What is Food Grade Vitamin B6 - Global Market?

Food Grade Vitamin B6 is a crucial component in the global market, primarily due to its essential role in human health and nutrition. This vitamin, also known as pyridoxine, is vital for numerous bodily functions, including amino acid metabolism, neurotransmitter synthesis, and hemoglobin production. The demand for food-grade Vitamin B6 is driven by its widespread application in the food and beverage industry, where it is used to fortify products and enhance nutritional value. As consumers become more health-conscious, there is an increasing preference for fortified foods that provide essential nutrients, including vitamins. This trend is further fueled by the growing awareness of vitamin deficiencies and their impact on health, prompting manufacturers to incorporate Vitamin B6 into their products. The global market for food-grade Vitamin B6 is also influenced by regulatory standards and guidelines that ensure the safety and efficacy of vitamin-enriched foods. These regulations help maintain product quality and consumer trust, thereby supporting market growth. Additionally, advancements in production technologies and the development of innovative delivery forms, such as powders and liquids, have expanded the market's reach, making Vitamin B6 more accessible to a broader audience. Overall, the food-grade Vitamin B6 market is poised for steady growth, driven by increasing consumer demand for health-enhancing food products.

Powder, Liquid in the Food Grade Vitamin B6 - Global Market:

In the global market for food-grade Vitamin B6, two primary forms are prevalent: powder and liquid. Each form has its unique advantages and applications, catering to different industry needs and consumer preferences. Powdered Vitamin B6 is widely used due to its stability and ease of incorporation into various food products. It is often added to dry mixes, baked goods, and dietary supplements, where it can be evenly distributed without affecting the product's texture or taste. The powdered form is also favored for its longer shelf life, making it a cost-effective option for manufacturers. On the other hand, liquid Vitamin B6 is gaining popularity for its versatility and ease of use in liquid-based products. It is commonly used in beverages, syrups, and liquid dietary supplements, where it can be easily blended and absorbed. The liquid form is particularly advantageous for products that require rapid nutrient delivery, as it is quickly absorbed by the body. Additionally, liquid Vitamin B6 can be used in formulations where precise dosing is essential, such as in medical nutrition products. The choice between powder and liquid forms of Vitamin B6 often depends on the specific application and desired product characteristics. For instance, in the beverage industry, liquid Vitamin B6 is preferred for its solubility and ability to maintain clarity in drinks. In contrast, the food industry may opt for powdered Vitamin B6 for its stability and ease of incorporation into solid products. Both forms of Vitamin B6 are subject to stringent quality control measures to ensure their safety and efficacy. Manufacturers must adhere to regulatory standards and guidelines, which dictate the permissible levels of Vitamin B6 in food products and supplements. These regulations are crucial in maintaining consumer trust and ensuring that products deliver the intended health benefits. The global market for food-grade Vitamin B6 is also influenced by technological advancements in production and formulation. Innovations in microencapsulation and nanotechnology have enhanced the stability and bioavailability of Vitamin B6, making it more effective in delivering health benefits. These advancements have opened new opportunities for product development and differentiation, allowing manufacturers to create unique offerings that cater to specific consumer needs. Furthermore, the increasing demand for clean-label and natural products has prompted manufacturers to explore alternative sources of Vitamin B6, such as plant-based and organic options. This trend aligns with the growing consumer preference for sustainable and environmentally friendly products, further driving the market for food-grade Vitamin B6. Overall, the powder and liquid forms of Vitamin B6 play a crucial role in the global market, offering diverse applications and benefits that cater to the evolving needs of consumers and industries alike.

Food, Beverage in the Food Grade Vitamin B6 - Global Market:

Food-grade Vitamin B6 is extensively used in the food and beverage industry, where it plays a vital role in enhancing the nutritional profile of products. In the food sector, Vitamin B6 is commonly added to fortified foods, such as cereals, bread, and snacks, to boost their vitamin content and provide additional health benefits. This fortification is particularly important in addressing vitamin deficiencies, which can lead to various health issues, including anemia, depression, and weakened immune function. By incorporating Vitamin B6 into food products, manufacturers can offer consumers a convenient way to meet their daily nutritional requirements. The use of Vitamin B6 in the food industry is also driven by the growing demand for functional foods, which are designed to provide health benefits beyond basic nutrition. These products often contain added vitamins, minerals, and other bioactive compounds that support overall health and well-being. Vitamin B6 is a popular choice for functional foods due to its role in energy metabolism and cognitive function, making it an attractive ingredient for products targeting active and health-conscious consumers. In the beverage industry, Vitamin B6 is used to fortify a wide range of drinks, including energy drinks, sports beverages, and fortified waters. These products are designed to provide a quick and convenient source of essential nutrients, catering to consumers with busy lifestyles and specific dietary needs. The inclusion of Vitamin B6 in beverages is particularly beneficial for individuals who may have difficulty obtaining sufficient vitamins from their diet alone. Additionally, Vitamin B6 is often used in combination with other B vitamins in multivitamin drinks, which offer a comprehensive approach to supporting overall health. The use of Vitamin B6 in the beverage industry is also influenced by consumer trends towards health and wellness, with an increasing focus on products that promote energy, mental clarity, and immune support. As a result, manufacturers are continually exploring new formulations and delivery methods to enhance the appeal and effectiveness of Vitamin B6-enriched beverages. The global market for food-grade Vitamin B6 in the food and beverage industry is supported by regulatory frameworks that ensure product safety and quality. These regulations help maintain consumer confidence and drive market growth by ensuring that fortified products deliver the intended health benefits. Overall, the use of food-grade Vitamin B6 in the food and beverage industry is a key driver of market growth, offering consumers a convenient and effective way to enhance their nutritional intake and support overall health.

Food Grade Vitamin B6 - Global Market Outlook:

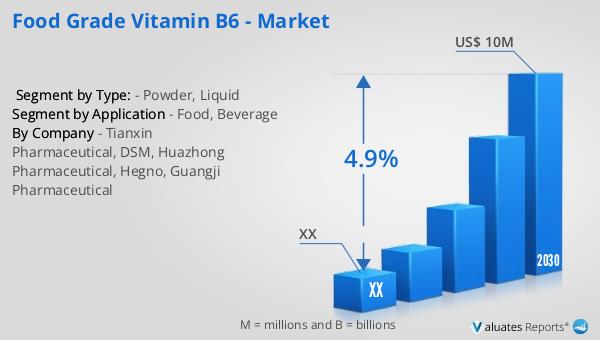

The global market for food-grade Vitamin B6 was valued at approximately $7 million in 2023, with projections indicating a growth to around $10 million by 2030. This growth represents a compound annual growth rate (CAGR) of 4.9% during the forecast period from 2024 to 2030. The North American market for food-grade Vitamin B6 is also expected to experience significant growth, although specific figures for this region were not provided. The anticipated expansion of the market can be attributed to several factors, including increasing consumer awareness of the health benefits associated with Vitamin B6 and the growing demand for fortified food and beverage products. As consumers become more health-conscious, there is a rising preference for products that offer additional nutritional benefits, driving manufacturers to incorporate Vitamin B6 into their offerings. Additionally, advancements in production technologies and the development of innovative delivery forms, such as powders and liquids, have made Vitamin B6 more accessible to a broader audience. These factors, combined with regulatory standards that ensure product safety and efficacy, are expected to support the steady growth of the food-grade Vitamin B6 market in the coming years.

| Report Metric | Details |

| Report Name | Food Grade Vitamin B6 - Market |

| Forecasted market size in 2030 | US$ 10 million |

| CAGR | 4.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Tianxin Pharmaceutical, DSM, Huazhong Pharmaceutical, Hegno, Guangji Pharmaceutical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |