What is Feed Grade L-Valine - Global Market?

Feed Grade L-Valine is a crucial component in the global animal feed industry, primarily used to enhance the nutritional value of feed for livestock and poultry. L-Valine is an essential amino acid that animals cannot synthesize on their own, making it necessary to include it in their diet to ensure optimal growth and health. This amino acid plays a significant role in protein synthesis, tissue repair, and muscle metabolism, which are vital for the overall development of animals. The global market for Feed Grade L-Valine has been expanding due to the increasing demand for high-quality animal protein and the growing awareness of the benefits of balanced animal nutrition. As the livestock and poultry industries continue to grow, particularly in regions like Asia-Pacific and North America, the demand for Feed Grade L-Valine is expected to rise. This market is characterized by the presence of several key players who are investing in research and development to improve the efficiency and effectiveness of L-Valine in animal feed. Additionally, the market is influenced by factors such as regulatory standards, technological advancements, and the rising trend of sustainable and organic farming practices. Overall, Feed Grade L-Valine is an essential component in the animal feed industry, contributing to the health and productivity of livestock and poultry worldwide.

80%-90%, 90-99% in the Feed Grade L-Valine - Global Market:

The global market for Feed Grade L-Valine is segmented based on purity levels, with two primary categories being 80%-90% and 90%-99%. These purity levels are crucial as they determine the effectiveness and efficiency of L-Valine in animal feed. The 80%-90% purity segment is often used in standard feed formulations where cost-effectiveness is a priority. This segment caters to markets where the primary focus is on providing essential nutrients at a lower cost, making it suitable for large-scale livestock operations that require bulk feed production. On the other hand, the 90%-99% purity segment is targeted towards premium feed formulations. This higher purity level ensures maximum absorption and utilization of L-Valine by the animals, leading to better growth rates, improved feed conversion ratios, and enhanced overall health. This segment is particularly popular in regions where there is a high demand for quality meat products and where farmers are willing to invest in superior feed solutions to achieve better yields. The choice between these purity levels often depends on factors such as the type of livestock, the specific nutritional requirements, and the economic considerations of the farmers. In regions like Europe and North America, where there is a strong emphasis on animal welfare and sustainable farming practices, the demand for high-purity L-Valine is more pronounced. This is because farmers in these regions are more inclined to invest in high-quality feed to ensure the well-being of their animals and to meet stringent regulatory standards. Conversely, in developing regions where cost constraints are a significant concern, the 80%-90% purity segment tends to dominate the market. However, with the increasing awareness of the benefits of high-purity L-Valine and the growing trend towards sustainable farming, there is a gradual shift towards the 90%-99% segment even in these regions. The market dynamics for these purity levels are also influenced by technological advancements in feed formulation and the continuous efforts by manufacturers to optimize production processes. As the global demand for animal protein continues to rise, driven by population growth and changing dietary preferences, the market for Feed Grade L-Valine is expected to witness significant growth. This growth will be supported by the increasing adoption of high-purity L-Valine in animal feed formulations, as farmers and feed manufacturers strive to enhance the nutritional value of their products and meet the evolving needs of the livestock and poultry industries.

Poultry, Livestock in the Feed Grade L-Valine - Global Market:

Feed Grade L-Valine plays a vital role in the poultry and livestock industries, serving as a key ingredient in animal feed formulations. In poultry farming, L-Valine is essential for the growth and development of chickens, turkeys, and other birds. It aids in protein synthesis, which is crucial for muscle development and overall health. By incorporating L-Valine into poultry feed, farmers can ensure that their birds receive the necessary nutrients for optimal growth, leading to improved feed conversion ratios and higher meat yields. This is particularly important in the broiler industry, where the focus is on producing meat efficiently and sustainably. Additionally, L-Valine helps in enhancing the immune system of poultry, making them more resistant to diseases and reducing the need for antibiotics. In the livestock sector, L-Valine is equally important for the growth and productivity of animals such as cattle, pigs, and sheep. It supports muscle development, tissue repair, and energy metabolism, which are essential for the overall health and performance of livestock. By providing a balanced diet enriched with L-Valine, farmers can improve the growth rates and feed efficiency of their animals, leading to higher milk production in dairy cattle and better meat quality in beef cattle and pigs. Moreover, L-Valine contributes to the reproductive health of livestock, ensuring better fertility rates and healthier offspring. The use of Feed Grade L-Valine in animal feed is also aligned with the growing trend towards sustainable and organic farming practices. By optimizing the nutritional content of feed, farmers can reduce the environmental impact of livestock production and promote animal welfare. This is particularly relevant in regions where there is a strong emphasis on sustainable agriculture and where consumers are increasingly demanding ethically produced animal products. Overall, the usage of Feed Grade L-Valine in poultry and livestock farming is crucial for enhancing the productivity and sustainability of these industries, ensuring that they can meet the growing global demand for high-quality animal protein.

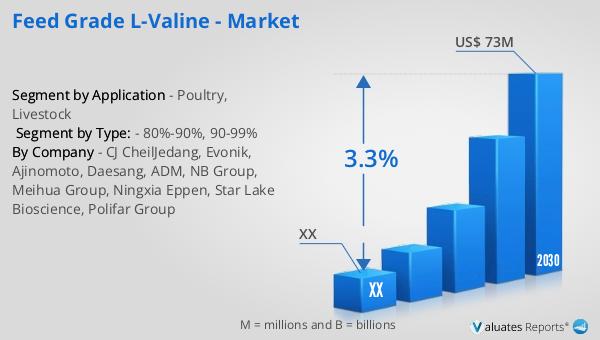

Feed Grade L-Valine - Global Market Outlook:

The global market outlook for Feed Grade L-Valine indicates a promising future, with the market valued at approximately US$ 58 million in 2023. This figure is expected to grow, reaching an estimated size of US$ 73 million by 2030. This growth trajectory reflects a compound annual growth rate (CAGR) of 3.3% during the forecast period from 2024 to 2030. The steady increase in market size can be attributed to several factors, including the rising demand for high-quality animal protein, advancements in feed formulation technologies, and the growing awareness of the benefits of balanced animal nutrition. As the livestock and poultry industries continue to expand, particularly in emerging markets, the demand for Feed Grade L-Valine is expected to rise. This growth is also supported by the increasing adoption of sustainable farming practices and the emphasis on animal welfare, which drive the need for high-quality feed ingredients like L-Valine. Additionally, the market is influenced by regulatory standards and the continuous efforts by manufacturers to optimize production processes and improve the efficiency of L-Valine in animal feed. Overall, the global market for Feed Grade L-Valine is poised for significant growth, driven by the evolving needs of the livestock and poultry industries and the increasing focus on sustainable and ethical farming practices.

| Report Metric | Details |

| Report Name | Feed Grade L-Valine - Market |

| Forecasted market size in 2030 | US$ 73 million |

| CAGR | 3.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | CJ CheilJedang, Evonik, Ajinomoto, Daesang, ADM, NB Group, Meihua Group, Ningxia Eppen, Star Lake Bioscience, Polifar Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |