What is CHNSO Analyzers - Global Market?

CHNSO analyzers are specialized instruments used to determine the elemental composition of a sample by measuring the amounts of carbon (C), hydrogen (H), nitrogen (N), sulfur (S), and oxygen (O). These analyzers play a crucial role in various industries by providing precise and reliable data on the elemental makeup of different materials. The global market for CHNSO analyzers is driven by the increasing demand for accurate and efficient analytical tools across sectors such as energy, chemicals, environment, agriculture, and geology. As industries continue to seek ways to optimize processes and ensure compliance with environmental regulations, the need for advanced analytical equipment like CHNSO analyzers is expected to grow. These instruments are essential for quality control, research and development, and regulatory compliance, making them indispensable in modern industrial applications. The market is characterized by technological advancements that enhance the accuracy, speed, and user-friendliness of these analyzers, further boosting their adoption across various sectors. As a result, the CHNSO analyzers market is poised for steady growth, driven by the ongoing demand for precise elemental analysis in diverse applications.

GC Chromatography, Frontal Chromatography, Adsorption-Desorption in the CHNSO Analyzers - Global Market:

Gas Chromatography (GC) is a widely used analytical technique in the CHNSO analyzers market, offering a method to separate and analyze compounds that can be vaporized without decomposition. In the context of CHNSO analyzers, GC is employed to identify and quantify the elemental composition of complex mixtures. This technique is particularly valuable in the chemical industry, where it aids in the analysis of hydrocarbons and other volatile compounds. Frontal Chromatography, on the other hand, is a less common but effective method used in CHNSO analysis. It involves the continuous introduction of a sample into a column, allowing for the separation of components based on their adsorption properties. This technique is beneficial for analyzing mixtures with components that have similar boiling points or are difficult to separate using traditional methods. Adsorption-desorption techniques are also integral to CHNSO analyzers, providing a means to study the interaction between gases and solid surfaces. This method is crucial in environmental studies, where it helps in understanding the behavior of pollutants and their impact on the environment. By analyzing the adsorption and desorption patterns, researchers can gain insights into the distribution and fate of contaminants in various ecosystems. The integration of these techniques in CHNSO analyzers enhances their versatility and applicability across different industries. In the energy sector, for instance, these analyzers are used to assess the quality of fuels and optimize combustion processes. By providing detailed information on the elemental composition of fuels, CHNSO analyzers help in improving energy efficiency and reducing emissions. In the chemical industry, these analyzers are essential for quality control and product development, ensuring that products meet the required specifications and standards. Environmental applications of CHNSO analyzers include monitoring air and water quality, assessing soil contamination, and studying the impact of industrial activities on ecosystems. In agriculture, these analyzers are used to evaluate soil fertility and optimize fertilizer use, contributing to sustainable farming practices. Geology is another field where CHNSO analyzers find application, helping geologists understand the composition of rocks and minerals and their formation processes. The versatility and precision of CHNSO analyzers make them indispensable tools in modern scientific research and industrial applications. As industries continue to prioritize sustainability and efficiency, the demand for advanced analytical tools like CHNSO analyzers is expected to grow, driving innovation and development in this market.

Energy, Chemical Industry, Environment, Agriculture, Geology, Other in the CHNSO Analyzers - Global Market:

CHNSO analyzers are extensively used across various sectors due to their ability to provide precise elemental analysis. In the energy sector, these analyzers are crucial for assessing the quality of fuels and optimizing combustion processes. By analyzing the carbon, hydrogen, nitrogen, sulfur, and oxygen content in fuels, energy companies can improve efficiency and reduce emissions, contributing to cleaner energy production. In the chemical industry, CHNSO analyzers are used for quality control and product development. They help ensure that chemical products meet the required specifications and standards by providing accurate data on their elemental composition. This is particularly important in the production of pharmaceuticals, polymers, and other chemical products where precise formulation is critical. Environmental applications of CHNSO analyzers include monitoring air and water quality, assessing soil contamination, and studying the impact of industrial activities on ecosystems. These analyzers help in identifying pollutants and understanding their distribution and fate in the environment, aiding in the development of strategies for pollution control and remediation. In agriculture, CHNSO analyzers are used to evaluate soil fertility and optimize fertilizer use. By analyzing the elemental composition of soil, farmers can make informed decisions about nutrient management, leading to improved crop yields and sustainable farming practices. Geology is another field where CHNSO analyzers find application. They help geologists understand the composition of rocks and minerals, providing insights into their formation processes and the history of the Earth's crust. This information is valuable for mineral exploration and understanding geological phenomena. The versatility and precision of CHNSO analyzers make them indispensable tools in modern scientific research and industrial applications. As industries continue to prioritize sustainability and efficiency, the demand for advanced analytical tools like CHNSO analyzers is expected to grow, driving innovation and development in this market.

CHNSO Analyzers - Global Market Outlook:

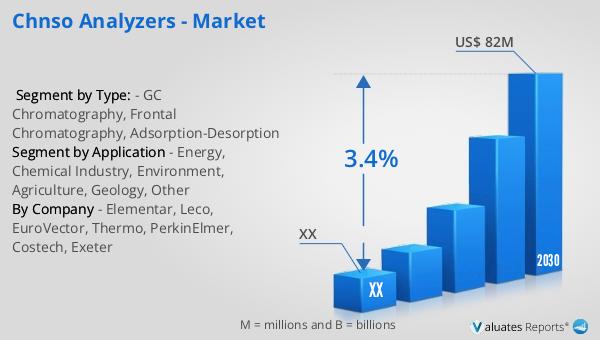

In 2023, the global market for CHNSO analyzers was valued at approximately $64 million. Looking ahead, it is anticipated that this market will expand to reach a revised size of $82 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.4% over the forecast period from 2024 to 2030. This growth trajectory underscores the increasing demand for precise elemental analysis across various industries. Notably, in 2019, the top seven players in the market accounted for a significant 90% of the global revenue share for CHNSO analyzers. This concentration indicates a competitive landscape dominated by a few key players who have established themselves as leaders in the field. These companies are likely to continue driving innovation and development in the market, leveraging their expertise and resources to meet the evolving needs of their customers. As industries continue to prioritize sustainability and efficiency, the demand for advanced analytical tools like CHNSO analyzers is expected to grow, driving innovation and development in this market. The market's growth is further supported by technological advancements that enhance the accuracy, speed, and user-friendliness of these analyzers, making them more accessible and appealing to a broader range of industries. As a result, the CHNSO analyzers market is poised for steady growth, driven by the ongoing demand for precise elemental analysis in diverse applications.

| Report Metric | Details |

| Report Name | CHNSO Analyzers - Market |

| Forecasted market size in 2030 | US$ 82 million |

| CAGR | 3.4% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Elementar, Leco, EuroVector, Thermo, PerkinElmer, Costech, Exeter |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |