What is Straight Dental Implant Analog - Global Market?

Straight dental implant analogs are essential components in the field of dental prosthetics, serving as replicas of dental implants. These analogs are used primarily in the laboratory setting to create accurate dental prostheses. They mimic the size and shape of actual dental implants, allowing dental technicians to fabricate crowns, bridges, and dentures that fit perfectly onto the implants placed in a patient's mouth. The global market for straight dental implant analogs is expanding due to the increasing demand for dental implants, driven by factors such as the aging population, rising awareness of oral health, and advancements in dental technology. As more people seek dental implants for tooth replacement, the need for precise and reliable analogs grows. This market is characterized by a variety of materials used in the production of these analogs, including stainless steel, titanium, and plastic, each offering unique benefits in terms of durability, cost, and ease of use. The global reach of this market is evident as dental professionals worldwide rely on these analogs to ensure the success of implant procedures and the satisfaction of their patients.

Stainless Steel, Titanium, Plastic, Other in the Straight Dental Implant Analog - Global Market:

The materials used in the production of straight dental implant analogs play a crucial role in their functionality and application. Stainless steel is a popular choice due to its strength and resistance to corrosion. It provides a durable option for dental laboratories, ensuring that the analogs can withstand the rigors of the fabrication process. Stainless steel analogs are often preferred for their cost-effectiveness and longevity, making them a staple in many dental labs. Titanium, on the other hand, is renowned for its biocompatibility and lightweight nature. Although more expensive than stainless steel, titanium analogs are favored for their ability to closely mimic the properties of actual dental implants, providing a more realistic model for prosthetic creation. This material is particularly beneficial in cases where precision and accuracy are paramount. Plastic analogs offer a different set of advantages, primarily in terms of cost and ease of manipulation. They are often used in situations where budget constraints are a concern or when a temporary solution is needed. Plastic analogs are lightweight and easy to work with, making them a versatile option for dental technicians. However, they may not offer the same level of durability as metal counterparts. Other materials, such as zirconia or hybrid composites, are also emerging in the market, offering unique properties that cater to specific needs in dental prosthetics. These materials provide additional options for dental professionals, allowing for customization based on the specific requirements of each case. The choice of material for straight dental implant analogs depends on various factors, including the specific application, budget, and desired outcome. As the global market for these analogs continues to grow, the diversity of materials available ensures that dental professionals have the tools they need to deliver high-quality prosthetic solutions to their patients.

Hospital, Clinic, Other in the Straight Dental Implant Analog - Global Market:

Straight dental implant analogs are utilized in various healthcare settings, including hospitals, clinics, and other specialized dental facilities. In hospitals, these analogs are often used in conjunction with complex dental surgeries, where precise planning and execution are critical. The use of analogs allows surgeons to simulate the placement of dental implants, ensuring that the final prosthetic fits perfectly and functions as intended. This is particularly important in cases involving multiple implants or when dealing with challenging anatomical structures. In clinics, straight dental implant analogs are a staple in the day-to-day operations of dental professionals. They are used to create accurate impressions and models, which are essential for the fabrication of crowns, bridges, and other dental prostheses. The use of analogs in clinics helps streamline the process of dental restoration, reducing the time and cost associated with traditional methods. This efficiency is crucial in a clinical setting, where patient turnover and satisfaction are key priorities. Other specialized dental facilities, such as dental laboratories, also rely heavily on straight dental implant analogs. In these settings, analogs are used to create detailed and precise models that serve as the foundation for high-quality dental prosthetics. The ability to replicate the exact dimensions and characteristics of dental implants ensures that the final product meets the highest standards of accuracy and functionality. The global market for straight dental implant analogs is driven by the increasing demand for dental implants and the need for reliable and efficient tools in the dental industry. As more healthcare providers recognize the benefits of using analogs in their practice, the adoption of these tools continues to rise, contributing to the growth of the market.

Straight Dental Implant Analog - Global Market Outlook:

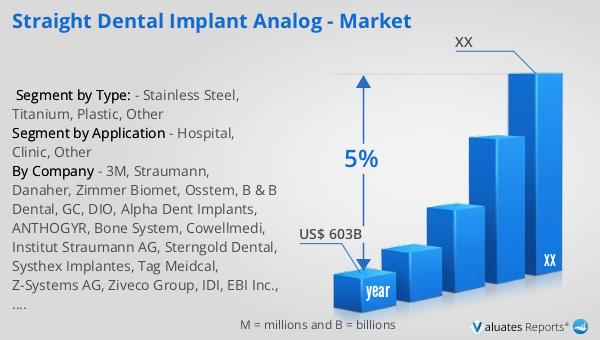

Our research indicates that the global market for medical devices, including straight dental implant analogs, is valued at approximately US$ 603 billion in 2023. This market is projected to experience a compound annual growth rate (CAGR) of 5% over the next six years. This growth is fueled by several factors, including advancements in medical technology, increasing healthcare expenditure, and the rising prevalence of chronic diseases that necessitate medical interventions. The dental sector, in particular, is witnessing significant growth due to the increasing demand for dental implants and related products. As the population ages and awareness of oral health rises, more individuals are seeking dental solutions that improve their quality of life. Straight dental implant analogs play a vital role in this landscape, providing the necessary tools for dental professionals to deliver effective and reliable implant procedures. The global reach of the medical device market ensures that innovations and advancements in dental technology are accessible to healthcare providers worldwide, further driving the adoption of straight dental implant analogs. As the market continues to expand, the focus remains on delivering high-quality, cost-effective solutions that meet the evolving needs of patients and healthcare providers alike.

| Report Metric | Details |

| Report Name | Straight Dental Implant Analog - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | 3M, Straumann, Danaher, Zimmer Biomet, Osstem, B & B Dental, GC, DIO, Alpha Dent Implants, ANTHOGYR, Bone System, Cowellmedi, Institut Straumann AG, Sterngold Dental, Systhex Implantes, Tag Meidcal, Z-Systems AG, Ziveco Group, IDI, EBI Inc., Bio 3 implants GmbH |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |