What is Police Dog Orthopedic Implants - Global Market?

Police dog orthopedic implants represent a specialized segment within the broader veterinary medical device market, focusing on the health and mobility of working dogs, particularly those in law enforcement. These implants are designed to address orthopedic issues such as fractures, joint problems, and other musculoskeletal injuries that police dogs may encounter in the line of duty. Given the rigorous physical demands placed on these animals, maintaining their health is crucial for their performance and longevity. The global market for these implants is driven by the increasing recognition of the importance of animal welfare and the role these dogs play in public safety. As veterinary medicine advances, more sophisticated and effective implant solutions are being developed, tailored specifically for the unique anatomical and physiological needs of police dogs. This market is characterized by a range of products, including plates, screws, and joint replacement implants, each serving a specific purpose in the treatment and rehabilitation of injured dogs. The growth of this market is also supported by the rising investment in veterinary healthcare infrastructure and the increasing number of police dogs employed worldwide. As awareness and demand for high-quality veterinary care continue to rise, the police dog orthopedic implants market is poised for significant growth.

Plates, Screws, Joint Replacement Implants, Others in the Police Dog Orthopedic Implants - Global Market:

In the realm of police dog orthopedic implants, several key components play a vital role in ensuring the effective treatment of musculoskeletal injuries. Plates are one of the primary devices used in orthopedic surgeries for police dogs. These metal implants are designed to stabilize fractures by holding the broken pieces of bone together, allowing them to heal properly. Plates come in various shapes and sizes, tailored to fit different bones and fracture types. They are typically made from biocompatible materials like stainless steel or titanium, which are strong yet lightweight, minimizing the risk of rejection by the dog's body. Screws, often used in conjunction with plates, are another crucial element in orthopedic surgeries. They secure the plates to the bone, providing additional stability and support during the healing process. Like plates, screws are made from durable, biocompatible materials to ensure they integrate well with the dog's body. Joint replacement implants are another significant category within this market. These implants are used to replace damaged or diseased joints, such as hips or elbows, restoring mobility and reducing pain for the dog. Joint replacements are typically made from a combination of metal and plastic components, designed to mimic the natural movement of the joint. The development of these implants requires a deep understanding of canine anatomy and biomechanics to ensure they function effectively and comfortably for the dog. Other products in the police dog orthopedic implants market include pins, wires, and external fixators. Pins and wires are often used to hold small bone fragments together, while external fixators are devices that stabilize fractures from outside the body, allowing for adjustments during the healing process. Each of these components plays a critical role in the comprehensive treatment of orthopedic injuries in police dogs, ensuring they can return to their duties as quickly and safely as possible. The market for these implants is driven by ongoing advancements in veterinary medicine, as well as the increasing demand for high-quality care for working dogs. As technology continues to evolve, the development of more sophisticated and effective implant solutions is expected to further enhance the treatment options available for police dogs, ultimately improving their quality of life and ability to perform their duties.

Hunting Dog, Patrol Dog, Ambulance Dog, Other in the Police Dog Orthopedic Implants - Global Market:

The use of police dog orthopedic implants extends beyond law enforcement, encompassing a variety of working dogs, including hunting dogs, patrol dogs, ambulance dogs, and others. Hunting dogs, for instance, are often exposed to rough terrains and demanding physical activities, making them susceptible to orthopedic injuries. Implants such as plates and screws are commonly used to treat fractures and joint issues in these dogs, ensuring they can continue to perform their tasks effectively. Patrol dogs, which are frequently used in security and military operations, also benefit from orthopedic implants. These dogs are trained to perform a range of tasks, from detecting explosives to apprehending suspects, which can put significant strain on their musculoskeletal systems. Orthopedic implants help maintain their mobility and overall health, allowing them to carry out their duties with minimal discomfort. Ambulance dogs, which assist in search and rescue operations, are another group that relies on orthopedic implants. These dogs often work in challenging environments, such as disaster sites, where they may suffer from injuries like fractures or joint dislocations. Implants play a crucial role in their recovery, enabling them to return to their life-saving work as quickly as possible. Other working dogs, such as therapy dogs and service dogs, may also require orthopedic implants to address various musculoskeletal issues. These dogs provide essential support to individuals with disabilities or emotional needs, and maintaining their health is vital to their ability to perform their roles. The global market for police dog orthopedic implants is driven by the increasing recognition of the importance of animal welfare and the critical roles these dogs play in society. As veterinary medicine continues to advance, the development of more effective and specialized implant solutions is expected to enhance the treatment options available for working dogs, ultimately improving their quality of life and ability to serve.

Police Dog Orthopedic Implants - Global Market Outlook:

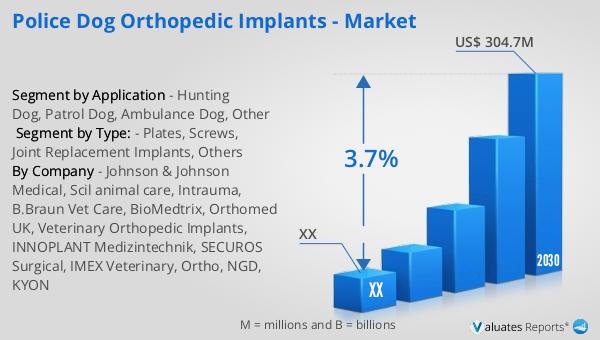

The global market for police dog orthopedic implants was valued at approximately $231 million in 2023. It is projected to grow to a revised size of $304.7 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.7% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for advanced veterinary care and the recognition of the vital role that police dogs play in law enforcement and public safety. The market for medical devices, in general, is estimated to be worth $603 billion in 2023, with a projected CAGR of 5% over the next six years. This broader market growth is driven by technological advancements, increasing healthcare expenditure, and the rising prevalence of chronic diseases. Within this context, the police dog orthopedic implants market represents a niche but important segment, highlighting the growing emphasis on animal welfare and the need for specialized medical solutions for working animals. As the market continues to expand, it is expected to offer new opportunities for innovation and development, ultimately benefiting both the animals and the industries that rely on them.

| Report Metric | Details |

| Report Name | Police Dog Orthopedic Implants - Market |

| Forecasted market size in 2030 | US$ 304.7 million |

| CAGR | 3.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Johnson & Johnson Medical, Scil animal care, Intrauma, B.Braun Vet Care, BioMedtrix, Orthomed UK, Veterinary Orthopedic Implants, INNOPLANT Medizintechnik, SECUROS Surgical, IMEX Veterinary, Ortho, NGD, KYON |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |