blood glucose and ketone meters are the traditional devices used by individuals to monitor their blood sugar and ketone levels. These meters typically require a small blood sample, usually obtained from a finger prick, to provide a reading. The process involves inserting a test strip into the meter, applying the blood sample to the strip, and waiting for the device to display the results. These meters are widely used due to their affordability and ease of use, making them accessible to a large number of people. However, they require manual testing and do not provide continuous monitoring, which can be a limitation for some users. On the other hand, continuous monitoring blood glucose and ketone meters offer a more advanced solution. These devices use sensors that are placed on the skin to continuously track glucose and ketone levels throughout the day. The data is transmitted to a receiver or smartphone app, allowing users to monitor their levels in real-time. This continuous feedback can be particularly beneficial for individuals who need to make frequent adjustments to their diet or medication. Continuous monitoring devices are gaining popularity due to their convenience and the comprehensive data they provide, which can lead to better diabetes management. However, they tend to be more expensive than standard meters, which can be a barrier for some users. Despite this, the demand for continuous monitoring devices is increasing as more people recognize the benefits of having real-time data at their fingertips. The global market for blood glucose and ketone meters is evolving, with both standard and continuous monitoring devices playing a crucial role in helping individuals manage their health effectively. As technology continues to advance, we can expect to see further innovations in this market, making these devices even more accessible and user-friendly.

Residential, Medical in the Blood Glucose and Ketone Meters - Global Market:

Blood glucose and ketone meters are used in various settings, including residential and medical environments, to help individuals manage their health effectively. In residential settings, these devices are primarily used by individuals with diabetes or those following a ketogenic diet. For people with diabetes, regular monitoring of blood glucose levels is essential to prevent complications and maintain overall health. Blood glucose meters allow individuals to check their levels at home, providing them with the information they need to make informed decisions about their diet, exercise, and medication. Similarly, ketone meters are used by individuals on a ketogenic diet to monitor their ketone levels and ensure they are in a state of ketosis, which is necessary for the diet to be effective. The convenience of having these devices at home allows users to take control of their health and make necessary adjustments to their lifestyle. In medical settings, blood glucose and ketone meters are used by healthcare professionals to monitor patients' levels and make informed decisions about their treatment plans. These devices are particularly important in hospitals and clinics, where accurate and timely data is crucial for patient care. In addition to monitoring patients with diabetes, ketone meters are also used in medical settings to assess patients with conditions such as diabetic ketoacidosis, a serious complication of diabetes that requires immediate attention. The use of these devices in medical settings ensures that healthcare professionals have the information they need to provide the best possible care to their patients. As the global market for blood glucose and ketone meters continues to grow, we can expect to see further advancements in the technology and increased adoption in both residential and medical settings.

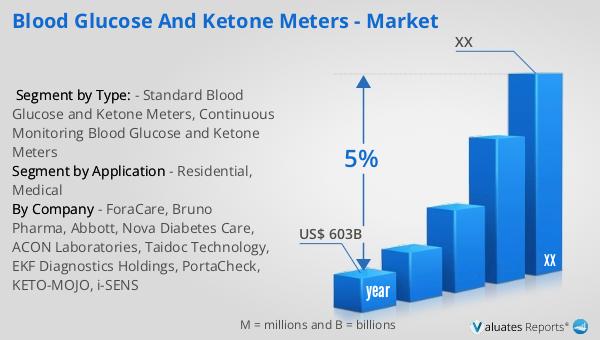

Blood Glucose and Ketone Meters - Global Market Outlook:

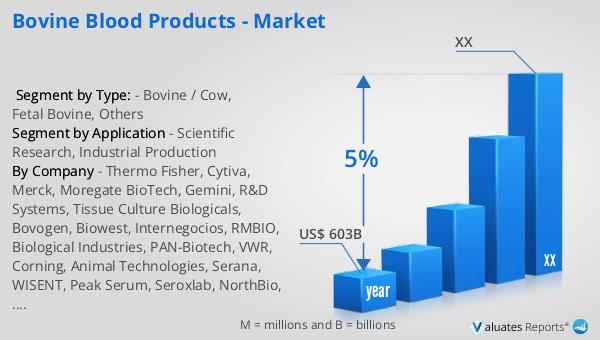

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases, technological advancements, and the rising demand for healthcare services worldwide. As the population continues to age and the incidence of conditions such as diabetes and cardiovascular diseases rises, the need for effective medical devices becomes more critical. Innovations in technology have also played a significant role in the market's expansion, with new devices offering improved accuracy, ease of use, and connectivity features that enhance patient care. Additionally, the growing awareness of the importance of regular health monitoring and the increasing adoption of wearable devices are contributing to the market's growth. As the global market for medical devices continues to evolve, manufacturers are focusing on developing innovative solutions that cater to the diverse needs of patients and healthcare providers. This focus on innovation and patient-centric solutions is expected to drive the market's growth in the coming years, making medical devices an essential component of modern healthcare.

| Report Metric | Details |

| Report Name | Blood Glucose and Ketone Meters - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | ForaCare, Bruno Pharma, Abbott, Nova Diabetes Care, ACON Laboratories, Taidoc Technology, EKF Diagnostics Holdings, PortaCheck, KETO-MOJO, i-SENS |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |